EM Hikes - Outlasting the Fed?

27 June 2022

Read Time 2 MIN

Fed Rate Hikes Expectations, Recession Concerns

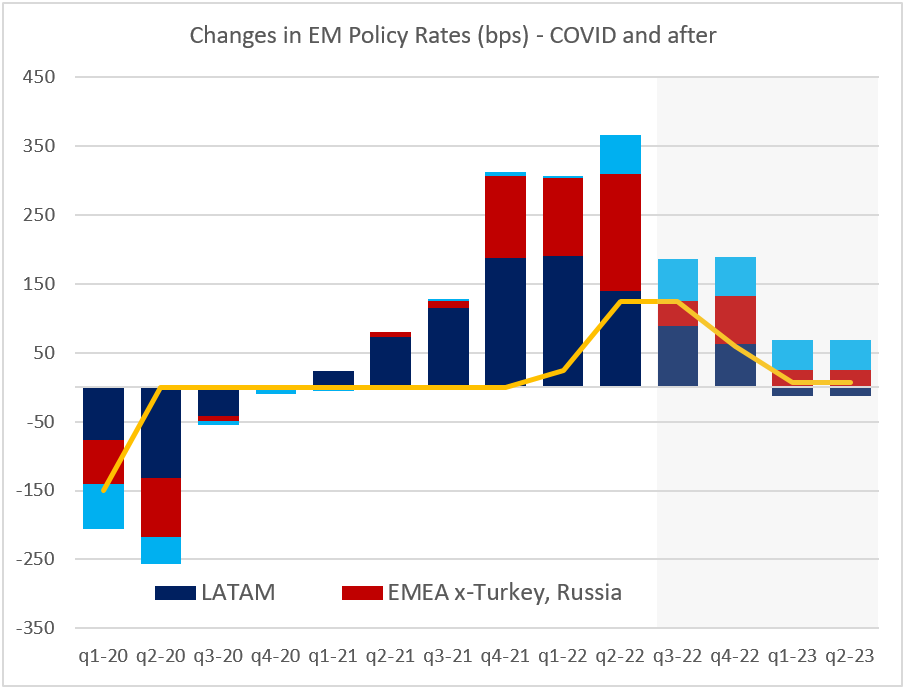

The current hiking cycle in the U.S. is expected to be short-lived – in part due to persistent recession concerns (the nearly-zero Federal Reserve Bank of Atlanta’s GDP nowcast and below-consensus activity surveys for June did little to improve sentiment last week). Where does this leave emerging markets (EM) central banks, many of which started to tighten aggressively well before the U.S Federal Reserve (Fed)? The current market expectations (“embedded” in local swap curves) suggest that the tightening cycle in EM might have peaked in Q2, but it can, nevertheless, outlast the Fed (see chart below). There are several reasons for that.

Uphill Inflation Battle in EM

EMs are facing multiple growth headwinds this year (stimulus withdrawal, capital outflows and higher commodity prices). However, many economies are growing above potential, and it is still an uphill battle on the inflation front for most countries – especially in Central Europe, where annual inflation is now in double digits (the consensus sees Poland’s inflation accelerating to 15.5% year-on-year in June). Aggressive frontloading leaves room for a slower pace of hikes going forward (Brazil is a good example), but it is too early to switch to neutral policy stance – an attempt to do so is likely to be treated by the market as a mistake (keep an eye on the Czech National Bank after the dovish makeover of its board). There is also a “changing of the guard” aspect in EM – Asian central banks were latecomers to the policy normalization game, but are now in the liftoff stage (India, Malaysia, the Philippines) or getting close to it (Thailand, Indonesia).

Turkey’s Unorthodox FX Policy

No discussion about EM rates will be complete without mentioning the block’s “enfant terrible” – Turkey. Turkey is flatly refusing to hike (despite 70%+ annual inflation), expanding the network of “out-of-the-box” FX rules instead. The latest “innovation” limits access to the lira-denominated loans for companies with FX deposits above a certain threshold. The lira did strengthen against the U.S. dollar after Friday’s announcement, but not nearly as much as after the first “out-of-the box” solution in December 2021 (Law of Diminishing Returns?) – suggesting that measures like this are poor substitutes for orthodox policies. Stay tuned!Chart at a Glance: EMs to Continue Hiking in 2022/23

Source: VanEck Research; Bloomberg LP

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.