Rate Cuts – On the Chopping Block?

04 April 2023

Read Time 2 MIN

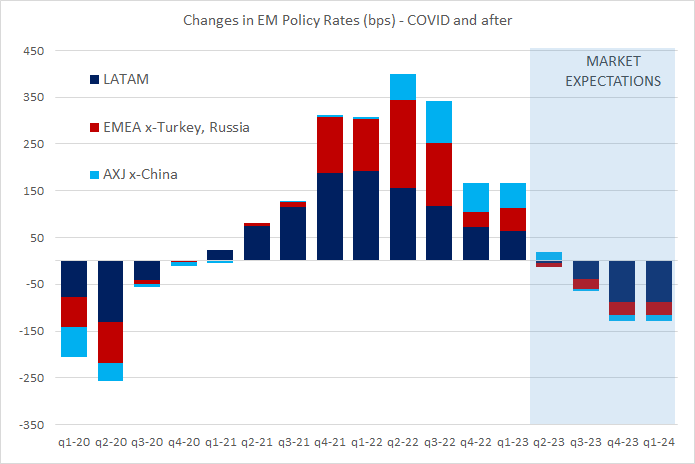

EM Policy Rate Expectations

Various emerging markets (EM) central banks continue to signal that while they are happy to end their tightening cycles, the bar for rate cuts is still high. The latest monetary policy communications in the Czech Republic, Hungary, Brazil, Malaysia and Thailand were surprisingly hawkish. The Bank of Thailand signaled more tightening as the economy continues to rebound. The Czech National Bank explicitly warned the market against “premature” bets on rate cuts, even suggesting that that policy rate might not have peaked yet. The Malaysian central bank cautioned that we are “not out of the woods on inflation”, and South Africa actually re-accelerated the pace of tightening last month.

EM Disinflation

The market seems to be OK with the “rate cuts delayed” narrative, seeing no noticeable easing until Q4 (see chart below). Uncertainty about global growth and the impact of geopolitics/China’s rebound on commodity prices are good reasons for being vigilant. Uneven or slower than expected disinflation also argues for policy caution. Sticky core inflation/inflation expectations are a problem for many central bankers – South Korean inflation prints for March illustrate this point really well. Some board members would prefer inflation to get closer to the target range (or the current benchmark rate) before initiating rate cuts – this was a message from the Romanian central bank earlier today, and we might hear similar undertones from the Chilean central bank in the afternoon.

EM Rate Cuts

Some factors, however, might pave the way for earlier/larger rate cuts. Real policy rates based on expected inflation are getting really high in some EMs, threatening the growth outlook in a situation when fiscal space is getting more limited. The pace of fiscal adjustment is key here (as this might affect inflation expectations) – with Brazil being a prime candidate for the policy rate re-pricing, if the new fiscal framework is deemed credible. We also keep an eye on “the mother of all base effects” that should have a stronger anti-inflation impact in the coming months. Finally, EM FX spectacular performance so far this year can also speed up disinflation, easing pressure on EM central banks and opening more room for rate cuts. Stay tuned!

Chart at a Glance: EM Rate Cuts – No Rush For Now

Source: VanEck Research; Bloomberg LP.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.