China – Growth Weakness vs. Market Optimism

30 November 2022

Read Time 2 MIN

China Slowdown

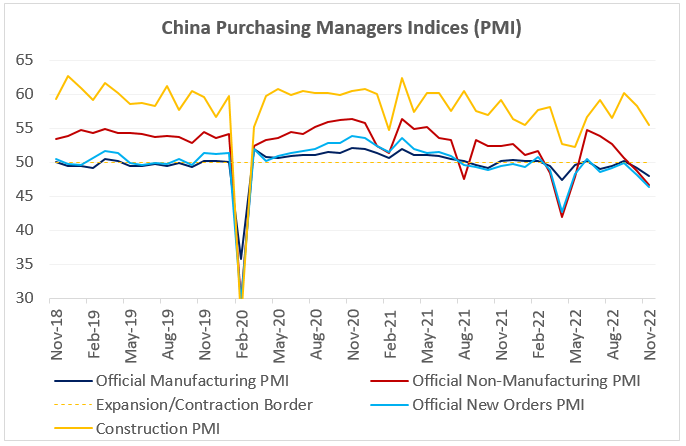

China’s domestic activity gauges for November were bad, no question about it. Most indices were well in contraction zone and deteriorating (see chart below). Even the construction PMI1 (Purchasing Managers Index) – which benefited from the earlier infrastructure stimulus – eased from 58.2 to 55.4. So, why is the market choosing to downplay the weakness? The answer is that authorities made several pre-emptive policy moves before the release, and, importantly, these initiatives address the underlying reasons of the slowdown – primarily real estate and re-opening.

China Real Estate Developers

The re-opening is still very tentative – the 20-point plan focuses on the optimization of the pandemic control, quarantine times, the frequency of testing and risk area delineations – but support for property developers looks more solid. The real estate package includes “stable financing” (the resumption of equity funding for listed companies, bond issuance, “reasonable” loan extension, relending facilities and absolving lenders from personal responsibility if something goes wrong), equal treatment of state-owned and private developers and mortgage support for homebuyers. Given the foregoing, it is not surprising that China’s High Yield/developers’ bonds staged a nice rally in the past week or so.

China Growth – Global Implications

One problem that China cannot fix on its own is weakening global demand – the new export orders PMI dropped to 46.7, which is the lowest level since May. “2023 Growth Cliff” is the most likely scenario for China’s main trade partners, and this underscores the importance of domestic pro-growth policies and orderly re-opening. Earlier reports about vaccination plans for the elderly and the easing of COVID restrictions in Guangzhou look encouraging, even though the progress will probably be slow and uneven (despite assertions that the anti-lockdown protests might turn out “stimulative”). The prospect of China’s domestic rebound – and commodity prices’ reaction to it – raises some interesting questions about (a) global disinflation and (b) growth spillovers in emerging markets (EM) (especially for commodity exporters). But this might be a story for Q2-Q3 next year. Stay tuned!

Chart at a Glance: China Activity Gauges – Still Sliding Down

Source: Bloomberg LP.

1 We believe PMIs are a better indicator of the health of the Chinese economy than the gross domestic product (GDP) number, which is politicized and is a composite in any case. The manufacturing and non-manufacturing, or service, PMIs have been separated in order to understand the different sectors of the economy. These days, we believe the manufacturing PMI is the number to watch for cyclicality.

Related Insights

Related Insights

06 marzo 2025

20 febrero 2025

16 enero 2025

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.

05 diciembre 2024

"Trump Trade 2.0" impulsó los repuntes de las acciones estadounidenses y los activos digitales, mientras que los activos reales se tambalearon debido a un dólar fuerte, con los mercados mundiales reaccionando de forma desigual a las políticas favorables al crecimiento.