EM Policy Options - To the Drawing Board

11 August 2022

Read Time 2 MIN

Summary

Recent changes in inflation and growth surprises are making emerging markets to re-evaluate their policy options.

EM Inflation, Growth Surprises

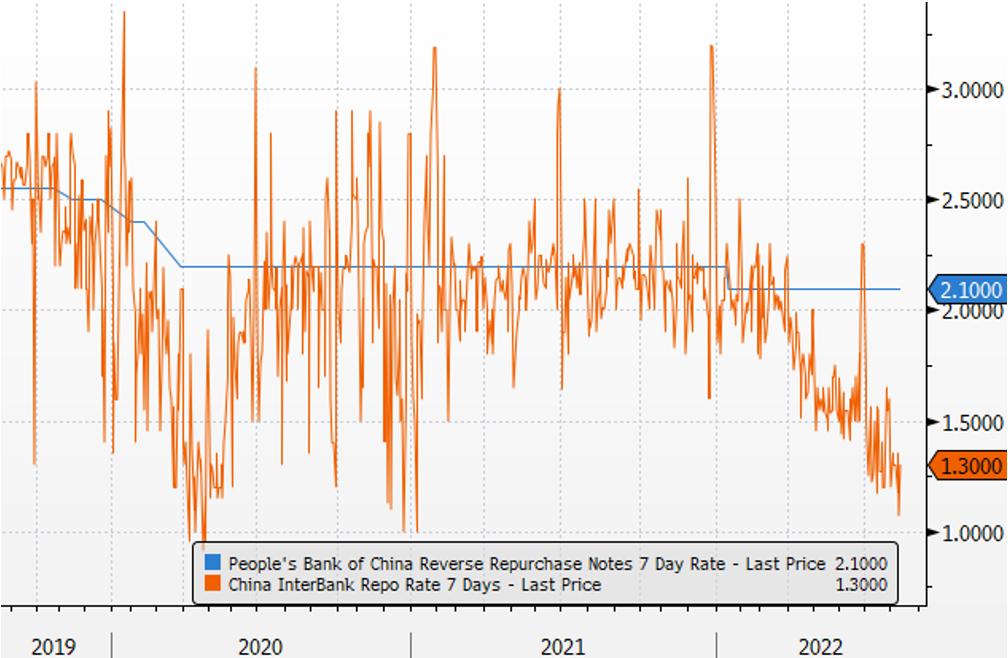

The inflation surprise index for emerging markets (EM) has been going down since May. The growth surprise index appears to be flat lining. It is therefore not surprising that an increasing number of EMs are going back to the drawing board to evaluate their policy options. In China, the central bank’s Q2 monetary policy report signaled that “a wall of liquidity” will not be coming back any time soon, despite benign inflation and multiple near-term growth headwinds (the 2022 consensus GDP growth has been cut to 3.9%). The chart below - with interbank rates well below their benchmark - shows why additional rate cuts might not be a policy option of choice either (there is no point), and why authorities are likely to focus on regulatory changes and fiscal channels.

Growth and Pace of EM Rate Hikes

Near-term growth headwinds might be even stronger in Central Europe, which is exposed to higher energy prices and negative spillovers from its main trading partner, the Eurozone. The Czech National Bank kept the policy rate on hold, opting for FX interventions (about 15% of the international reserves since mid-May, according to some sell-side estimates) to cap inflation pressures. Hungary is actively employing fiscal tightening (a surprising surplus in July) in addition to more aggressive benchmark frontloading. So, today’s decision to keep the 1-week deposit rate unchanged looks perfectly logical in all respects. Finally, today’s minuscule downside surprise in Romanian inflation can give the central bank an excuse to tighten at a slower pace going forward.

LATAM Policy Divergence

The inflation and growth landscapes in LATAM look quite diverse. Brazil is exiting its tightening cycle - and rightly so. But other countries/central banks might need to work harder (=hike more) to leave the inflation peak behind. Mexico’s rate-setting meeting will be closely watched this afternoon. The consensus expects another sizable hike of 75bps, following an upside inflation surprise in July. But the statement will be equally important as regards the balance of risks and especially the central bank’s view on growth risks, because Mexico’s manufacturing survey (Purchasing Managers Index) unexpectedly moved into contraction zone in July (48.5). Stay tuned!

Chart at a Glance: China Interest Rates - Lower Without Policy Rate Cuts

Source: Bloomberg LP

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.