Rate Hikes – The End Is Nigh?

01 February 2023

Read Time 2 MIN

Fed Rate Cuts

The focus of the day is the U.S. Federal Reserve’s (Fed’s) rate-setting meeting. The U.S. data-flow – including below-consensus ADP employment change and the ISM survey – are supportive of a smaller +25bps move, but the main “attraction” will be the Fed’s guidance. The market continues to price in rate cuts in 2023 (around 44bps), despite the fact that the Fed’s message has been more hawkish. The market expectation of policy easing in emerging markets (EM) and developed markets (DM) set a potentially positive stage for lower interest rates, driving EM performance at the end of 2022, and so far this year. And this is the reason why the EM folks will be glued to their Bloomberg screens this afternoon.

EM Disinflation

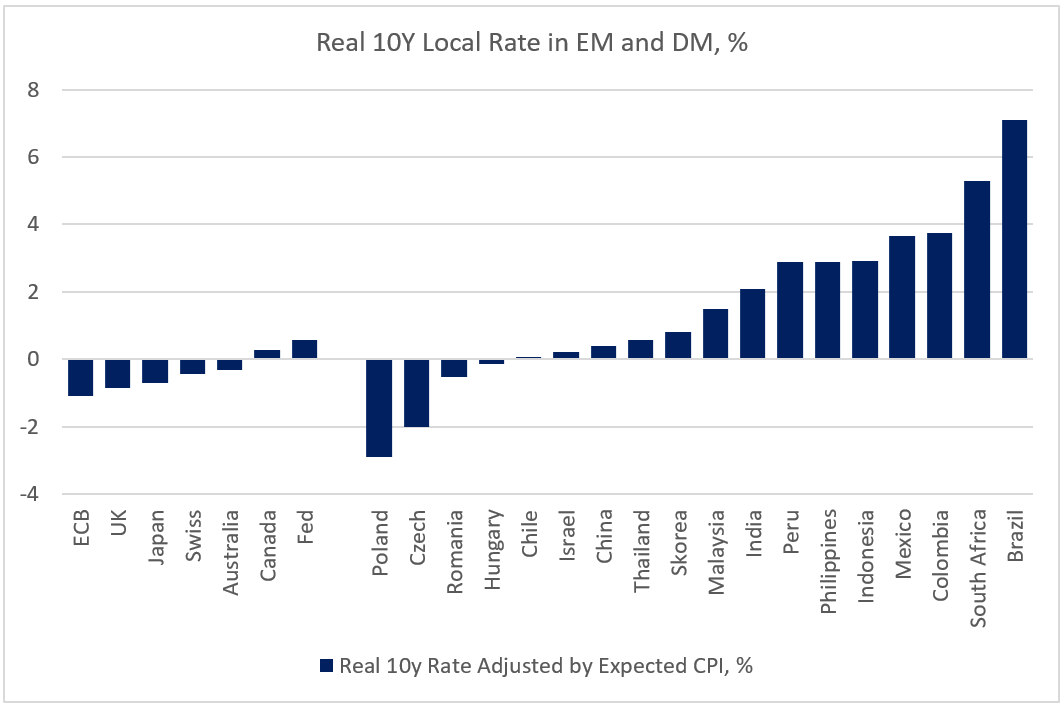

Some fundamental developments in EM argue in favor of ending the tightening cycles. Peak inflation is already behind in most countries – today’s downside surprises in Indonesia and Peru are good examples. A high base effect will also help to drive inflation down in the coming months – as will lower energy prices. The latter will have a particularly strong impact in Central Europe, where headline inflation can decline to single digits in Q4. Lower inflation is a boon for EM real yields, which already look attractive compared to their DM peers (see chart below).

China and EM Growth Tailwinds

There are risks though – and this is why many EM central banks are not in a hurry to open the door for rate cuts. Inflation is still far from the official targets in most places. Fiscal stimulus might still be positive in several EMs (due to a more populist policy agenda like in Brazil or an election cycle like in Poland). China might rebound at a faster pace – a potential upside risk for commodity prices, but also a major tailwind for EM growth, especially in countries with strong trade/tourism connections with China. Today’s stronger than expected activity gauges (Purchasing Managers Indices) in Thailand, Indonesia and the Philippines gave some food for thought in this regard. In Europe, the manufacturing PMIs in Poland and the Czech Republic continued to bounce from low levels. If the growth outlook continues to improve, EM central banks might feel comfortable staying on the sidelines for longer. Stay tuned!

Chart at a Glance: EM Real Local Rates – Nice Lineup!

Source: VanEck Research; Bloomberg LP.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.