Major Narratives Still Intact

31 March 2023

Read Time 2 MIN

Global Drivers for EM Assets

The last day of March brought more signs that two major market narratives are still in play. The global inflation momentum continues to moderate (albeit with some nuances – like stickier than expected core inflation in Europe and some emerging markets (EM)), while China’s recovery keeps gaining traction. This is good news for EMs – as some are more correlated with the U.S. Federal Reserve’s rate cycle and others are more correlated with China’s rebound/growth cycle.

China Recovery

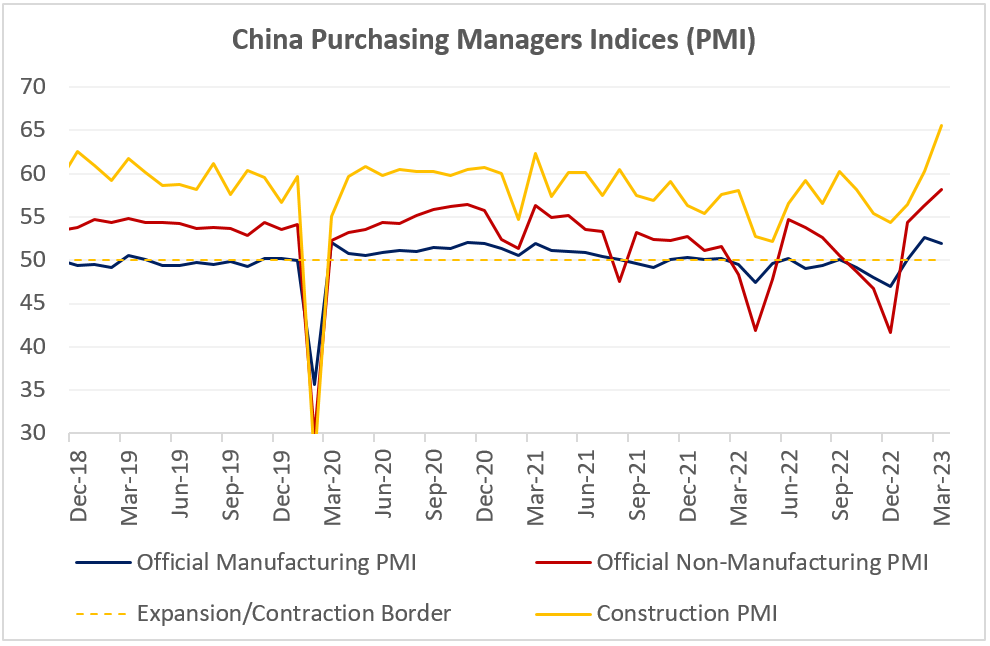

China’s latest domestic activity gauges (Purchasing Managers Indices) support the consensus optimism regarding this year’s growth outlook (5.3% - above the official growth target of about 5%). Key PMI components stayed in expansion zone, with some showing sizable improvements – including services and construction (see chart below). The surging construction PMI reflects a concerted effort to boost infrastructure investments, but could also be indicative of the stabilizing housing sector (which, in turn, a major supporting factor for consumer confidence). The release, however, showed that external growth headwinds might be getting stronger – tighter lending conditions in developed markets (DM) is one obvious avenue – which is why we expect the “supportive yet restrained” policy stance to remain unchanged for now. We also would like to remind that authorities responded very quickly to potential contagion risks associated with the banking mini-crisis in DMs in the middle of the month (in the form of an earlier than expected cut in the reserve requirements for banks).

EM Peak Rates

China’s rebound could create additional inflation pressures going forward – for example, via commodity prices. Global uncertainties like this widen the range of potential growth and inflation outcomes, and this is a reason that keeps various EM central banks on the cautious side as regards policy easing, even when inflation had already peaked. The Colombian central bank stated yesterday that policy stance will remain restrictive for some time, and the Mexican central bank indicated that the balance of inflation risks is still biased to the upside. Both central banks delivered the expected 25bps rate hikes yesterday, and the market thinks that another small “farewell” hike might still be on the table. Stay tuned!

Chart at a Glance: China Activity Gauges Support Optimistic GDP Forecasts

Source: Bloomberg LP.

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.