“Agnostic” Fed = Bullish EM?

02 February 2023

Read Time 2 MIN

Fed Policy Outlook

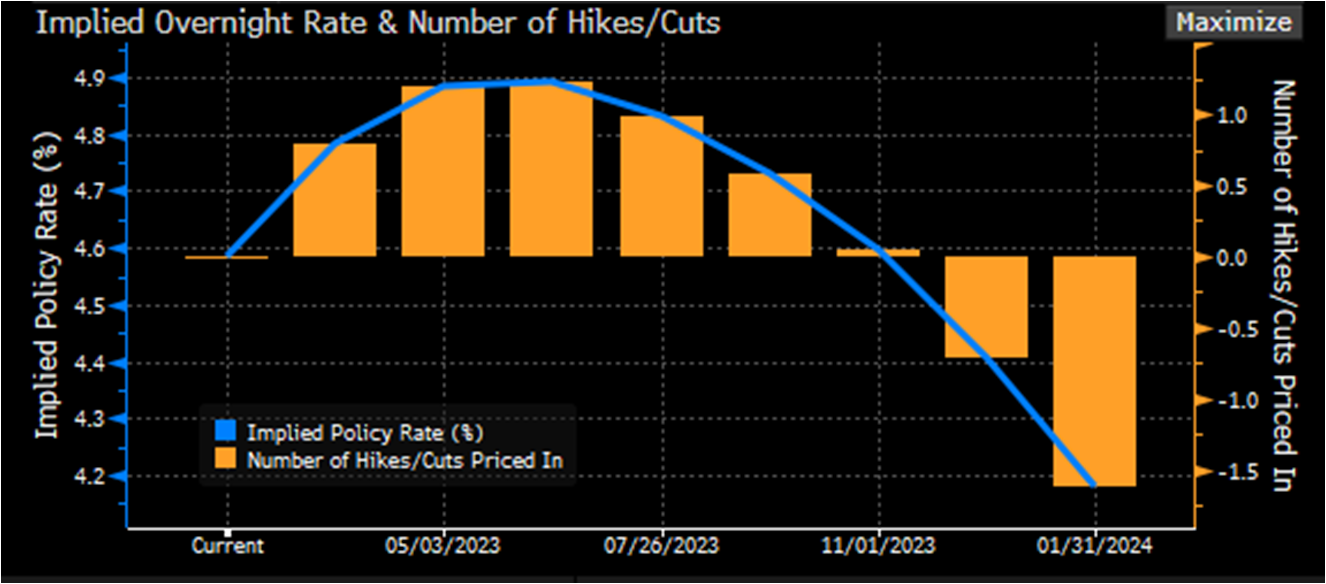

U.S. Federal Reserve (Fed) Chairman Jerome Powell’s defense against the market’s dovish expectations and easing monetary conditions at yesterday’s press conference was not particularly convincing. The Fed’s “data-dependent” message – and the mention of disinflation – pushed the implied peak rate below 4.9% and reaffirmed the expectation of rate cuts (about 50bps – see chart below) already this year, further supporting emerging markets (EM) assets. There are potential risks on both sides – a nasty recession in the U.S. could be risk-negative despite lower interest rates and slower disinflation would argue against rate cuts – but these scenarios might not disturb the status quo for some time.

Risk-On Fed

The “everything rally” lifts many boats, but a specific set of policies in EM can make a difference as well. The Brazilian central bank kept the policy rate on hold yesterday and issued a stark warning against the “heightened uncertainty” on the fiscal framework, which is pushing inflation projections away from the target (“no rate cuts for you!”). A combination of high carry, the hawkish (=credible) central bank, and the “agnostic” Fed lifted the Brazilian real to the top of the global FX “league table” in the morning trade. The Czech national bank also sounded cautious today, saying that the policy rate path might be higher than the market expects.

Global Disinflation

EMs’ bumpy and noisy disinflation (especially in core prices) is a reason why various central banks are choosing to stay on the sidelines instead of rushing into rate cuts. The Czech national bank assumed a big inflation increase in January. South Korean inflation surprised to the upside in January, re-accelerating to 5.2% year-on-year. The forthcoming inflation releases in Thailand, Colombia and the Philippines will also be closely watched. These countries are well positioned to benefit from China’s growth rebound – a major driver for EM assets in the coming months – but domestic policy agendas will determine whether this potential can be fully realized. Stay tuned!

Chart at a Glance: Implied U.S. Federal Reserve Rate Cuts – EMs Are Watching

Source: Bloomberg LP.

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.