EM Inflation - Memes and Themes

09 August 2022

Read Time 2 MIN

Summary

There are finally signs of disinflation in some EMs, but for the majority it is still “hike, baby, hike”.

EM Disinflation

It’s a “The Eagle Has Landed” and “Elvis Has Left the Building” morning in Brazil. Headline inflation dropped a bit more than expected to 10.07% year-on-year, which means that the country is now officially in disinflation zone. Tax cuts definitely helped, but the Brazilian central bank did an amazing job, responding to rising price pressures early and aggressively – and we are now seeing the results. Brazil’s real rates adjusted by expected inflation are among the highest in emerging markets (EM), and they still look reasonably attractive relative to macroeconomic fundamentals.

Fiscal and Monetary Tightening in EM

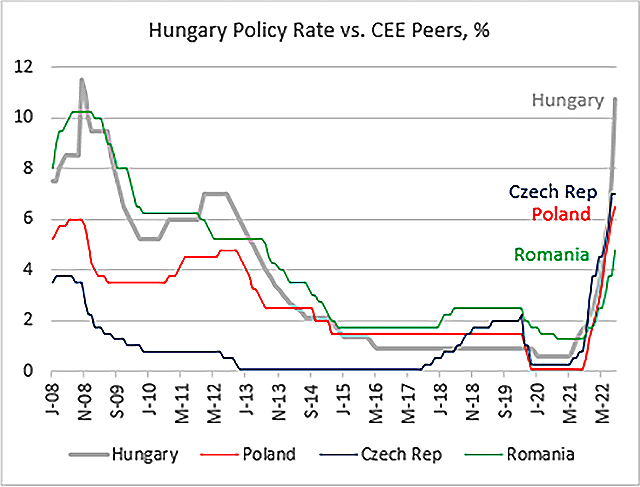

For many other EMs, it’s a “you’re gonna need a bigger boat”… sorry, a bigger rate hike story. Let’s start with Hungary, where annual headline inflation unexpectedly jumped to 13.7%. There are legitimate concerns about an H2 growth “cliff” in the region, but we are not seeing it yet in Hungarian high-frequency data (take, for example, July’s super-strong manufacturing survey of 57.8). Authorities are firing on all cylinders – doing both fiscal adjustment and aggressive monetary tightening – but today’s inflation release signals that it is too early to stop.

Inflation Persistence

Back in LATAM, Mexico’s upside surprise was not huge, but with annual headline inflation rising above 8% and core inflation above 7.6%, a 75bps rate hike on Thursday would be a very good idea indeed. Chilean July CPI was also higher than expected, accelerating to 13.1% year-on-year, and driven in part by fiscal measures aimed at supporting consumption in a high-inflation environment. So, it’s “hike, baby, hike” for the central bank, and the latest minutes clearly signaled more tightening going forward. Stay tuned!

Chart at a Glance: Central Europe Policy Rates - Different Speed

Source: Bloomberg LP

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.