Opportunity in Elevated EM High Yield Corporate Bond Spreads?

29 May 2020

Read Time 2 MIN

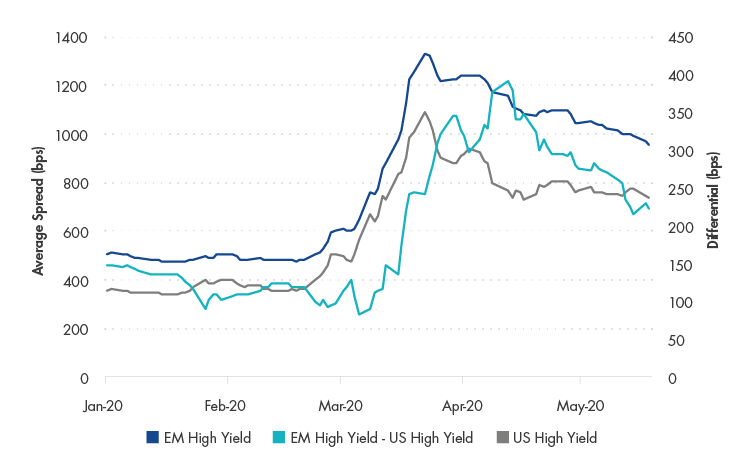

Emerging markets corporate high yield bond spreads continue to stand out following the selloff experienced in March and April. While U.S. high yield bond spreads remain elevated, they are tighter compared to the widest levels reached in late March. In addition to the magnitude of the spreads, which continue to hover around 1,000 basis points, the yield pickup versus U.S. high yield corporate bonds remains historically wide. Since 2004 this differential has averaged 108 basis points, but was 224 basis points as of May 19, 2020, nearly two standard deviations away from this long-term average.

Emerging Markets High Yield Corporate Bond Spreads Remain Elevated

Source: ICE Data Indices as of 5/19/2020. EM High Yield is represented by ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index, U.S. High Yield is represented by ICE BofA US High Yield Index

Several sectors expected by many to be most impacted by negative global growth are exhibiting distress, including Energy, Basic Industry (particularly Metals & Mining), Retail and Transportation. However, we believe emerging markets energy issuers have held up better than U.S. issuers overall due to the greater presence of quasi-sovereigns. Elevated spreads, however, are not confined to these most impacted sectors, and as shown below, these sectors do not have significantly greater weights within emerging markets compared to the U.S. market, indicating a general re-pricing of risk within emerging markets rather than sector-led weakness.

| Weight (%) | ||

| EM High Yield | U.S. High Yield | |

| Automotive | 0.37 | 5.15 |

| Basic Industry | 13.59 | 9.65 |

| Energy | 13.17 | 12.38 |

| Leisure | 2.53 | 4.81 |

| Retail | 0.71 | 4.45 |

| Transportation | 3.62 | 1.09 |

Source: ICE Data Indices as of 5/19/2020. EM High Yield is represented by ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index, U.S. High Yield is represented by ICE BofA US High Yield Index

Are these levels attractive? Clearly the market is pricing in a substantial amount of risk at these levels, including a significantly higher probability of defaults. Whether these spreads are adequate compensation will depend on the ultimate impact of the pandemic and the speed at which global growth will recover.

It is worth noting that emerging markets corporates went into this downturn with what we believe are relatively stronger fundamentals compared to U.S. counterparts, including lower levels of leverage and higher coverage ratios to service debt. Further, we expect to see more “fallen angels”—which are high yield bonds that were originally issued with investment grade ratings but subsequently downgraded—emerge. For example, Pemex1, with over $40 billion of index-eligible debt, entered the emerging markets high yield benchmark at the maximum weight of 3% at the end of April (but did not enter U.S. high yield benchmarks due to index eligibility rules). With both corporate and sovereign downgrades likely, we anticipate that more fallen angels will follow. Given the historical propensity of these bonds to sell-off prior to downgrade, enter the index at deep discounts and subsequently recover in value, these fallen angels may provide some tailwinds to the asset class.

Related Insights

Related Insights

06 March 2026

05 December 2025

11 March 2026

Iran-driven risks are reshaping EM debt markets. EMBX reduced Gulf exposure as valuations failed to reflect rising conflict risk and shifted toward resilient Latam and SSA commodity exporters.

06 March 2026

EM bonds outperformed in 2025 and the case of allocating continues to be supported by a weaker US dollar and stronger EM fundamentals in 2026.

18 December 2025

Get your portfolio ready for 2026 with detailed insights from VanEck’s investment team about the factors driving risk and returns in their respective asset classes.

05 December 2025

EM local-currency bonds offer high real yields, strong 2025 returns, and resilience to shocks, driven by credible policy and solid fundamentals.

04 December 2025

EM high yield has extended its 2025 momentum, delivering strong carry and compelling yields. With higher credit quality and lower defaults, the segment offers a more attractive risk profile than US high yield.