Global Rates – No Pause For You?

03 November 2022

Read Time 2 MIN

Global Tightening Cycles

Developed markets (DM) doves are backing off for now, following yesterday’s 75bps hike by the U.S. Federal Reserve (Fed) and Chairman Powell’s “I am the boss” press conference, which scared the daylights out of many risky assets. The Fed Funds Futures effectively added one more 25bps rate hike in 2023, bringing the expected terminal rate to 5.16%. The European Central Bank (ECB) terminal rate expectations moved above 3%. Several ECB speakers said today that hikes should not be affected by political noise and that the policy rate should rise much higher.

EM Asia Inflation Pressures

Against this backdrop, today’s off-cycle central bank meeting in India raised concerns that there will be another emergency rate hike there. But it turned out that the central bank simply wanted (was asked?) to explain to the government why it missed the inflation target for three quarters in a row. A larger rate hike, however, seems imminent in the Philippines. The central bank signaled once again that it might raise its policy rate by 75bps on November 17 – moving in step with the Fed – due to inflation concerns (the October print is out this evening). Unlike the Philippines, central banks in Indonesia and Malaysia might have more policy room for the dovish pivot. The Bank Indonesia pointed out that the second round of inflationary effects was not as strong as initially feared. The central bank of Malaysia stated that it was not on a “pre-set course” after today’s expected 25bps rate hike.

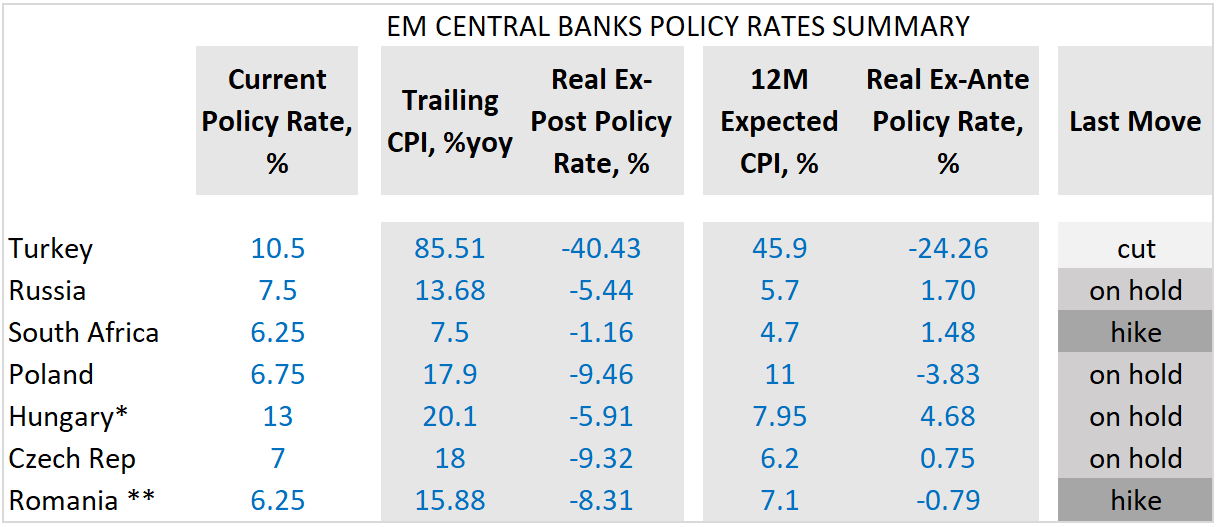

EM Peak Rates

The “data dependent” argument was also made by the governor of the Peruvian central bank, inviting suggestions that it might stay on hold already next week, joining Brazil and (maybe) Chile. While LATAM is contemplating exits from the tightening cycles, most of EMEA is already there (see chart below). The region now has only two active “hikers” – South Africa and Hungary (shadow hikes) – and today’s “on hold” decision by the Czech national bank confirmed the status quo. The next important milestone for the region is Poland’s rate-setting meeting. The central bank surprised the markets by keeping the policy rate unchanged in September. Still, inflation accelerated more than expected last month, and the market continues to price in more hikes on a 12-month horizon. Stay tuned!

Chart at a Glance: EMEA Doves Come in Droves

Source: VanEck Research; Bloomberg LP

* Hungary’s official policy rate is on hold, but there is massive shadow tightening

** Romania hiked, but indicated that this is likely to be the last hike

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.