Major Narratives Still Intact

31 March 2023

Read Time 2 MIN

Global Drivers for EM Assets

The last day of March brought more signs that two major market narratives are still in play. The global inflation momentum continues to moderate (albeit with some nuances – like stickier than expected core inflation in Europe and some emerging markets (EM)), while China’s recovery keeps gaining traction. This is good news for EMs – as some are more correlated with the U.S. Federal Reserve’s rate cycle and others are more correlated with China’s rebound/growth cycle.

China Recovery

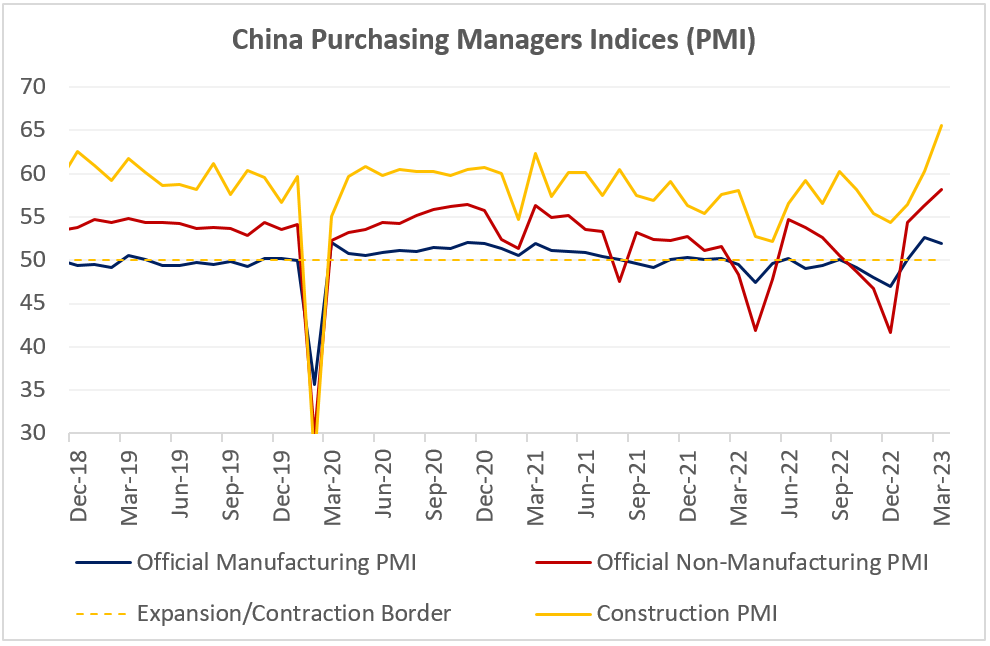

China’s latest domestic activity gauges (Purchasing Managers Indices) support the consensus optimism regarding this year’s growth outlook (5.3% - above the official growth target of about 5%). Key PMI components stayed in expansion zone, with some showing sizable improvements – including services and construction (see chart below). The surging construction PMI reflects a concerted effort to boost infrastructure investments, but could also be indicative of the stabilizing housing sector (which, in turn, a major supporting factor for consumer confidence). The release, however, showed that external growth headwinds might be getting stronger – tighter lending conditions in developed markets (DM) is one obvious avenue – which is why we expect the “supportive yet restrained” policy stance to remain unchanged for now. We also would like to remind that authorities responded very quickly to potential contagion risks associated with the banking mini-crisis in DMs in the middle of the month (in the form of an earlier than expected cut in the reserve requirements for banks).

EM Peak Rates

China’s rebound could create additional inflation pressures going forward – for example, via commodity prices. Global uncertainties like this widen the range of potential growth and inflation outcomes, and this is a reason that keeps various EM central banks on the cautious side as regards policy easing, even when inflation had already peaked. The Colombian central bank stated yesterday that policy stance will remain restrictive for some time, and the Mexican central bank indicated that the balance of inflation risks is still biased to the upside. Both central banks delivered the expected 25bps rate hikes yesterday, and the market thinks that another small “farewell” hike might still be on the table. Stay tuned!

Chart at a Glance: China Activity Gauges Support Optimistic GDP Forecasts

Source: Bloomberg LP.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.