EM Institutions and Markets

08 December 2022

Read Time 2 MIN

LATAM Politics

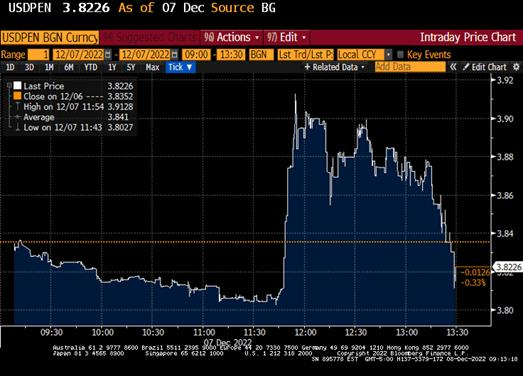

Very often when we talk about institutional frameworks in emerging markets (EM), it is in a context of their weakness, which can lead to deteriorating economic metrics, rating downgrades, and a loss of investor confidence. But there are other – much more encouraging – examples (which can also create interesting trade opportunities). Take yesterday’s “lunchtime” coup attempt in Peru. President Pedro Castillo (who is now ex-President) tried to avoid impeachment by unlawfully dissolving the congress. But the congress had none of it, impeaching Castillo anyway, and putting him in jail. The line of succession was clear, and by the early-afternoon Peru had the first ever female president, Dina Boluarte. The currency – which sold off initially – ended up stronger against the U.S. Dollar (see chart below), and the central bank matter-of-factly delivered a 25bps “farewell” policy rate hike. The end.

EM Rate Cuts

Institutional constraints also allowed the Brazilian central bank to remain on hold yesterday – instead of delivering a “warning shot” rate hike to address new administration’s fiscal expansion plans. President-elect Lula’s grand (populist) vision for social spending underwent a reality check in the parliament, and the market responded by pricing out some rate hikes on a 6-month horizon. Fiscal risks are still here – they featured prominently in the central bank’s statement, and they can delay 2023 rate cuts. As of this morning, the local swap curve was seeing no policy easing until September 2023 (compared to March/May 2023 before the elections runoff).

EM Disinflation

Institutions is a major discussion topic in Mexico and Hungary, but today’s market focus was on inflation. It looks like Mexico is finally on the disinflation track – with both core and headline bi-weekly inflation much lower than expected at the end of November. This should allow the central bank to safely slow the pace of rate hikes (to 50bps at the next meeting in a few days). Hungary’s case is more complicated. Headline inflation accelerated above consensus in November (to 22.5% year-on-year), and it is now set to get even higher in December (peaking at 25-26%) after the removal of gasoline price caps. The caps removal can actually be beneficial for Hungary’s budget (and for bonds’ technicals), but it is also essential that the central bank maintains a hawkish policy stance until inflation starts rolling over in 2023. Stay tuned!

Chart at a Glance: EM Asset Prices (Peruvian Sol) – The Importance of Being Nimble

Source: Bloomberg LP.

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.