EM Policy Options - To the Drawing Board

11 August 2022

Read Time 2 MIN

Summary

Recent changes in inflation and growth surprises are making emerging markets to re-evaluate their policy options.

EM Inflation, Growth Surprises

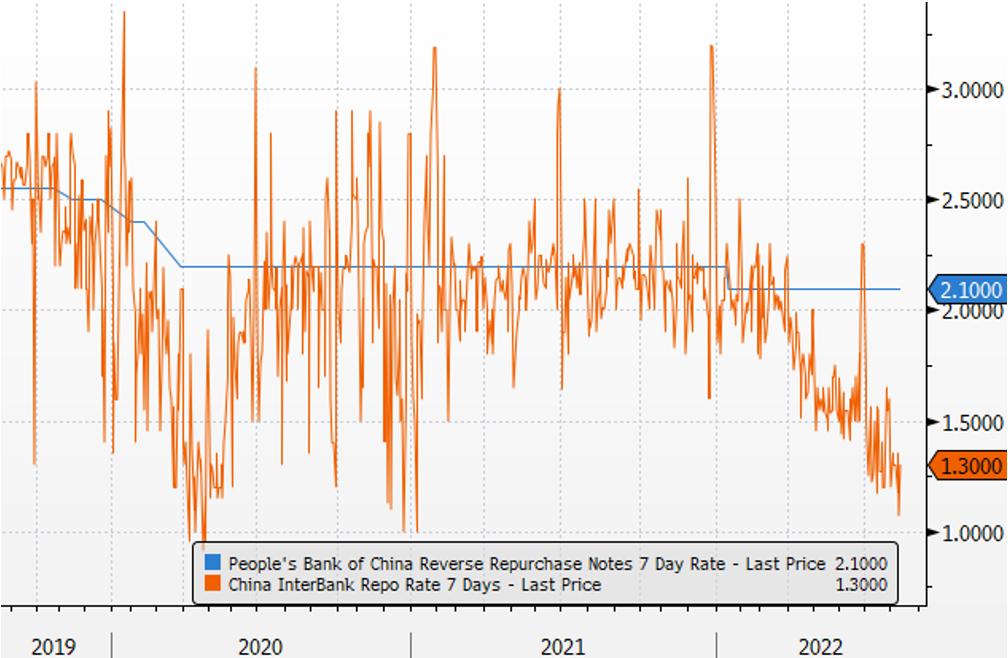

The inflation surprise index for emerging markets (EM) has been going down since May. The growth surprise index appears to be flat lining. It is therefore not surprising that an increasing number of EMs are going back to the drawing board to evaluate their policy options. In China, the central bank’s Q2 monetary policy report signaled that “a wall of liquidity” will not be coming back any time soon, despite benign inflation and multiple near-term growth headwinds (the 2022 consensus GDP growth has been cut to 3.9%). The chart below - with interbank rates well below their benchmark - shows why additional rate cuts might not be a policy option of choice either (there is no point), and why authorities are likely to focus on regulatory changes and fiscal channels.

Growth and Pace of EM Rate Hikes

Near-term growth headwinds might be even stronger in Central Europe, which is exposed to higher energy prices and negative spillovers from its main trading partner, the Eurozone. The Czech National Bank kept the policy rate on hold, opting for FX interventions (about 15% of the international reserves since mid-May, according to some sell-side estimates) to cap inflation pressures. Hungary is actively employing fiscal tightening (a surprising surplus in July) in addition to more aggressive benchmark frontloading. So, today’s decision to keep the 1-week deposit rate unchanged looks perfectly logical in all respects. Finally, today’s minuscule downside surprise in Romanian inflation can give the central bank an excuse to tighten at a slower pace going forward.

LATAM Policy Divergence

The inflation and growth landscapes in LATAM look quite diverse. Brazil is exiting its tightening cycle - and rightly so. But other countries/central banks might need to work harder (=hike more) to leave the inflation peak behind. Mexico’s rate-setting meeting will be closely watched this afternoon. The consensus expects another sizable hike of 75bps, following an upside inflation surprise in July. But the statement will be equally important as regards the balance of risks and especially the central bank’s view on growth risks, because Mexico’s manufacturing survey (Purchasing Managers Index) unexpectedly moved into contraction zone in July (48.5). Stay tuned!

Chart at a Glance: China Interest Rates - Lower Without Policy Rate Cuts

Source: Bloomberg LP

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.