Rate Cuts and Sanity Checks

19 April 2023

Read Time 2 MIN

Rate Cuts Expectations

Last week in DC, the IMF repeatedly cautioned against premature rate cut communications, but the Hungarian central bank either did not listen carefully, or decided to check what happens anyway. The currency (the Hungarian forint) had a very adverse reaction to an early rate cut suggestion from the deputy governor, weakening the most against the U.S. Dollar compared to emerging markets (EM) peers (as of 10:00am ET, according to Bloomberg LP). We are not saying that the IMF is always right, and we realize that some factors (like the mother of all base effects) argue for faster disinflation in H2. Hungary’s case is also quite extreme – we do not see 20%+ headline and core inflation (vs. 3% inflation target) very often in EM these days. Still, the forint’s reaction was a teachable moment, which hopefully got noticed by various EM central banks. High real rates helped to shield many EMs from this year’s market turbulence – and it is not wise to throw this cushion away while there are plenty of bumps on the disinflation road.

EM Disinflation

In fact, it might be prudent for some EMs to raise their policy rates a bit more. This is what the market currently prices in for South Africa, where headline inflation surprised to the upside in March, re-accelerating to 7.1% year-on-year, and core inflation stayed close to a multi-year high of 5.2% year-on-year. The surprise was mostly due to higher food prices - mega-drought in Argentina, as well as a rising probability of El Nino this year can create headwinds for disinflation not just in South Africa but in wider EM in the coming months.

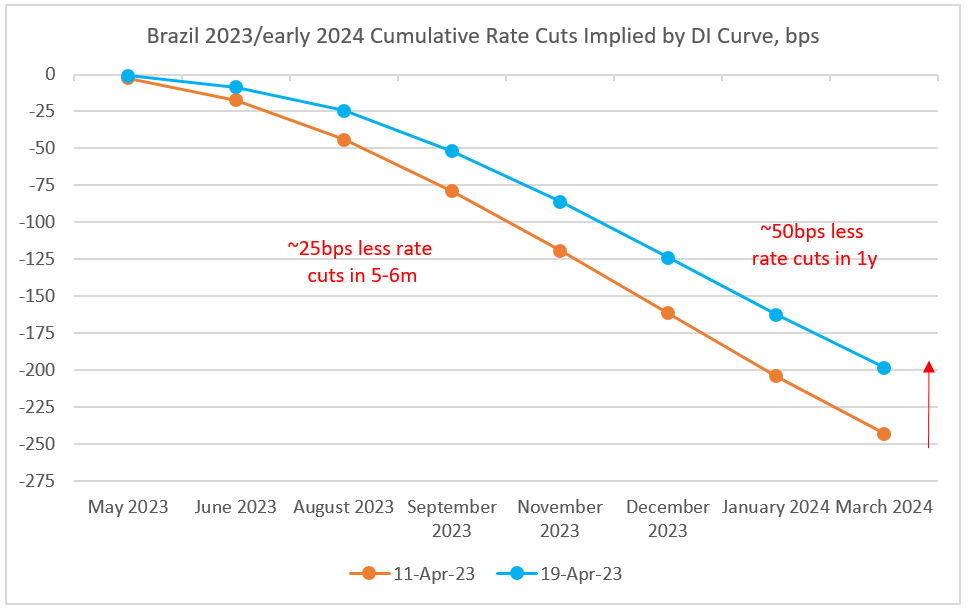

LATAM Fiscal Outlook

Sanity checks for EM rate cuts can also come from the fiscal side. The market continued to adjust its expectations for policy easing in Brazil in 6-12 months, as it received the final version of the government’s new fiscal framework. Many details of the plan were known before, but the document confirmed that the new framework is more convoluted and less enforceable. There is also a lot of uncertainty about generating additional revenue to meet the primary fiscal targets (which might not necessarily stabilize the debt/GDP ratio). So, even though Brazil’s real policy rate is the highest among major EMs (around 8.7%), the local swap curve priced out about 50bps of implied rate cuts on a 1-year horizon within the past week (see chart below). It is not the end of Brazil’s easing story, but fiscal certainly is key for a big breakthrough. Stay tuned!

Chart at a Glance: Brazil’s Policy Easing Room – Fiscal Certainty Is Key

Source: Bloomberg LP.

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.