EM – Fighting Against DM Currents

26 September 2022

Read Time 2 MIN

Rising Global Rates

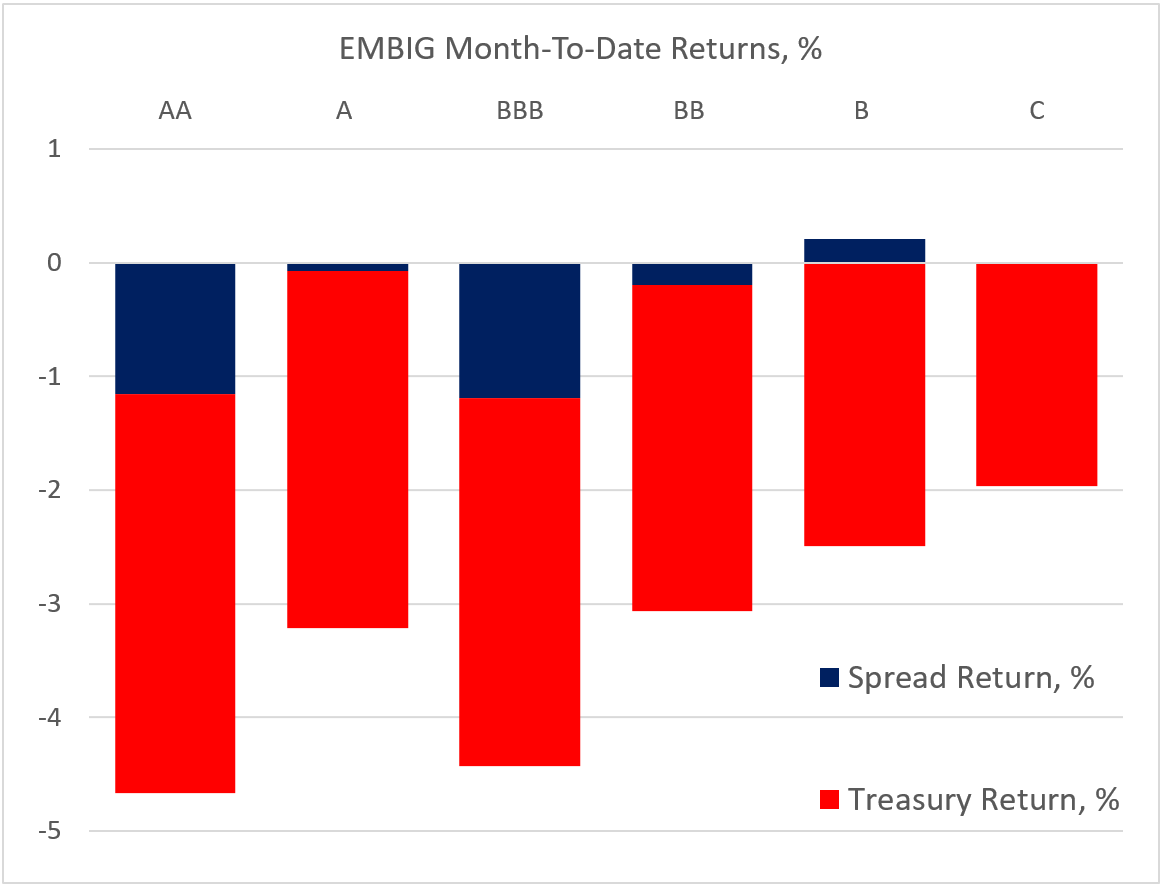

Emerging markets (EM) are caught in the global sentiment vortex, and rising global rates are dragging down returns on EM debt – irrespective of ratings and often “overriding” fundamentals (see chart below). This is one reason we closely monitor the market expectations for key policy rates – the expectations for the U.S. Federal Reserve were stable this morning, with the November hike (+75bps) and the cycle’s terminal rate (4.73%). The current surge in the terminal rate expectations for the Bank of England (over 6% as of this morning, according to Bloomberg LP) is still perceived as an isolated event, driven by the local policy agenda.

EM Tightening Cycles

It is noteworthy that the market continues to acknowledge EMs’ aggressive – and early – rate hike frontloading in the current cycle and does not automatically adjust the terminal rate expectations in lockstep with developed markets (DM), as was often the case in the past. Brazil is #1 on the “Divergent” list. The central bank stayed on hold at its last meeting, and the local swap curve does not price any additional rate hikes. Brazil’s real policy rate adjusted by expected inflation is the highest in EM, and it is one of the few countries where the 2022 growth outlook was revised upwards (a lot – from 0.5% to 2.35%). And today’s balance of payments numbers showed that Brazil might have problems (including a very entertaining political scene), but external is not one of them. Emerging markets where the markets did raise the terminal rate expectations in a meaningful way are relative latecomers to the global tightening cycle (Hungary, Malaysia, and South Africa).

China Growth And FX

China is a major dovish exception in EM (and the world), as authorities are trying to prop up this year’s GDP growth (the consensus forecast has been cut to 3.35%) amidst the housing sector disruptions and the zero-COVID approach. A side-effect of easing policies is the currency weakness – and the pace of depreciation is now getting too fast for comfort. This explains why the central bank decided to impose a 20% risk reserve requirement on FX forward sales for banks, hoping this will help stabilize the market expectations for the renminbi. Stay tuned!

Chart at a Glance: EM Sovereign Debt Total Returns by Rating Bucket*

Source: Bloomberg LP

EMBIG – JP Morgan’s Emerging Market Bond Global Index that tracks total returns for traded external debt instruments in the emerging markets.

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.