Hawks vs. Growth Headwinds

28 July 2022

Read Time 2 MIN

Fed Hikes, U.S. Recession

The below-consensus Q2 GDP print in the U.S. (0.9% sequential contraction) came on the heels of yesterday’s 75bps rate hike by the U.S. Federal Reserve (Fed) and Chairman Jerome Powell’s hawkish press-conference, at which he mentioned a possibility of another “unusually large” move in September. This is a reminder that the Fed is willing to tolerate a recession in order to bring inflation down. Incidentally, the U.S. is among the countries with the sharpest cuts in the 2022 and 2023 growth forecasts in the just-updated World Economic Outlook (IMF).

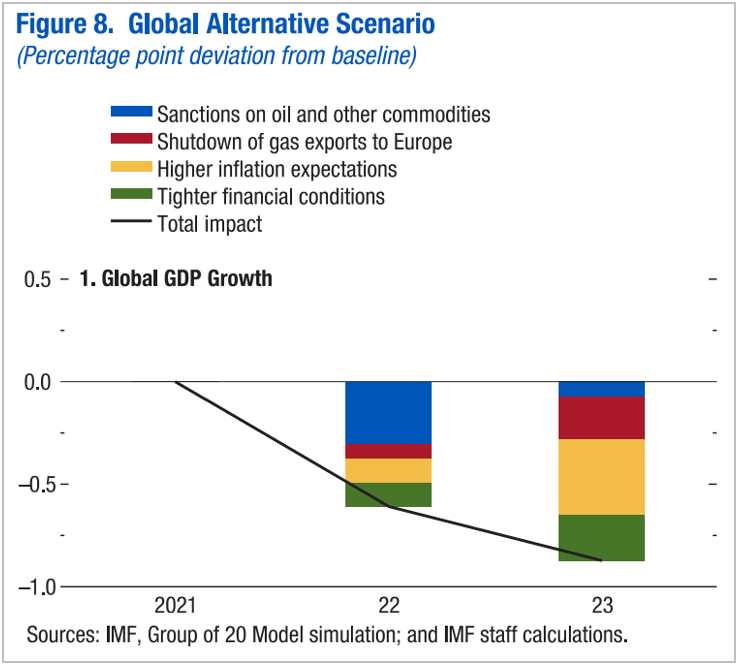

Global Growth Headwinds

The IMF believes that the global balance of risks is squarely to the downside due to a combination of the Russia/Ukraine war’s impact on gas prices, higher inflation and higher costs of disinflation and tighter financial conditions. The new 2022 world GDP forecast is 0.4% lower than April’s projection, and the 2023 forecast was cut by 0.7%. An adverse scenario sees even deeper cuts in global growth projections (see chart below). What was a bit surprising is that the downward revision of the growth forecasts for emerging markets (EM) as a whole was relatively small. In part, this might be due to the fact that parts of EM are expected to benefit from higher commodity prices – these are some Middle Eastern economies and LATAM.

China Growth Slowdown

China, however, is not that lucky. The IMF thinks that the Chinese economy will expand only by 3.3% in real terms this year, which is 1.1% lower than the April estimate. China’s 2023 forecast was cut by 0.5%, to 4.6%. Both numbers are significantly lower than the official growth target of about 5.5%. This is why the market keeps a very close eye on new policy initiatives that could potentially reverse the negative impact of the past – growth-negative – policy initiatives (this sounds like circular reasoning, but…). The central bank’s intention to create a bailout fund (up to CNY1T) to give low-interest loans to real estate developers so that they can complete unfinished apartments (“diffusing” the mortgage payers’ strike in the process) looks promising. But we also learned today that the Politburo was not too keen on aggressive stimulus. Near-term, our focus is on the July batch of China’s activity surveys (out this weekend), which will show whether the economy (especially consumption) enters Q3 in a meaningfully better shape or whether the improvement is still marginal. Stay tuned!

Chart at a Glance: What’s Behind Adverse Growth Scenarios

Source: International Monetary Fund, World Economic Outlook Update, July 2022

Related Insights

Related Insights

06 marzo 2025

20 febrero 2025

16 enero 2025

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.

05 diciembre 2024

"Trump Trade 2.0" impulsó los repuntes de las acciones estadounidenses y los activos digitales, mientras que los activos reales se tambalearon debido a un dólar fuerte, con los mercados mundiales reaccionando de forma desigual a las políticas favorables al crecimiento.