Fed Stimulus Clears Path for Gold Run

01 September 2020

The level of stimulus the Federal Reserve (Fed) has thrown at the economy this year is almost unprecedented and has investment consequences.

First, gold. Our outlook for gold has been bullish since the summer of 2019, and the case for gold investing has become more solid in recent weeks as gold rallied through its $1,800 per ounce technical resistance level and past its previous high of $1,921.

To help gauge how high gold could go, we looked at prior gold bull markets—which could be categorized as either inflationary or deflationary—as well as the persistence of negative real interest rates. Our base case now is that we are in a deflationary environment and, based on historical trends, gold’s price typically moves up two to three times in a deflationary cycle. This helped inform the $3,400 price target we have set for gold. (See prior gold bull markets here.)

Financial markets have also benefited from the Fed stimulus. And perhaps the surprise from this summer’s data is that the global economy is doing quite well, supporting the markets, despite the social distancing that we all feel in our personal lives. Important commodities like copper have regained pre-COVID highs. In addition, China’s industrial recovery is pointing to all-time highs in activity, even while the consumer activity is still below prior-year levels.

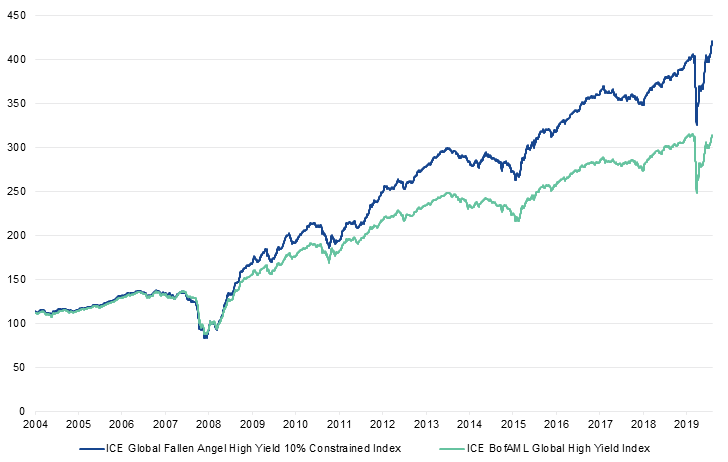

A Beneficiary: High Yield and Fallen Angel Bonds

In a recessionary environment, some bonds are going to default or be downgraded. Fixed income markets this year generally started recovering after the Fed announced plans to intervene. We have already seen a record amount of new fallen angel bond volume over $140B as of 31 July 20201—and expect more through the remainder of the year.

Similar to 2016, we have seen a lot of energy companies downgraded to become fallen angels, and the fallen angel strategy is buying those downgraded bonds. These new energy fallen angels are among the top contributors to performance of the fallen angel strategy so far this year. As long as the Fed remains supportive, we believe this strategy should continue to do well.

Fallen Angel High Yield Bonds vs. Broad High Yield Bond Market

31/12/2003 – 31/7/2020

Source: ICE Data Indices as of 31/7/2020. This chart is for illustrative purposes only. Broad High Yield Bond Market is represented by the ICE BofAML Global High Yield Index. Fallen Angel Global High Yield is represented by the ICE Global Fallen Angel High Yield 10% Constrained Index (HWCF). Index performance is not illustrative of fund performance. Indexes are unmanaged and are not securities in which an investment can be made. Current data may differ from data quoted. Past performance is no guarantee of future results. An investor cannot invest directly in an index. The results assume that no cash was added to or assets withdrawn from the index.

Risks to this Scenario

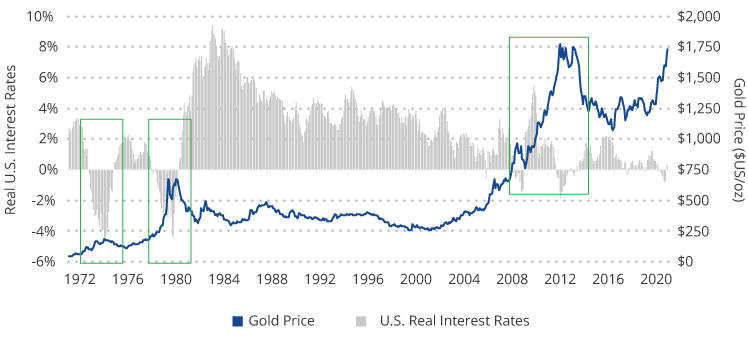

One risk to gold and bonds is if there were to be an unforeseen rise in interest rates in the U.S. This could come from a burst of inflation driven by supply chain issues or money supply growth, for example. This is not our “base case”, but it is possible. As we can see from the chart below, higher real interest rates are not good for gold.

