EM Bonds – Policies Matter

04 January 2023

Read Time 2 MIN

China Policy Support

We had two strong contenders for today’s daily chart – China and Brazil – as both countries demonstrate the impact of changing government policies on bond returns. China’s reopening and concerted efforts to support real estate developers after the 20th communist party congress have led to a massive corporate bond rally (High Yield in particular) at the end of 2022. Reports about more support – especially for systemically important players – ensured that the rally continued in the early days of 2023, despite surging COVID infections and outright scary domestic activity gauges (such as 41.6 non-manufacturing Purchasing Managers Index).

Brazil Populism Concerns

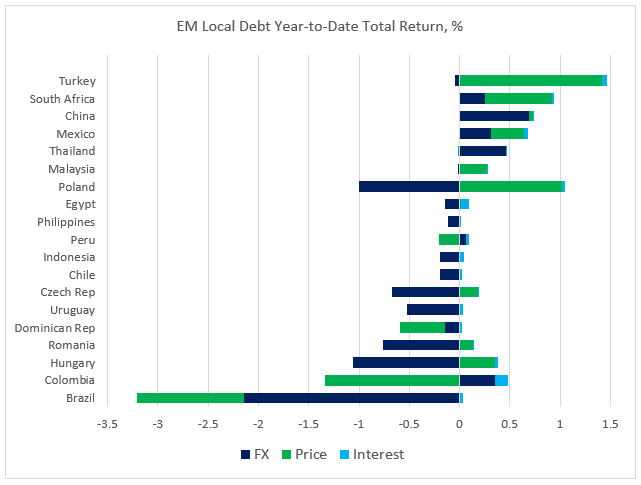

The policy U-turn in Brazil, however, is producing the opposite result. The market initially gave President-elect Luiz Inácio Lula da Silva the benefit of the doubt, hoping his latest political “incarnation” would be less populist. But this does not seem to be quite the case – judging by spending initiatives and inauguration speeches – which explains the market’s concern about reforms rollback and fiscal expansion. These concerns are strong enough to offset the impact of other – much more positive – factors, such as Brazil’s very high real interest rates, fast disinflation, and solid external accounts (high international reserves, basic balance surplus). Brazil’s local bonds underperformed GBI-EM peers by a wide margin so far this year (see chart below), continuing the post-runoff trend. Policy concerns are also a reason why the market prices in only 65bps of rate cuts in Brazil in 2023.

EM Tightening Exits

Central Europe’s combo of dovish policy shifts (Poland, Czech Republic) and emergency rate hikes (Hungary) caused heart palpitations on more than one occasion last year. Still, strong institutions and a prospect of cooling inflation helped to reassure the market in Q4. The region is not yet out of the woods, though. Hungary’s large twin deficit (a sum of fiscal and current account deficits) might require additional bond issuance (including U.S. Dollar denominated bonds) – especially if there are further delays in the disbursement of the EU funds. Poland’s election cycle is expected to widen the budget deficit from estimated 3.9% of GDP in 2022 to 5.4% of GDP this year – potentially testing the market and the central bank’s dovish resolve. Stay tuned!

Chart at a Glance: Brazil – At the Bottom of EM Local Debt Pack

Source: Bloomberg LP.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.