Rate Cuts – On the Chopping Block?

04 April 2023

Read Time 2 MIN

EM Policy Rate Expectations

Various emerging markets (EM) central banks continue to signal that while they are happy to end their tightening cycles, the bar for rate cuts is still high. The latest monetary policy communications in the Czech Republic, Hungary, Brazil, Malaysia and Thailand were surprisingly hawkish. The Bank of Thailand signaled more tightening as the economy continues to rebound. The Czech National Bank explicitly warned the market against “premature” bets on rate cuts, even suggesting that that policy rate might not have peaked yet. The Malaysian central bank cautioned that we are “not out of the woods on inflation”, and South Africa actually re-accelerated the pace of tightening last month.

EM Disinflation

The market seems to be OK with the “rate cuts delayed” narrative, seeing no noticeable easing until Q4 (see chart below). Uncertainty about global growth and the impact of geopolitics/China’s rebound on commodity prices are good reasons for being vigilant. Uneven or slower than expected disinflation also argues for policy caution. Sticky core inflation/inflation expectations are a problem for many central bankers – South Korean inflation prints for March illustrate this point really well. Some board members would prefer inflation to get closer to the target range (or the current benchmark rate) before initiating rate cuts – this was a message from the Romanian central bank earlier today, and we might hear similar undertones from the Chilean central bank in the afternoon.

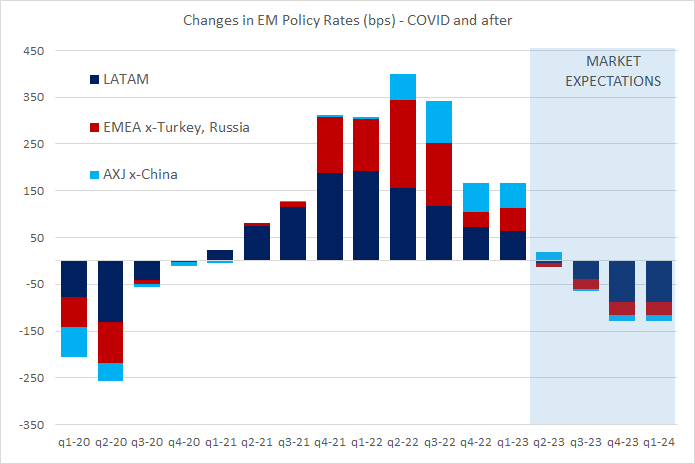

EM Rate Cuts

Some factors, however, might pave the way for earlier/larger rate cuts. Real policy rates based on expected inflation are getting really high in some EMs, threatening the growth outlook in a situation when fiscal space is getting more limited. The pace of fiscal adjustment is key here (as this might affect inflation expectations) – with Brazil being a prime candidate for the policy rate re-pricing, if the new fiscal framework is deemed credible. We also keep an eye on “the mother of all base effects” that should have a stronger anti-inflation impact in the coming months. Finally, EM FX spectacular performance so far this year can also speed up disinflation, easing pressure on EM central banks and opening more room for rate cuts. Stay tuned!

Chart at a Glance: EM Rate Cuts – No Rush For Now

Source: VanEck Research; Bloomberg LP.

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.