Gold Price vs. Real Interest Rates

Source: VanEck, FactSet, Bloomberg. Data as of May 2020. Past performance is no guarantee of future results.

Another concern for the market is that the return to full employment may be bumpy. An incredible number of people have been laid off in the U.S. and, regardless of GDP numbers, people are unlikely to return to work at the same levels as the start of the year. Concern may be high enough for policy makers to take additional steps that may impact the financial recovery.

2020 Elections: Focus on Policies, not Politics

In our view, it is hard to invest according to politics, but it is important to look at the underlying policies and see if they are going to change. Regardless of who is elected in November, we don’t anticipate a big shift in Fed policy. As far as tax policy, we think there would have to be quite a degree of confidence in the economic recovery before any possible fiscal shock in terms of a big tax increase. In our view, investors should ignore all the political noise and make sure there is going to be a policy change before shifting their assets.

1Source: FactSet, ICE Data Indices, LLC and Morningstar.

Belangrijke kennisgeving

Uitsluitend voor informatie- en advertentiedoeleinden.

Deze informatie is afkomstig van VanEck (Europe) GmbH. VanEck (Europe) GmbH is aangesteld als distributeur van VanEck-producten in Europa door VanEck Asset Management B.V., een beheermaatschappij onder Nederlands recht en geregistreerd bij de Nederlandse Autoriteit Financiële Markten (AFM). VanEck (Europe) GmbH, met als vestigingsadres Kreuznacher Str. 30, 60486 Frankfurt, Duitsland, is een financiële dienstverlener die onder toezicht staat van BaFin, de Duitse toezichthouder voor de financiële markten. De informatie is uitsluitend bedoeld om beleggers te voorzien van algemene en voorlopige informatie en mag niet worden opgevat als beleggings-, juridisch of fiscaal advies. VanEck (Europe) GmbH en de aan VanEck (Europe) GmbH verbonden en gelieerde bedrijven (samen "VanEck") wijzen elke aansprakelijkheid van de hand met betrekking tot beslissingen die de belegger op basis van deze informatie neemt ten aanzien van het kopen, verkopen of aanhouden van beleggingen. De visies en meningen die hier worden gegeven, zijn die van de auteur(s) en komen niet noodzakelijkerwijs overeen met die van VanEck. De meningen zijn actueel op de datum van publicatie en kunnen worden aangepast op basis van veranderende marktomstandigheden. Bepaalde verklaringen in deze bijdrage kunnen ramingen, voorspellingen en andere op de toekomst gerichte verklaringen zijn die niet overeenkomen met de werkelijkheid. Wij achten de informatie die afkomstig is van derden, betrouwbaar. Deze informatie is echter niet onafhankelijk gecontroleerd. De nauwkeurigheid en volledigheid ervan kunnen daarom niet worden gegarandeerd. Alle indices die worden vermeld, zijn maatstaven voor het vergelijken van algemene marktsectoren en rendementen. Het is niet mogelijk om rechtstreeks in een index te beleggen.

Alle rendementsgegevens hebben betrekking op het verleden en bieden geen garantie voor toekomstige resultaten. Beleggen brengt risico's met zich mee, waaronder mogelijk verlies van de hoofdsom. Lees het prospectus en de essentiële beleggersinformatie voordat u gaat beleggen.

Niets in dit materiaal mag in welke vorm dan ook worden verveelvoudigd en er mag ook niet naar worden verwezen in andere publicaties zonder de uitdrukkelijke schriftelijke toestemming van VanEck.

© VanEck (Europe) GmbH

Gerelateerde inzichten

Related Insights

08 december 2023

10 oktober 2023

10 oktober 2023

15 augustus 2023

08 december 2023

10 oktober 2023

10 oktober 2023

15 augustus 2023