We’re Gonna Need a Bigger Boat?

15 March 2023

Read Time 2 MIN

Recession Fears and Fed Rates

Concerns that the Silicon Valley Bank and Credit Suisse “episodes” might not be isolated cases, but rather precursors to a fully-blown banking crisis and a global recession, are not going away, keeping the market expectations for the U.S. Federal Reserve (Fed) thoroughly depressed. The remaining Fed hikes are pretty much out the window this morning, and the Fed Funds Futures now price in 115-120bps of rate cuts (!) between now and December. The European Central Bank’s (ECB’s) rate-setting meeting is tomorrow – policy messaging has been quite hawkish until recently (given a series of upside inflation surprises), but the rate hike expectations are also dwindling as banking concerns jumped from the U.S. to Europe.

China Rebound

One counter-point to the global recession narrative is China’s reopening and growth rebound. The latest domestic activity indicators confirmed that even though the recovery is still moderate, it is gaining pace across the board (an encouraging sign for those concerned about China’s unbalanced growth). Importantly, property investments are finally started to show signs of stabilization – a signal that the easing of housing restrictions is bearing fruit. There was nothing to suggest that the economy needs another massive stimulus, but certain sectors and smaller privately-owned companies might require continuing targeted support.

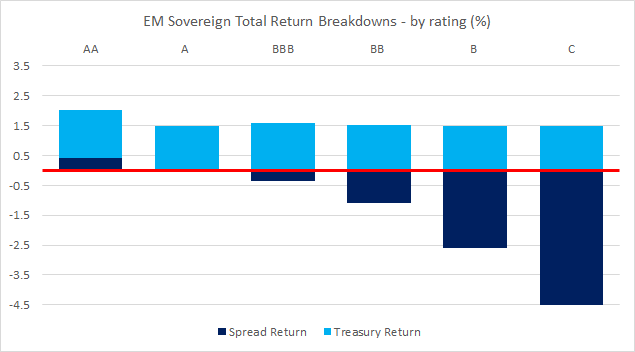

EM Reaction to Market Turbulence

Many emerging markets (EM) are expected to benefit from China’s improving growth outlook – especially in Asia – but the market turbulence in developed markets (DM) is a major risk. So far, the reaction of EM sovereign bonds was quite logical (see chart below). Investment Grade bonds held on quite well (despite thinner spread “cushions”), while spread returns on lower-rated bonds were dragged down, in part, by higher U.S. rates’ volatility. EM FX is under more pressure today, but many local rates rallied in tandem with U.S. Treasuries. A sign of EM resilience so far is that the market continues to price in orderly (and cautious) rate cuts by those central banks that hiked early and aggressively in response to the rising post-pandemic price pressures – rather than “emergency” rate hikes to stem depreciation pressures, as was often the case in the past. Stay tuned!

Chart at a Glance: Market Turbulence and EM Sovereign Bonds – Logical Reaction

Source: Bloomberg LP. Data from 3/9/2023 to 3/14/2023.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

16 January 2025

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.

05 December 2024

"Trump Trade 2.0" fueled U.S. equity and digital asset rallies, while real assets faltered under a strong dollar, with global markets reacting unevenly to pro-growth policies.