Disinflation – Bumps, Twists, and Turns

23 December 2022

Read Time 2 MIN

DM Policy Tightening

The global disinflation narrative has shifted from “whether/when” to “how fast,” – but the slowing trend does not mean “smooth sailing.” We get an occasional upside surprise – including the Eurozone’s November revision or today’s U.S. Personal Consumption Expenditure Core Price Index (core PCE). And sometimes inflation peaks remain elusive, downside surprises notwithstanding – like in Japan, where November’s inflation drew extra attention this morning after the central bank’s hawkish yield curve control adjustment a few days ago. These developments explain why the market now expects 44bps of rate hikes in Japan in 2023.

EM Asia Rate Hikes

Emerging Markets (EM) disinflation is on firmer ground – and with lower (tentative) peaks in the case of EM Asia. However, today’s inflation releases in Malaysia and Singapore showed no further progress (in year-on-year terms) in November (contrary to expectations). Further, Malaysia’s core inflation continued to grind higher, challenging the market expectation of the peak policy rate and an extended policy rate pause in 2023. Some sell-side commentators suggested that the central bank might err on the side of caution in January and raise the policy rate one more time – which would be a prudent move, given that the policy rate differential between EM Asia and the U.S. Federal Reserve is very slim now.

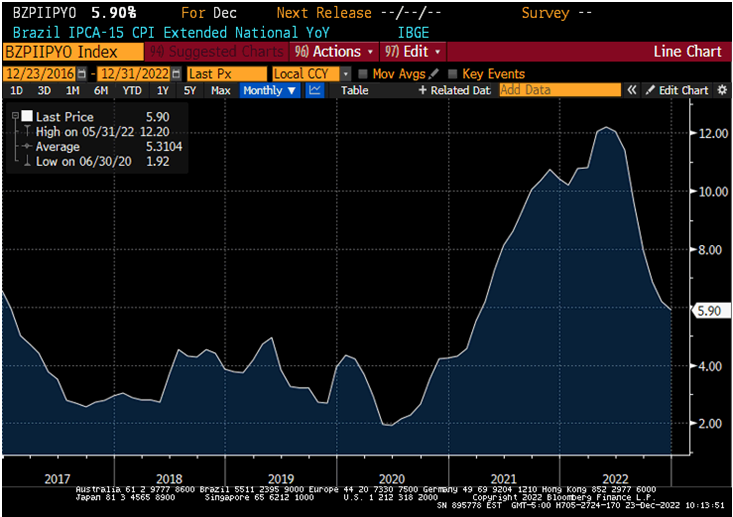

LATAM Disinflation

Yesterday, Mexico’s bi-weekly inflation print was another illustration of the “bumpy road” price trajectory in EM. However, Brazil reaffirmed its “disinflation poster kid” status this morning, with a nice downside surprise and further moderation in mid-month inflation, which is now below 6% year-on-year (vs 12.2% back in May, see chart below). Easing price pressures mean that Brazil’s real policy rate is among the highest in the world – and this leaves ample room for rate cuts in 2023. Whether or not the central bank would be able to use this policy space is a different question though – due to fiscal concerns. The fact that the incoming administration’s spending waver was approved only for one year is a big plus, but the new cabinet’s lineup signals that we might see more populist policy surprises in the coming months. Stay tuned!

Chart at a Glance: Brazil Disinflation – Nice and Steady

Source: Bloomberg LP.

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.