EM Disinflation – Another Success Story?

01 November 2022

Read Time 2 MIN

Global Peak Inflation

We continue to get upside inflation surprises across the globe, but the peak inflation drumbeat is getting stronger. The disinflation poster kid in emerging markets (EM) is, undoubtedly, Brazil – headline inflation is now in single digits, and, importantly, the price diffusion index is also getting lower (=price pressures are not as widespread as before). Still, the central bank minutes made it very clear that irresponsible fiscal policy may affect inflation and risk premia and that the board would not hesitate to hike again if something goes wrong with the disinflation process. This is a reminder that President-elect Luiz Inácio Lula da Silva (Lula) should think twice before making any dramatic populist policy U-turns. It would also be nice for the outgoing president Jair Bolsonaro to finally concede so that we all can move on – but this is a separate story.

EM Asia Prices And Growth

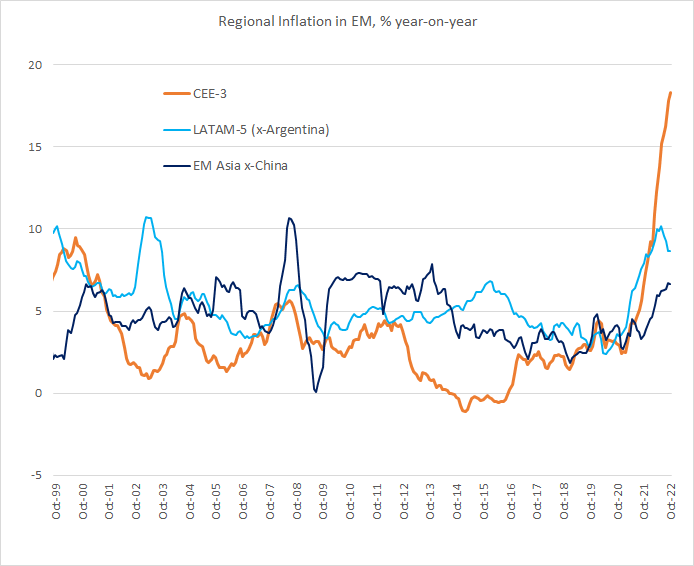

We also watch very intently inflation developments in EM Asia, which might be able to escape the high inflation curse that plagued most of EMEA and LATAM in the past year and a half. A nascent inflation peak in South Korea should probably survive a small expected uptick in October (out this evening). Today’s inflation print in Indonesia also looked promising – outright headline disinflation and lower-than-expected core prices. If regional prices start moderating at levels well below EM Europe/LATAM (see chart below), this might give central banks more policy room to deal with multiplying growth headwinds. Note that the activity gauges (Purchasing Managers Indices, or PMIs) in South Korea, Malaysia, and Thailand remained in the contraction zone in October.

EM Growth Cliff

The collapse of manufacturing PMIs in Central Europe raises a question about the eventual impact of the growth cliff on regional prices. Right now, ~20% inflation in the region is the new “10%” (see chart below) due to the impact of the Russia/Ukraine war on supply chains and energy/commodity prices. But the manufacturing PMI in the Czech Republic is rapidly approaching the COVID levels (it dropped to 41.7 in October), and we are bracing ourselves for tomorrow’s PMI releases in Hungary and Poland. The Czech national bank is meeting on Thursday – and we’ll see how the growth outlook factors into its policy rate decisions. The consensus expectation is that the pause will be extended at 7%, despite 18% annual headline inflation. Stay tuned!

Chart at a Glance: Inflation in EM Regions – Very Different Patterns

Source: VanEck Research; Bloomberg LP.

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.