Ausgaben im Spiel: Revolutionierung der Einnahmen aus Videospielen

24 November 2020

Lesezeit 4 MIN.

Wer hätte geahnt, dass ein kostenloses Spiel in einem einzigen Jahr mehr Geld einbringen würde als jedes andere Videospiel? Genau das ist dem Spiel Fortnite gelungen, das 2018 rund 2,4 Milliarden USD einbrachte. Es ist ein prominentes Beispiel dafür, wie In-Game-Käufe, also Ausgaben innerhalb des Spiels, die Videospiele-Landschaft revolutioniert haben.

Beim traditionellen Geschäftsmodell – „Game as a Product“ (GAAP) genannt – entwickelt ein Spieleherausgeber ein Spiel und verkauft dieses dann gegen eine einmalige, Umsatz generierende Gebühr an den Verbraucher. Nachdem der Verbraucher das Spiel gekauft hat, muss der Herausgeber ein anderes Videospiel oder ein sogenanntes Add-on zur Erweiterung des bestehenden Spiels entwickeln, um zusätzliche Umsatzerlöse mit diesem Verbraucher zu erwirtschaften.

Mitte der 2000er Jahre begannen Videospiele-Herausgeber, das „Game as a Service“-Modell zu testen. Dabei entfallen für den Verbraucher die anfänglichen Kosten für den Kauf des Spiels – stattdessen zahlt er fortlaufend Gebühren, damit er das Spiel weiter nutzen und auf den gewünschten Content zugreifen kann. Der Spieleherausgeber kann mit diesem Modell auf verschiedene Arten Umsatz generieren, u. a. über Spieleabos, Mikrotransaktionen und sogenannte Season Passes. Wenngleich die Transaktionen beim Service-Modell möglicherweise geringere Beträge lukrieren, eröffnet das Modell dem Herausgeber die Möglichkeit, den Zeitraum, in dem Verbraucher Käufe für ein Spiel tätigen, endlos auszudehnen und so den mit einem einzelnen Spiel erzielten Gesamtumsatz zu steigern.

Dieses Geschäftsmodell dient aus Sicht des Herausgebers drei wichtigen Zwecken. Es verlängert den Lebenszyklus von Spielen, die von Verbrauchern gespielt werden, es erhöht das maximale Umsatzpotenzial von einem einzelnen Verbraucher und es senkt die Hürde für neue potenzielle zahlende Kunden, das Spiel auszuprobieren, bevor sie sich für einen Kauf entscheiden. Die Herausgeber nutzen dieses neue Modell als eine Möglichkeit, um das Umsatzwachstum zu fördern. Allerdings passen die verschiedenen Herausgeber ihre Strategie für In-Game-Käufe je nach ihrem spezifischen Produktangebot an. Activision Blizzard und Take-Two Interactive haben jeweils sehr unterschiedliche Ansätze zur Umsetzung dieses Geschäftsmodells gewählt.

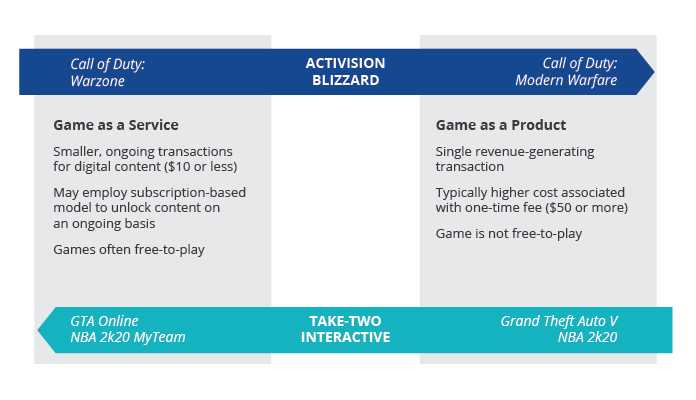

Zwei unterschiedliche Ansätze zum „Game as a Service“-Modell

Die Infografik wurde zu Illustrationszwecken vereinfacht.

Activision Blizzard: Von kostenlos auf Premium

Blizzard Entertainment (jetzt ein Geschäftsbereich von Activision Blizzard) war einer der Pioniere dieses neuen Umsatzmodells. Der Spielentwickler brachte 2004 World of Warcraft, ein MMORPG (Massively Multiplayer Online Role-Playing Game), auf den Markt, das Spielern die Möglichkeit bot, ein monatliches, fortlaufendes Abonnement zu erwerben, um Zugang zum vollständigen, freigeschalteten Spiel zu erhalten. Derzeit setzt Activision Blizzard das Modell zur Generierung von In-Game-Umsätzen in einer Reihe von verschiedenen Spielen und Plattformen ein.

Call of Duty: Warzone ist ein kostenloses Spiel, das seit seiner Herausgabe im ersten Quartal 2020 von mindestens 75 Millionen Menschen auf der ganzen Welt heruntergeladen und gespielt wurde.

- Warzone dient als eigenständige Einnahmequelle durch sein Battle-Pass-Abonnement und das Angebot digitaler Gegenstände (wie Felle und Waffen).

- Warzone dient auch als eine Art kostenloser Test für die Spieler, die sich dann möglicherweise das ganze Spiel von Call of Duty: Modern Warfare im Rahmen des herkömmlichen „Game as Product“-Modells kaufen.

