EM’s Policy Cushions and Fear of Unknown

25 April 2023

Read Time 2 MIN

Growth in China, U.S.

The U.S. debt ceiling debacle continues to drive some market segments (see chart below), but a big question for emerging markets (EM) folks is which countries might be shielded by a faster recovery in China if U.S. recession concerns stage a comeback (a scenario under which there is no resolution before the debt ceiling is reached). Various sell-side estimates suggest that Indonesia, South Korea, Thailand, Brazil and Poland might be in a stronger position, whereas the Philippines, Mexico, Turkey and Hungary could face more headwinds.

Policy Easing

This configuration sheds a new light on the inaugural rate cuts in EM, including Hungary’s decision to lower the Lombard rate (top range of the interest rate corridor) from 25% to 20.5% this morning. The market’s reaction was much calmer than last week’s currency meltdown, because the key rate remained unchanged at 18%, giving the central bank more time/space to evaluate the disinflation progress (which is expected to accelerate in the summer).

EM External Balances

EMs with less exposure to the U.S. growth downside might also benefit from the fact that their external balances are either already strong (current accounts in Indonesia and Thailand flipped to surplus last year) or started adjusting (Poland). Brazil’s basic balance (current account and foreign direct investments) also looked rock-solid in March, providing fundamental support for the currency and making it easier for the central bank to start rate cuts, once the fiscal path is clear. Stay tuned!

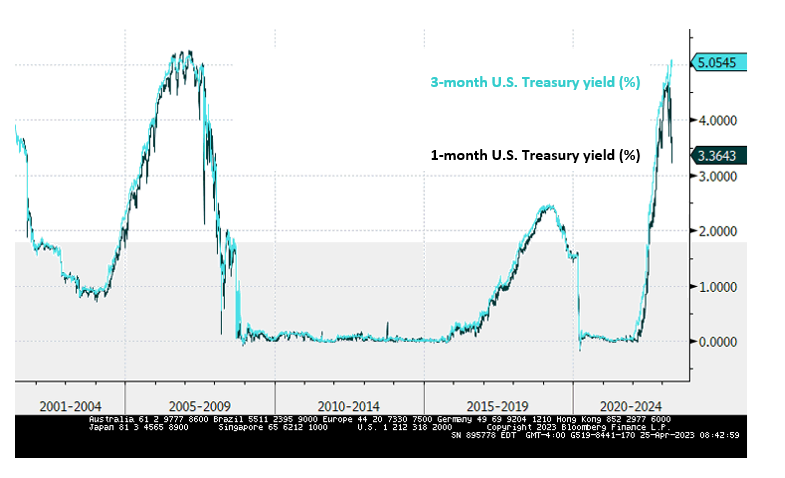

Chart at a Glance: U.S. Debt Ceiling Fear In Two Lines

Source: Bloomberg LP.

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.