Policy Reaction to Mixed Data Signals

02 December 2022

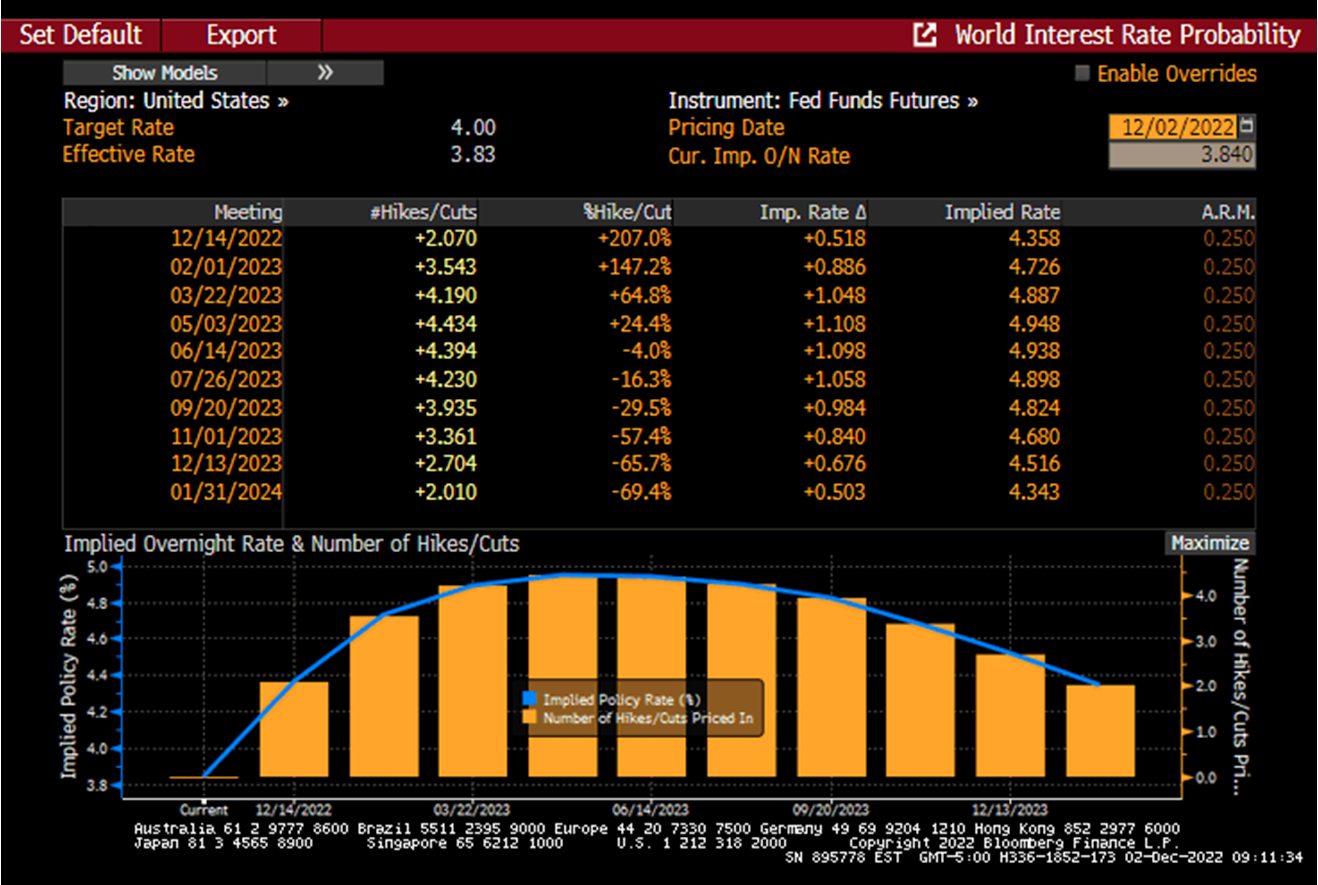

The Pace of Fed Hikes

The global data flow does not challenge the slowdown narrative, but it also shows that the momentum is very uneven – today’s strong labor market report in the U.S. could not have looked more different from this week’s ISM survey, which sent a much weaker signal. Both releases are, however, consistent with the market view that the U.S. Federal Reserve (Fed) can and should continue raising its policy rate, but at a slower pace (see chart below). At the same time, upside surprises like the strong labor market report raise a question mark as to whether the Fed would indeed have room for around 40bps of rate cuts in H2-2023.

EM Disinflation

The data flow in emerging markets (EM) is also not uniform – especially on the inflation front. The overall trend in EM inflation surprises is down, but it does not mean that we do not get an occasional above-consensus print, like in Peru. Peruvian headline inflation unexpectedly accelerated to 8.45% year-on-year in November, interrupting the nascent disinflation trend and signaling that the underlying price pressures may prove more persistent than previously thought. The year-to-date total return on Peru’s local debt (J.P. Morgan’s GBI-EM Peru U.S. Dollar Unhedged Index1) is still positive, but future performance will depend on the central bank’s ability to navigate the situation credibly (and this includes the expected 25bps rate hike next week). South Korea’s inflation print was the opposite of Peru – a nice downside surprise, which can allow the central bank to pause going forward.

EM Growth Slowdown

As regards upside growth surprises, some (if not most) of them require additional context. For example, Chile’s economic activity was stronger than expected in October, but it was still contracting at an accelerated pace (-1.2% year-on-year). In the same vein, today’s upside surprise in the Czech Republic’s Q3 GDP masked another sequential decline (-0.2% quarter-on-quarter), which might get worse going forward judging by the super-weak November PMI (41.6). There is no question that the central bank will stick to its “on hold” stance under these circumstances. Finally, Brazil’s industrial production growth also beat consensus in October, but the new administration’s policy agenda could have an impact (and not necessarily positive) on the business sentiment – a worrying prospect against the backdrop of a sharp decline in Brazil’s manufacturing PMI (to 44.3). Stay tuned!

Chart at a Glance: Market Sticks to Its Policy Rate Expectations for the Fed

Source: Bloomberg LP

1J.P. Morgan GBI-EM Peru U.S. Dollar Unhedged Index is the Peru subset of the GBI-EM Index, defined below.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.