Disinflation – Causes, Surprises, Prospects

10 November 2022

Read Time 2 MIN

Downside Inflation Surprises

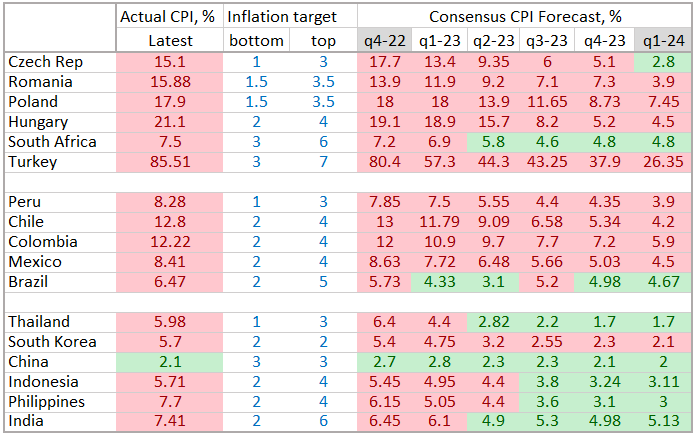

Wow, what a morning! A sizable downside inflation surprise in the U.S. (including core prices), a sharp disinflation move in the Czech Republic, a nervous breakdown in Brazil’s currency and rates (despite on-going disinflation) and “stingy” credit aggregates in China – and we still have the whole day in front of us. Today’s releases confirmed that disinflation is getting more entrenched in parts of both emerging and developed markets (EM and DM) – a fact definitely appreciated by the market. The speed of disinflation, however, will matter more and more going forward. A larger than expected drop in Czech headline inflation (from 18% to 15.1% year-on-year) suggests that prices might indeed return to the target range sooner than in the rest of the region (see chart below), reassuring the market and the central bank that it is safe to remain on hold. Brazil’s prices continued to moderate (to 6%-handle1), but not as fast as expected, and this upside surprise might have been the “last drop” for the market, which is getting wary of the “chimerical” post-election transition team and President-elect spending plans.

China Growth, Stimulus

China’s domestic inflation pressures remain very low – and today’s surprisingly weak credit aggregates explain why: there is a lack of stimulus and a lack of demand. In all fairness, the October moderation was partly seasonal, and authorities did approve numerous measures to prop up growth (especially on the supply side), but the impact will remain muted while the COVID restrictions stay in place (there is a lot of buzz about potential changes, but nothing concrete yet). Mortgage lending suffered a major setback in October – a sizable sequential decline, and a reminder of near-term growth headwinds (real estate and construction account for a significant chunk of gross domestic product).

Global Policy Rate Outlook

Now, what do all these surprises mean for the policy outlook(s)? The dovish pivot narrative got a boost in the U.S., with the Fed Funds Futures now showing a zero probability of a 75bps hike in the December. The Czech swap curve now prices in about 50bps of cuts in the next 12 months, and today’s inflation surprise can encourage Central European neighbors – specifically Poland - to hold on for a bit longer before disinflation (hopefully) kicks in. Mexico and Peru will announce their policy rate decisions in the afternoon – nascent disinflation leaves room for slower rate hikes. And how about EM’s disinflation trailblazer, Brazil? It looks like concerns about the policy direction started to “contaminate” market expectations. The local swap curve now sees only 85-90bps of cuts in the next year – down form 185-200bps just days ago, and compared to ~500bps of cuts priced in for Chile. Stay tuned!

Chart at a Glance: EM Inflation Targets – Progressing At Different Speeds

Source: Bloomberg LP.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.