Can EM Rates Defy the U.S. Fed?

08 March 2023

Read Time 2 MIN

U.S. Fed Rate Hikes

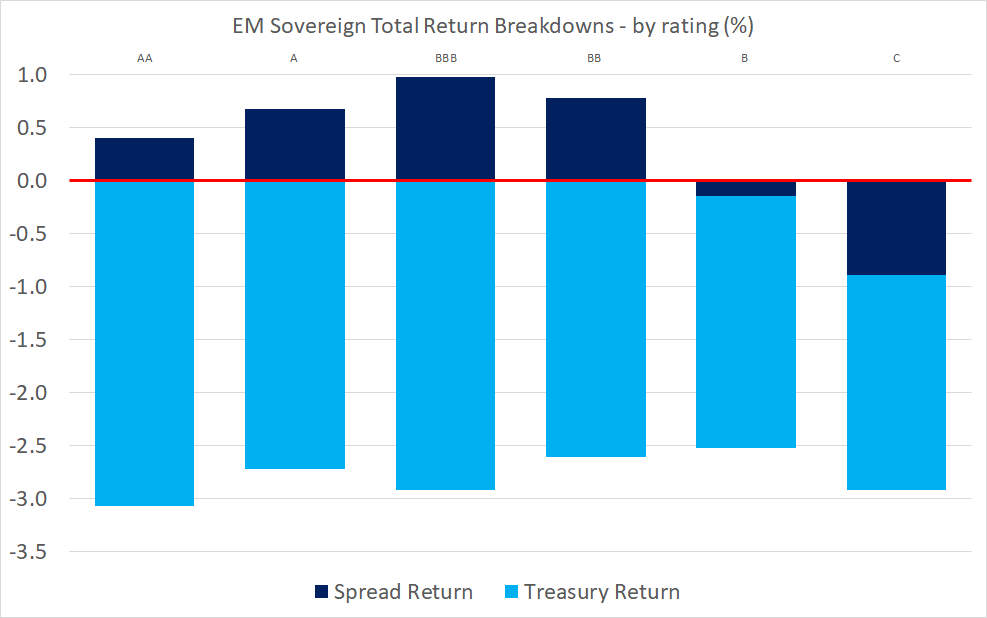

The U.S. Federal Reserve Chairman’s testimony scared the market into pricing even more rate hikes. The peak rate implied by the Fed Funds Futures reached 5.65%, the implied probability of June’s hike is now above 80%, and the market thinks that the Fed might opt for a larger 50bps hike this month. Today’s above-consensus ADP employment print (242k) did little to dissuade the market hawks. So, we are waiting for the Fed’s Beige Book this afternoon with some trepidation. What does it all mean for emerging markets (EM) bonds? The chart below shows that the rising “risk-free” rate was the main factor that affected sovereign returns in February and March – across all rating categories. In addition, the rising volatility of “risk-free” rates pushed down spread returns on lower-rated EMs – in part due to concerns about their structural and institutional ability to handle higher global rates.

EM Disinflation

What we find quite interesting though is that the market continues to price in – still cautiously – policy rate cuts in various EMs, despite the rising expectations for the U.S. peak rate. Why? Because many EMs tightened early and aggressively in response to rising price pressures (=high real rates), and inflation is clearly moderating (albeit sometimes in a “bumpy” manner). This week’s big inflation data dump in EM looks promising so far – we had good results in EM Asia yesterday (Philippines and Thailand), which were followed by another downside surprise in LATAM (Chile). If everything goes according to plan, inflation prints in Mexico (Thursday) and Brazil (Friday) should reaffirm the EM disinflation trend.

EM Fiscal Outlook

One potential headwind for EM doves is fiscal slippage. Brazil is a great example to illustrate this point. Brazil’s real policy rate based on expected inflation is super-high (around 8%), but the uncertainty about new administration’s spending plans kept the market and the central bank on defensive for quite some time. The recent reduction in political noise and a promise of decent tax reform did wonders for the rate cut expectations though – and there is definitely more to come if the administration stays fiscally responsible. Another example is Hungary, where a surprising fiscal splurge (around 50% of the annual deficit target in the first two months of the year) raised questions about the easing timeline, even though headline inflation finally peaked and food/core services pressures are moderating. Stay tuned!

Chart at a Glance: U.S. Fed Hawks and EM Sovereign Bonds

Source: Bloomberg LP. Data from 1/31/2023 to 3/7/2023.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.