EM Inflation - Memes and Themes

09 August 2022

Read Time 2 MIN

Summary

There are finally signs of disinflation in some EMs, but for the majority it is still “hike, baby, hike”.

EM Disinflation

It’s a “The Eagle Has Landed” and “Elvis Has Left the Building” morning in Brazil. Headline inflation dropped a bit more than expected to 10.07% year-on-year, which means that the country is now officially in disinflation zone. Tax cuts definitely helped, but the Brazilian central bank did an amazing job, responding to rising price pressures early and aggressively – and we are now seeing the results. Brazil’s real rates adjusted by expected inflation are among the highest in emerging markets (EM), and they still look reasonably attractive relative to macroeconomic fundamentals.

Fiscal and Monetary Tightening in EM

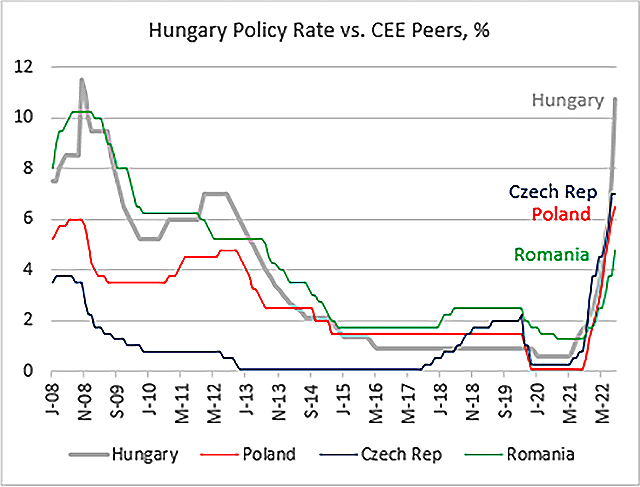

For many other EMs, it’s a “you’re gonna need a bigger boat”… sorry, a bigger rate hike story. Let’s start with Hungary, where annual headline inflation unexpectedly jumped to 13.7%. There are legitimate concerns about an H2 growth “cliff” in the region, but we are not seeing it yet in Hungarian high-frequency data (take, for example, July’s super-strong manufacturing survey of 57.8). Authorities are firing on all cylinders – doing both fiscal adjustment and aggressive monetary tightening – but today’s inflation release signals that it is too early to stop.

Inflation Persistence

Back in LATAM, Mexico’s upside surprise was not huge, but with annual headline inflation rising above 8% and core inflation above 7.6%, a 75bps rate hike on Thursday would be a very good idea indeed. Chilean July CPI was also higher than expected, accelerating to 13.1% year-on-year, and driven in part by fiscal measures aimed at supporting consumption in a high-inflation environment. So, it’s “hike, baby, hike” for the central bank, and the latest minutes clearly signaled more tightening going forward. Stay tuned!

Chart at a Glance: Central Europe Policy Rates - Different Speed

Source: Bloomberg LP

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.