EM Policy Rates – Steady Now!

09 March 2023

Read Time 2 MIN

EM Central Banks On Hold

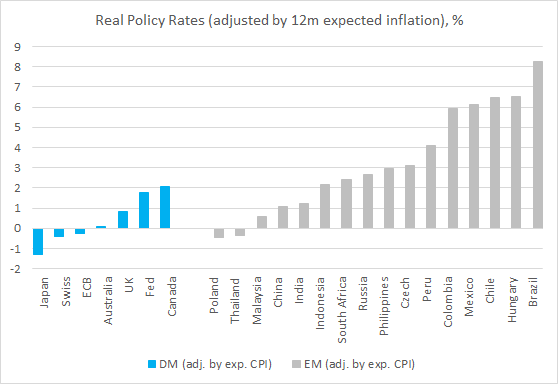

It could have been the shortest emerging markets (EM) daily blog ever. Why are various EM central banks increasingly staying on hold, despite the rising peak rate expectations for the U.S. Federal Reserve and the ECB? Just check the chart below. The End. But, of course, we are not that laconic, so let’s have a closer look. A big takeaway from today’s chart is that EM’s aggressive and timely policy response created an impressive policy cushion – a fundamental “positive” for EM FX, including carry trades (especially against the backdrop of the improving growth outlook). So, even though the U.S. Dollar is up so far this year, several major EM currencies are up (a lot) against the U.S. Dollar. And this creates room for differentiation in the EM space.

EM Disinflation Progress

EM’s disinflation progress is the main driving force here. The high-frequency dataflow can be “jumpy”, but this week’s releases pointed in the right direction – including today’s downside inflation surprise in Mexico. The best part of the release – from the central bank’s point of view in particular – was further moderation in core inflation. The bi-weekly core inflation print looked especially encouraging, easing from 8.38% year-on-year to 8.21%. We don’t think that the Mexican central bank is done hiking yet, but a pause is definitely within reach now. Since we are talking about EM disinflation, we ought to mention China’s surprisingly weak February prints (1% year-on-year vs. 1.9% expected). Even though it might be tempting to interpret them solely as a sign of weak domestic demand, there were several factors – such as seasonality and pork prices (3.8% year-on-year vs. nearly 52% back in October) – that could have led to February’s distortions.

EM External Balances

What else can influence EM’s doves? Well, fiscal consolidation is key, especially in big index names like Brazil. As you can see on the chart below, Brazil’s room for rate cuts is massive in theory – and could increase further if tomorrow’s inflation print meets expectations – but the market needs reassurance about the government’s spending plans and tax reform. We’ll also keep an eye on external balances, as wider current account gaps can increase pressure on FX (and hence on inflation). South Africa’s current account deficit widened more than expected in Q4 (2.6% of GDP), and even though the size is not critical yet, further deterioration might require more action on the central bank’s part. Stay tuned!

Chart at a Glance: EM High Real Rates Create Room For Eventual Rate Cuts

Source: VanEck Research; Bloomberg LP.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.