EM – Fighting Against DM Currents

26 September 2022

Read Time 2 MIN

Rising Global Rates

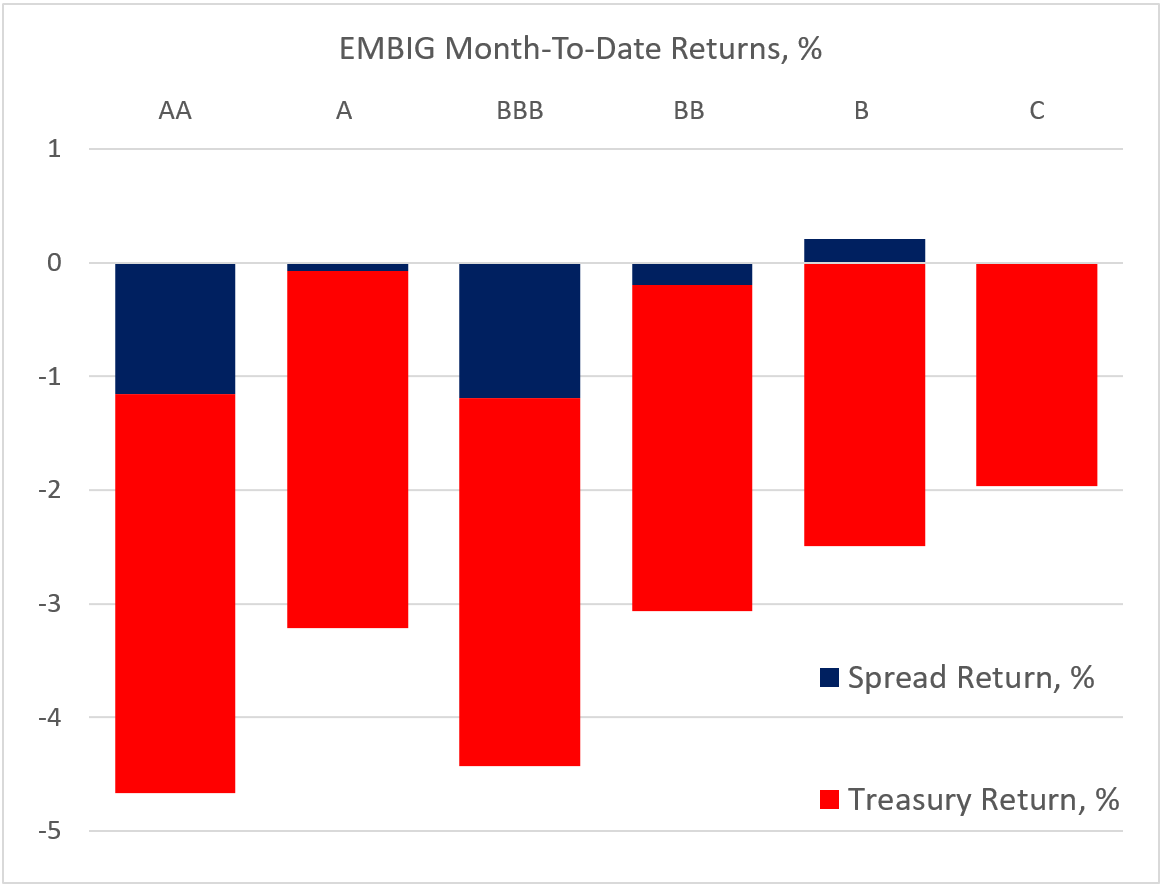

Emerging markets (EM) are caught in the global sentiment vortex, and rising global rates are dragging down returns on EM debt – irrespective of ratings and often “overriding” fundamentals (see chart below). This is one reason we closely monitor the market expectations for key policy rates – the expectations for the U.S. Federal Reserve were stable this morning, with the November hike (+75bps) and the cycle’s terminal rate (4.73%). The current surge in the terminal rate expectations for the Bank of England (over 6% as of this morning, according to Bloomberg LP) is still perceived as an isolated event, driven by the local policy agenda.

EM Tightening Cycles

It is noteworthy that the market continues to acknowledge EMs’ aggressive – and early – rate hike frontloading in the current cycle and does not automatically adjust the terminal rate expectations in lockstep with developed markets (DM), as was often the case in the past. Brazil is #1 on the “Divergent” list. The central bank stayed on hold at its last meeting, and the local swap curve does not price any additional rate hikes. Brazil’s real policy rate adjusted by expected inflation is the highest in EM, and it is one of the few countries where the 2022 growth outlook was revised upwards (a lot – from 0.5% to 2.35%). And today’s balance of payments numbers showed that Brazil might have problems (including a very entertaining political scene), but external is not one of them. Emerging markets where the markets did raise the terminal rate expectations in a meaningful way are relative latecomers to the global tightening cycle (Hungary, Malaysia, and South Africa).

China Growth And FX

China is a major dovish exception in EM (and the world), as authorities are trying to prop up this year’s GDP growth (the consensus forecast has been cut to 3.35%) amidst the housing sector disruptions and the zero-COVID approach. A side-effect of easing policies is the currency weakness – and the pace of depreciation is now getting too fast for comfort. This explains why the central bank decided to impose a 20% risk reserve requirement on FX forward sales for banks, hoping this will help stabilize the market expectations for the renminbi. Stay tuned!

Chart at a Glance: EM Sovereign Debt Total Returns by Rating Bucket*

Source: Bloomberg LP

EMBIG – JP Morgan’s Emerging Market Bond Global Index that tracks total returns for traded external debt instruments in the emerging markets.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.