- Im Ergebnisbericht von Activision für das zweite Quartal 2020 stellte das Unternehmen fest, dass durch Modern Warfare (die kostenpflichtige Version) „mehr Spieler außerhalb eines Einführungsquartals für das Premium-Call-of-Duty-Erlebnis gewonnen wurden als jemals zuvor, wobei die Mehrheit durch Upgrades aus Warzone hinzukam“.1

- In diesem Beispiel hat Activision Blizzard erfolgreich ein kostenlos spielbares Spiel (Warzone) eingesetzt, um Millionen neuer Spieler anzuziehen, was wiederum die Verkäufe ihres Premium-Spiels (Modern Warfare) unter dem traditionellen „Game as a Product“-Paradigma steigerte.

Take-Two Interactive: Vom Produkt zum Service

Take-Two Interactive prägte den Begriff „wiederkehrende Verbraucherausgaben“ und definiert ihn als Einnahmen, die aus der dauerhaften Verbraucherbindung generiert werden, einschließlich virtueller Währung, Zusatzinhalten und In-Game-Käufen. Diese Einnahmequellen sind speziell gruppiert, so dass der anfängliche Spielkauf ausgeschlossen ist.

Laut Take-Two stiegen die wiederkehrenden Verbraucherausgaben um 52% und machten 58% des gesamten GAAP-Nettoumsatzes zum Zeitpunkt des Quartalsberichts für das erste Quartal 2021 aus.2 „Die größten Beiträge zum GAAP-Nettoumsatz im ersten Quartal 2021 waren auf Grand Theft Auto® Online und Grand Theft Auto V; NBA® 2K20; Red Dead Redemption 2 und Red Dead Online zurückzuführen.“3

- Wiederkehrende Verbraucherausgaben machen nun den Großteil des Nettoumsatzes von Take-Two aus, was darauf hindeutet, dass das Unternehmen weiterhin Content und Spiele veröffentlichen wird, die In-Game-Käufe generieren können.

- Grand Theft Auto V wurde 2013 auf den Markt gebracht, ist aber immer noch die wichtigste Einnahmequelle für das Unternehmen. In diesem Fall kauften die Verbraucher zuerst das Spiel (Game as a Product) und hatten dann die Möglichkeit, weitere Käufe innerhalb des Spiels zu tätigen (Game as a Service).

Videospiele und Esports: Medien und Unterhaltung auf die nächste Stufe bringen

Activision und Take-Two haben im Wesentlichen entgegengesetzte Ansätze für das „Game as a Service“-Modell gewählt. Die Veröffentlichung eines kostenlos spielbaren Spiels durch Activision trägt dazu bei, die Verbraucher zum Kauf eines traditionellen Spiels zu bewegen, während Take-Two einen Vorabkauf des Spiels erfordert, bevor die Verbraucher mehr für Dinge innerhalb des Spiels ausgeben können.

Wiederkehrende Ausgaben innerhalb des Spiels gehören zu den Trends, die das Wachstum der Videospielbranche vorantreiben und diesen Bereich unserer Ansicht nach zu einer überzeugenden Investitionsmöglichkeit machen.

1Quelle: Ergebnisbericht von Activision Blizzard für das zweite Quartal 2020

2Take-Two Interactive Software, Ergebnisbericht für das erste Quartal 2021

3ebd.

Wichtige Hinweise

Ausschließlich zu Informations- und/oder Werbezwecken.

Diese Informationen stammen von VanEck (Europe) GmbH, die von der nach niederländischem Recht gegründeten und bei der niederländischen Finanzmarktaufsicht (AFM) registrierten Verwaltungsgesellschaft VanEck Asset Management B.V. zum Vertrieb der VanEck-Produkte in Europa bestellt wurde. Die VanEck (Europe) GmbH mit eingetragenem Sitz unter der Anschrift Kreuznacher Str. 30, 60486 Frankfurt, Deutschland, ist ein von der Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) beaufsichtigter Finanzdienstleister. Die Angaben sind nur dazu bestimmt, Anlegern allgemeine und vorläufige Informationen zu bieten, und sollten nicht als Anlage-, Rechts- oder Steuerberatung ausgelegt werden. Die VanEck (Europe) GmbH und ihre verbundenen und Tochterunternehmen (gemeinsam „VanEck“) übernehmen keine Haftung in Bezug auf Investitions-, Veräußerungs- oder Retentionsentscheidungen, die der Investor aufgrund dieser Informationen trifft. Die zum Ausdruck gebrachten Ansichten und Meinungen sind die des Autors bzw. der Autoren, aber nicht notwendigerweise die von VanEck. Die Meinungen sind zum Zeitpunkt der Veröffentlichung aktuell und können sich mit den Marktbedingungen ändern. Bestimmte enthaltene Aussagen können Hochrechnungen, Prognosen und andere zukunftsorientierte Aussagen darstellen, die keine tatsächlichen Ergebnisse widerspiegeln. Es wird angenommen, dass die von Dritten bereitgestellten Informationen zuverlässig sind. Diese Informationen wurden weder von unabhängigen Stellen auf ihre Korrektheit oder Vollständigkeit hin geprüft noch können sie garantiert werden. Alle genannten Indizes sind Kennzahlen für übliche Marktsektoren und Wertentwicklungen. Es ist nicht möglich, direkt in einen Index zu investieren.

Alle Angaben zur Wertentwicklung beziehen sich auf die Vergangenheit und sind keine Garantie für zukünftige Ergebnisse. Anlagen sind mit Risiken verbunden, die auch einen möglichen Verlust des eingesetzten Kapitals einschließen können. Sie müssen den Verkaufsprospekt und die KID lesen, bevor Sie eine Anlage tätigen.

Ohne ausdrückliche schriftliche Genehmigung von VanEck ist es nicht gestattet, Inhalte dieser Publikation in jedweder Form zu vervielfältigen oder in einer anderen Publikation auf sie zu verweisen.

© VanEck (Europe) GmbH

Verwandte Einblicke

06 September 2022