Policy Space and Politics

07 November 2022

U.S. Elections, Growth

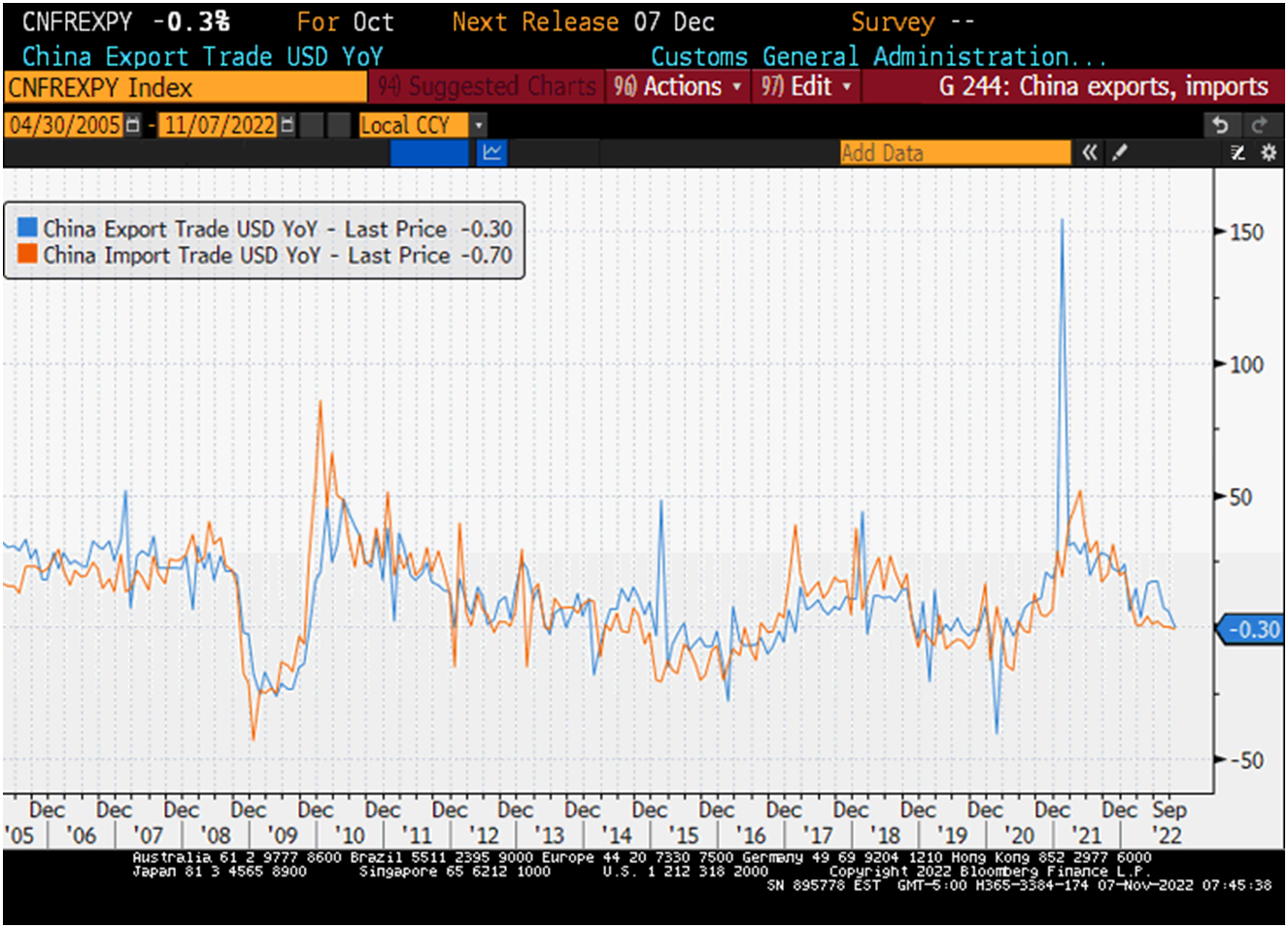

This week’s newsflow is dominated by the U.S. mid-term elections – the impact on the fiscal outlook (and growth and interest rates) is gaining in importance with the prospect of the higher peak policy rate. Concerns about policy room in another independent global growth driver – China – also refuse to go away. China has already used a lot of fiscal space – the government’s primary deficit is expected to be the largest among major emerging markets (EM) and developed markets (DM), both in 2022 and in 2023 – and today’s foreign trade numbers point to persistent growth headwinds. China’s exports and imports contracted in annual terms in October (see chart below), surprising to the downside and reflecting the combined effect of softer global demand and the weakened renminbi. China’s growth is still expected to accelerate in 2023 – but this will be conditional on the removal of COVID restrictions (a lot of buzz, but no concrete steps/timeline yet).

EM Growth and Policy Normalization

The expected growth cliff is already affecting the policy mix in parts of EM. Central banks in EMEA are becoming increasingly dovish – Poland’s rate-setting meeting would be another important test case later this week. In LATAM, Colombia is in a tough spot – the real GDP growth is expected to moderate from 7.3% this year to mere 1.9% in 2023, while inflation continues to surprise to the upside (12.22% year-on-year in October). The government’s policy agenda – which is often ideologically-driven and includes a controversial pension reform proposal among other things – added pressure, both on the currency (the Colombia peso was the worst-performing major EM FX in Q4) and local bonds (the second largest quarter-to-date loss among GBI-EM constituents). And this can limit the central bank’s ability to slow the pace of rate hikes to support growth (or worsen the outlook for local debt if it does).

EM Asia Disinflation, Growth Outlook

The growth outlook for EM Asia is not too bad compared to EM peers – Indonesia reported a stronger than expected Q3 GDP print (5.72% year-on-year), and the consensus sees another healthy expansion (approximately 4.8%) in 2023. This should reduce pressure on fiscal accounts, while allowing the central bank to continue tightening at a measured pace if disinflation stalls. Thailand’s prospects seem to be improving on several fronts at the same time – headline disinflation, the return of the current account surplus and stronger real GDP growth in 2023 (according to the Bloomberg consensus). However, core inflation is still grinding higher, which means more “catching up” rate hikes for the central bank including another 25bps move in November. Stay tuned!

Chart at a Glance: China Foreign Trade – More External Growth Headwinds

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.