EM Rate Hikes – Success?

05 April 2023

Read Time 2 MIN

Case for EM Bonds

Emerging markets (EM) central banks’ independence and early (credible) responses to the post-pandemic inflation spike boosted EM real yields and carry, supporting the fundamental case for EM bonds and helping to shield them from recent market turbulence in developed markets (DM). EM’s disinflation progress keeps the pivot hopes alive, but for now most central banks prefer to stay vigilant. And often this means an extended pause – like in the case of the Chilean central bank yesterday (higher rates for longer), or Poland’s national bank this morning.

EM Disinflation

The latest inflation prints in Mexico, Colombia and the Philippines show why many central banks are cautious – even though headline inflation has clearly peaked, core price pressures are much more persistent. Mexico’s core inflation slowed less than expected in March – staying above 8% year-on-year – and services inflation continued to accelerate. Core inflation in Colombia and the Philippines was also in “lift-off” mode – the latter reached a new high since March 1999, leaving room for a small “farewell” rate hike. The market expects to have more clarity on these issues in three to six months, which explains the timing of priced-in “inaugural” EM rate cuts. A comment from Poland’s central bank Governor Adam Glapinski also drew attention to the disinflationary impact of stronger EM currencies, which might help to bring easing forward in some countries.

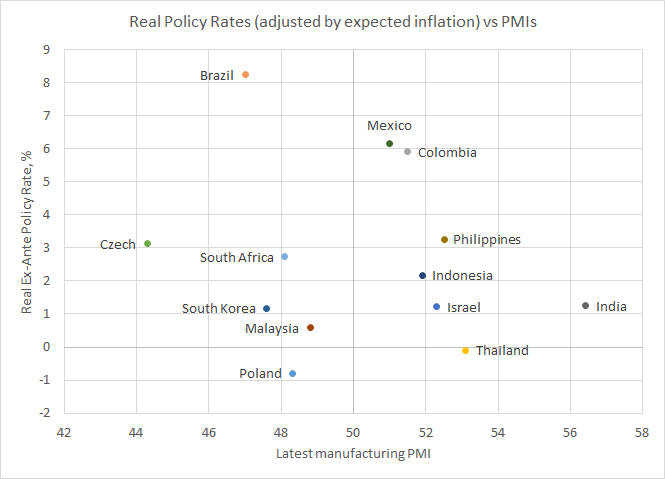

Global Growth Outlook

As more EMs are exiting their tightening cycle, the attention is shifting to the impact of high real interest rates on growth. The chart below plots real policy rates against the latest activity gauges – and it shows that bringing inflation down can come at a price, as domestic demand slows. The updated World Economic Outlook – released by the IMF this morning – reminded that there are additional considerations here, such as the increasingly complicated global backdrop. The report talks about the impact of geopolitical tensions and geo-economic fragmentations, which can “reshape the geography of foreign direct investments”, especially in strategic sectors. Some EMs will be winners in this brave new world – but some can become more vulnerable. Stay tuned!

Chart at a Glance: EM Rate Hikes and Domestic Activity Gauges

Source: Bloomberg LP.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.