Global Recession Narrative - Policy Dilemma

23 June 2022

Read Time 2 MIN

Global Recession Fears

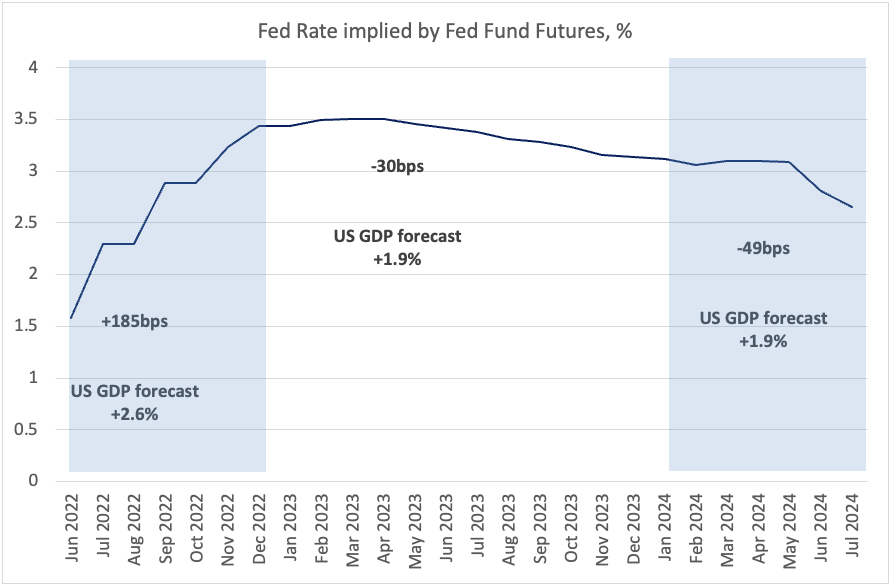

Weak European activity gauges (Purchasing Managers Indices, PMI) reinforced growth concerns in the region this morning. The subsequent below-consensus PMI prints in the U.S. gave an extra boost to the global recession narrative, leading to a massive rally in U.S. Treasuries and European rates (including Central Europe). The consensus growth forecast for both regions (Europe and the U.S.) still looks rosy 1-2 years ahead (around 2%), but the market expectations for the policy rate in the U.S. (Fed Fund Futures) tell a less optimistic growth story, anticipating that the current tightening cycle will end in December and seeing rate cuts from H2-2023 on (see chart below).

Pace of Rate Hikes in EM

This macro backdrop creates additional policy challenges for emerging markets (EM), where tightening is already well underway, but inflation pressures are not yet abating. Central banks in Chile (CLP) and Brazil (BCB) believe that aggressive rate hike frontloading gave them room to proceed at a slower pace from now on. However, Mexico might not have such luxury yet. The latest bi-weekly inflation prints – both headline and core – surprised significantly to the upside (respective 7.88% and 7.47% year-on-year), moving further away from the target (2-4%), and cementing the consensus expectation of a 75bps rate hike this afternoon (with a small probability of a larger 100bps move).

Monetary Policy Room in EM Asia

One EM region that can afford to proceed gradually with policy normalization is EM Asia. Regional headline inflation is much closer to the official targets than either in EMEA and LATAM, and even within the target range in two countries (China and Indonesia). This explains why the Indonesian central bank (BI) chose to stay on hold earlier today (after adjusting the reserve requirements for banks higher in May, and hoping that fiscal subsidies will cap inflation pressures), and why the Philippine central bank (BSP) raised its policy rate only by 25bps. The regional focus now shifts to Thailand, which refused to hike - the policy rate is still at 0.5%! - despite annual headline inflation surging to 7.1%. The next rate-setting meeting is in August, and we strongly suspect that another “oversized” inflation print will change the doves/hawks balance at the central bank. Stay tuned!

Chart at a Glance: Fed Fund Futures – Anticipating Recession?

Source: VanEck Research; Bloomberg LP

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.