EM Inflation - Memes and Themes

09 August 2022

Read Time 2 MIN

Summary

There are finally signs of disinflation in some EMs, but for the majority it is still “hike, baby, hike”.

EM Disinflation

It’s a “The Eagle Has Landed” and “Elvis Has Left the Building” morning in Brazil. Headline inflation dropped a bit more than expected to 10.07% year-on-year, which means that the country is now officially in disinflation zone. Tax cuts definitely helped, but the Brazilian central bank did an amazing job, responding to rising price pressures early and aggressively – and we are now seeing the results. Brazil’s real rates adjusted by expected inflation are among the highest in emerging markets (EM), and they still look reasonably attractive relative to macroeconomic fundamentals.

Fiscal and Monetary Tightening in EM

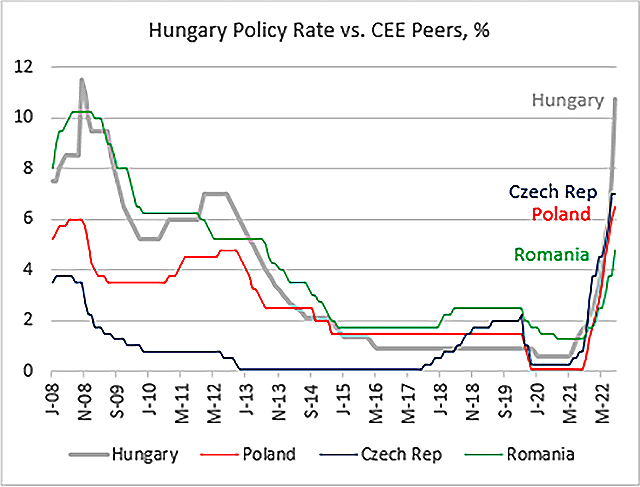

For many other EMs, it’s a “you’re gonna need a bigger boat”… sorry, a bigger rate hike story. Let’s start with Hungary, where annual headline inflation unexpectedly jumped to 13.7%. There are legitimate concerns about an H2 growth “cliff” in the region, but we are not seeing it yet in Hungarian high-frequency data (take, for example, July’s super-strong manufacturing survey of 57.8). Authorities are firing on all cylinders – doing both fiscal adjustment and aggressive monetary tightening – but today’s inflation release signals that it is too early to stop.

Inflation Persistence

Back in LATAM, Mexico’s upside surprise was not huge, but with annual headline inflation rising above 8% and core inflation above 7.6%, a 75bps rate hike on Thursday would be a very good idea indeed. Chilean July CPI was also higher than expected, accelerating to 13.1% year-on-year, and driven in part by fiscal measures aimed at supporting consumption in a high-inflation environment. So, it’s “hike, baby, hike” for the central bank, and the latest minutes clearly signaled more tightening going forward. Stay tuned!

Chart at a Glance: Central Europe Policy Rates - Different Speed

Source: Bloomberg LP

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.