EM Disinflation – Another Success Story?

01 November 2022

Read Time 2 MIN

Global Peak Inflation

We continue to get upside inflation surprises across the globe, but the peak inflation drumbeat is getting stronger. The disinflation poster kid in emerging markets (EM) is, undoubtedly, Brazil – headline inflation is now in single digits, and, importantly, the price diffusion index is also getting lower (=price pressures are not as widespread as before). Still, the central bank minutes made it very clear that irresponsible fiscal policy may affect inflation and risk premia and that the board would not hesitate to hike again if something goes wrong with the disinflation process. This is a reminder that President-elect Luiz Inácio Lula da Silva (Lula) should think twice before making any dramatic populist policy U-turns. It would also be nice for the outgoing president Jair Bolsonaro to finally concede so that we all can move on – but this is a separate story.

EM Asia Prices And Growth

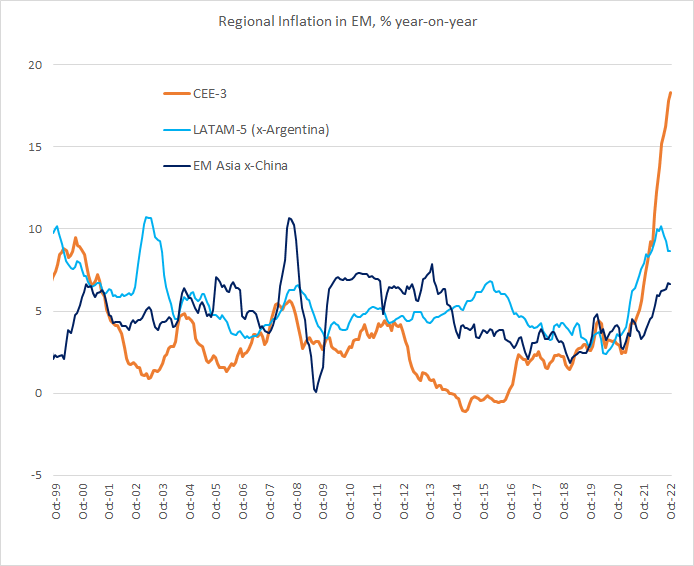

We also watch very intently inflation developments in EM Asia, which might be able to escape the high inflation curse that plagued most of EMEA and LATAM in the past year and a half. A nascent inflation peak in South Korea should probably survive a small expected uptick in October (out this evening). Today’s inflation print in Indonesia also looked promising – outright headline disinflation and lower-than-expected core prices. If regional prices start moderating at levels well below EM Europe/LATAM (see chart below), this might give central banks more policy room to deal with multiplying growth headwinds. Note that the activity gauges (Purchasing Managers Indices, or PMIs) in South Korea, Malaysia, and Thailand remained in the contraction zone in October.

EM Growth Cliff

The collapse of manufacturing PMIs in Central Europe raises a question about the eventual impact of the growth cliff on regional prices. Right now, ~20% inflation in the region is the new “10%” (see chart below) due to the impact of the Russia/Ukraine war on supply chains and energy/commodity prices. But the manufacturing PMI in the Czech Republic is rapidly approaching the COVID levels (it dropped to 41.7 in October), and we are bracing ourselves for tomorrow’s PMI releases in Hungary and Poland. The Czech national bank is meeting on Thursday – and we’ll see how the growth outlook factors into its policy rate decisions. The consensus expectation is that the pause will be extended at 7%, despite 18% annual headline inflation. Stay tuned!

Chart at a Glance: Inflation in EM Regions – Very Different Patterns

Source: VanEck Research; Bloomberg LP.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.