Welcome to VanEck

Select Investor Type

05 August 2020

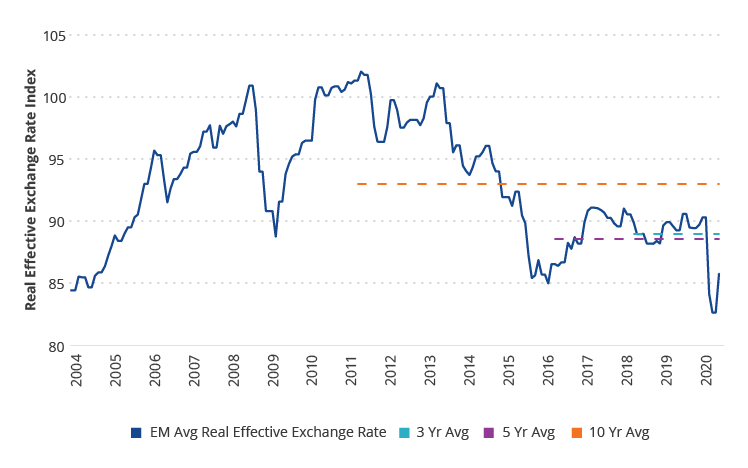

Emerging markets currencies (“EMFX”) have depreciated sharply against the U.S. dollar this year, with valuations near historical lows. Although off the lowest levels of March when returns were -15% for the year, EMFX has still detracted approximately 9% from emerging markets local currency bond returns year to date as of 27 July, 2020, more than offsetting the positive return driven by local interest rates. We expect that EMFX will be the dominant driver of returns for the remainder of the year, and although further volatility is expected, we believe there is a strategic case for an EMFX recovery even though timing can be nearly impossible to predict. Recent technical weakness of the U.S. dollar against developed markets currencies may also make EMFX attractive from a tactical standpoint, and the yields provided by emerging markets local currency bonds may make the asset class an attractive way to gain exposure.

Source: VanEck and J.P. Morgan as of 30/06/2020. Emerging Markets Average Real Effective Exchange Rate refers to the average of a country's currency relative to an index or basket of other currencies.

A return to growth is a prerequisite for prolonged EMFX recovery. Policymakers in many emerging markets have taken drastic fiscal and monetary policy actions, including lowering interest rates and implementing quantitative easing style measures for the latest updates). Although not directly supportive of currencies, prioritizing growth is more important in the longer term and that would be supportive of EMFX. China’s remarkable economic recovery may also boost EMFX returns, both because of the recent inclusion of CNY in emerging markets local currency bond indices, and because of the broader economic impact on supply chains and commodity demand globally. Importantly, central banks have a variety of both conventional and unconventional tools at their disposal. Emerging markets bond fund flows have been sharply negative since February, but signs of recovery and a shift in sentiment could also result in a reversal that may provide further support to currencies.

There are many risks to this outlook, most importantly a resurgence in COVID-19 cases globally or failure to find an effective vaccine. Further fiscal deterioration beyond what is already priced in is also possible. One silver lining is that there is also a natural adjustment that takes place when a currency weakens that can help to stabilize an emerging market’s balance of payments and help to mitigate further capital flight.

On the domestic side, there are many reasons why U.S. dollar strength may not continue. Record deficits and economic contraction make the prospect of higher U.S. interest rates highly unlikely for the foreseeable future. To the extent that foreign investors lose confidence in the U.S. dollar or seek to diversify their exposure, the U.S. dollar may weaken broadly. However, the U.S. dollar can exhibit strength for extended periods despite these headwinds, because ultimately we believe it is still “the” safe haven asset, and support may be driven by external factors as much as the internal economic position of the U.S.

Nevertheless, in our view valuations remain extremely cheap, and we believe that emerging markets local currency bonds can provide diversification in a global bond portfolio. Recent U.S. dollar weakness may also begin to be reflected in EMFX. Tactical or strategic exposure through emerging markets local currency bonds via an ETF may be attractive because of the low trading costs and high liquidity. At the same time, although yields have compressed globally, the yield pickup against developed markets sovereign bonds and U.S. Treasuries has widened, and the asset class continues to provide attractive real interest rates as well.

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

11 December 2025

11 December 2025