Low Rates – The Natural Order of Things?

20 April 2023

Read Time 2 MIN

Natural Rates

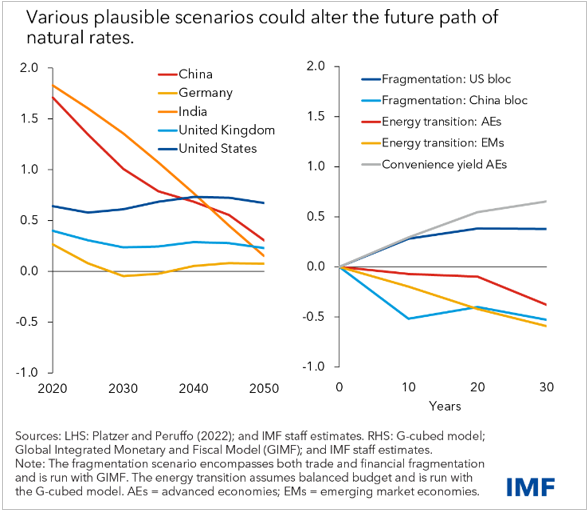

The markets are getting increasingly accustomed to the prospect of a 25bps U.S. rate hike in May (90% implied probability as of this morning). Meanwhile, the IMF published an interesting report in which it argues that the current spike in real interest rates is likely to prove temporary, and interest rates are set to return to the pre-pandemic levels – once inflation is under control, of course. It is reassuring that the report also talks about alternative scenarios (see chart below), including the rising public debt, “green transition,” and de-globalization. Another important factor is emerging markets (EMs) ability – and willingness – to invest their surplus dollars into developed markets (DM) instruments. Many EMs already showed interest in high-quality EM instruments as potential reserve assets. EMs are also eager to accumulate reserve gold, and EMs’ domestic savings will be increasingly spent to finance the “green transition.”

Rate Cuts

Talking about lower rates, some EM central banks are getting antsy – despite various warnings about premature policy moves/communications. The Hungarian central bank tested the waters yesterday with comments about potential near-term easing, and the central bank of Uruguay surprised with a 25bps “proper” policy rate cut. Judging by the Hungarian forint’s reaction, the market is not yet ready to talk about policy easing in that part of the world, given that both core and headline inflation is still in their 20s. Uruguay’s move did not produce a lot of optimism either, even though the real policy rate is high, and both core and headline inflation are on their way down (and much lower than in Hungary). There are concerns that inflation expectations might prove stickier than expected, while mega-drought in neighboring Argentina poses obvious risks to food prices.

Disinflation

Most EMs are not yet ready to take the easing plunge. The Chilean central bank’s minutes sounded very hawkish, talking about upside surprises in both inflation and domestic demand and saying there are not enough signs that inflation is indeed converging to the target. Central banks in EM Asia might be better positioned to pause and eventually cut rates safely, as inflation generally peaked at much lower levels, and food prices are moderating at a faster pace. Malaysia’s central bank left the door open for another hike at its last meeting, but today’s downside inflation surprise (3.4% year-on-year in March) should reassure monetary authorities that the pause can be extended without jeopardizing the disinflation progress. Stay tuned!

Chart at a Glance: Future Interest Rates – Alternatives Matter

Source: International Monetary Fund.

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.