Is “Everything Rally” In Trouble?

22 February 2023

Read Time 2 MIN

Fed Message and the Market

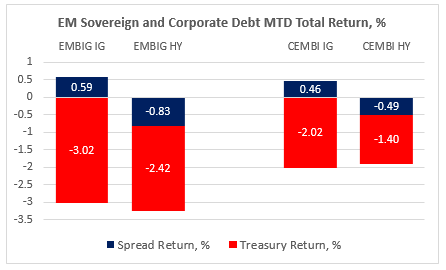

January’s rally in the 10-year U.S. Treasury yield is now completely undone, causing collateral damage in emerging markets (EM) debt. As you can see on the chart below, EM debt’s losses in February are largely the result of higher “risk-free” rates – this applies both to sovereign and corporate bonds. Lower-rated bonds were also affected by higher U.S. rates volatility, which has a fairly strong correlation with High Yield EM spreads (this shows as the negative spread return on the chart). The “higher for longer U.S. rates” narrative is partly driven by a slower pace of disinflation and more robust domestic activity in the U.S. And the market was slow to catch up with the U.S. Federal Reserve’s (Fed’s) hawkish message. The Fed’s minutes this afternoon might well provide an extra push in the hawkish direction.

Fed, Geopolitics, Macro

Can U.S. rates start “decompressing” once the new Fed narrative gets internalized by the market? Quite possibly. It is not unusual for UST yields to anticipate the Fed’s path (the peak rate and eventual easing in this case) well in advance. However, higher geopolitical tensions might complicate things. Will the next leg of Russia’s offensive in Ukraine affect Europe’s growth prospects (the consensus priced out the 2023 recession) and reaffirm the “least bad” status of the U.S. dollar and U.S. rates? Or will another debt ceiling debacle (ummm… debate) in the U.S. – together with the persistent drumbeat about the end of the petrodollar – make the greenback’s life more difficult this time around?

China’s Recovery

China is, of course, an integral part of the global geopolitical “knot”, but we suspect that the market might be paying more attention to the economic data flow in the next few days. China’s high frequency data signals that the recovery might be “uneven” and perhaps even “delayed” until H2/early-2024. There is a sense that perhaps the market’s pause is justified after the huge “reopening” rally, and it’s time to wait until the recovery’s timeline becomes clearer. The next set of China’s activity gauges (out next week) will therefore be closely watched. Stay tuned!

Chart at a Glance: EM Debt Returns Hit by Higher Risk-Free Rates

Source: Bloomberg LP.

CEMBI – J.P. Morgan Corporate Emerging Markets Bond Index is a global, liquid corporate emerging markets benchmark that tracks U.S.-denominated corporate bonds issued by emerging markets entities.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.