China – At the Cusp of Reopening?

11 November 2022

Read Time 2 MIN

China Zero-COVID Policy

The overnight news about China’s easing some COVID restrictions – which came on the heels of a downside inflation surprise in the U.S. – were well received by the market. We saw very nice equity indices gains across the board, and some exceptional FX performance, such as a 427bps gain in the Korean won. China’s measures to “further optimize pandemic control” (a total of 20) are cautious, with the main focus on quarantine times, the frequency of testing and risk area delineations. However, the move sends an encouraging signal regarding China’s near-term growth outlook, especially as regards demand side (services, consumption) and the efficacy of the already approved policy stimulus. The just-announced measures to help struggling property developers came in handy as well.

EM Disinflation

China is the only independent global growth driver in emerging markets (EM), and the positive growth news is flowing at a time when more and more EMs are leaving peak inflation behind. Today’s downside inflation surprise in Romania is just another example. Disinflation should free up some policy space to deal with softer growth in the rest of EM, but it does not necessarily mean that (all) EMs will stop tightening, as inflation is still too far from the targets in most places and inflation expectations are elevated as well. This was the message sent by central banks in Mexico and Peru yesterday. The market sees at least 125bps more rate hikes in Mexico in the next six months, before there is any room for policy easing.

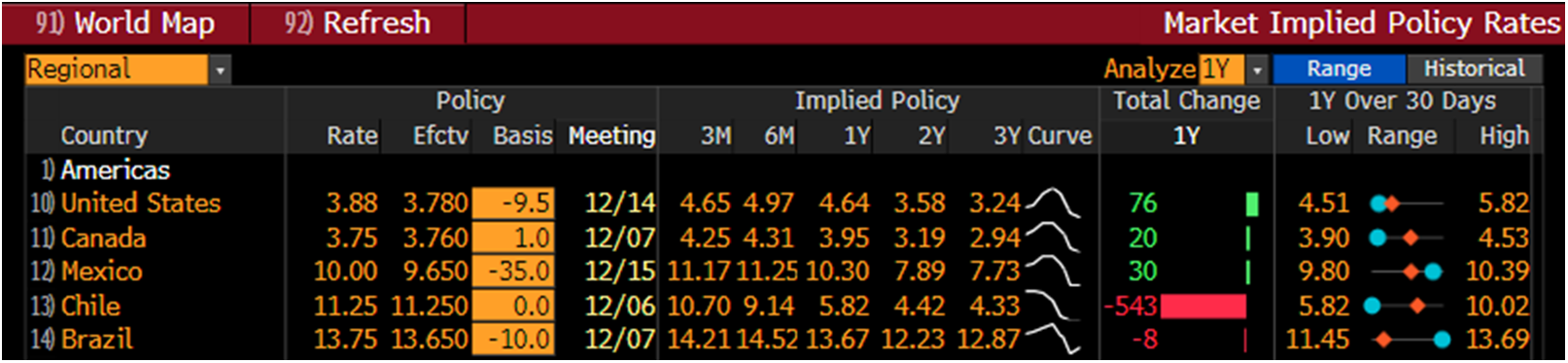

EM Rates and Fiscal Policy

The pace of easing in EM could also be determined by the policy agenda – especially on the fiscal front. This is what drives the market expectations for the policy rate in Brazil right now (and probably makes the central bank very nervous, as well). Brazil’s swap curve was pricing some sizable rate cuts (~186-200bps) on a 1-year horizon going into the presidential elections runoff. The 1-year expectations have been adjusted to a mere -8bps in the past week (see chart below), with the market adding nearly 50bps of rate hikes between now and March. These abrupt changes reflect investors’ concerns about President-elect Luiz Inácio Lula da Silva’s spending plans, as well as the composition of his transition economic team. Stay tuned!

Chart at a Glance: Brazil’s Rapidly Shrinking Space for Rate Cuts

Source: Bloomberg LP

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.