Benvenuti in VanEck

Seleziona il tipo di investitore

19 febbraio 2021

Un segnale positivo, che indica una ripresa dell'economia, è il rialzo del prezzo delle azioni delle società estrattive dai minimi toccati lo scorso marzo allo scoppio dell'epidemia di Covid. Seguendo l'andamento rialzista dei prezzi di rame, ferro, platino e altri metalli, queste società minerarie globali hanno recuperato le perdite subite e hanno proseguito la corsa.

Due delle maggiori società minerarie mondiali hanno appena confermato il proprio ruolo di leader nella ripresa, remunerando generosamente i propri azionisti sulla scia della migliore congiuntura degli ultimi dieci anni. Questa settimana ho letto con piacere che BHP ha dichiarato un dividendo record e che Glencore ha ripreso a distribuire dividendi dopo averli sospesi lo scorso anno.

Sono due dei giganti mondiali dell'estrazione mineraria e, insieme a società come Anglo-American, Rio Tinto e Vale, controllano la produzione mondiale di metalli. Nell'annunciare i risultati annuali di Glencore la scorsa settimana, il Ceo Ivan Glasenberg ha usato toni ottimisti. Proprio mentre l'offerta di metalli si contrae – ha dichiarato – la domanda cinese esplode. Se il governo statunitense lancia ora un imponente programma di investimenti infrastrutturali – ha aggiunto – riuscirà a stimolare ulteriormente la domanda, creando condizioni di grande crescita.1.

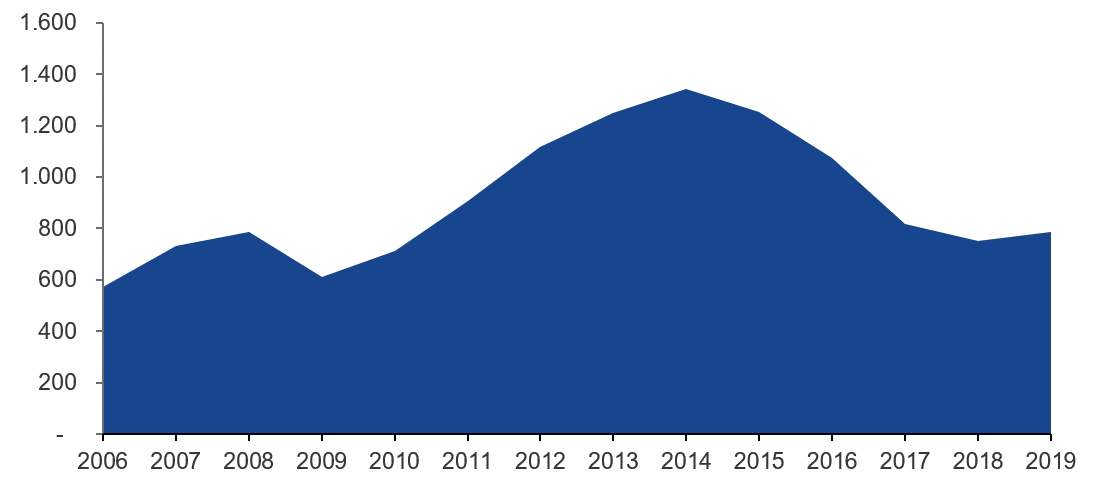

Una domanda sorge spontanea: siamo all'inizio di un super-ciclo, di un lungo periodo di tempo in cui la domanda crescente supera l'offerta? In genere, l'estrazione mineraria è un settore estremamente ciclico in cui la spesa per investimenti oscilla tra alti e bassi, spesso provocando una carenza di offerta proprio nel momento in cui si registra un aumento della domanda (figura 1). L'ultima volta che si è verificata una situazione simile è stato negli anni Duemila, quando l'esplosione dell'edilizia in Cina aveva colto alla sprovvista il settore estrattivo, innescando un super-ciclo.

Fonte: McKinsey, Through-cycle investment in mining, 8 luglio 2020.

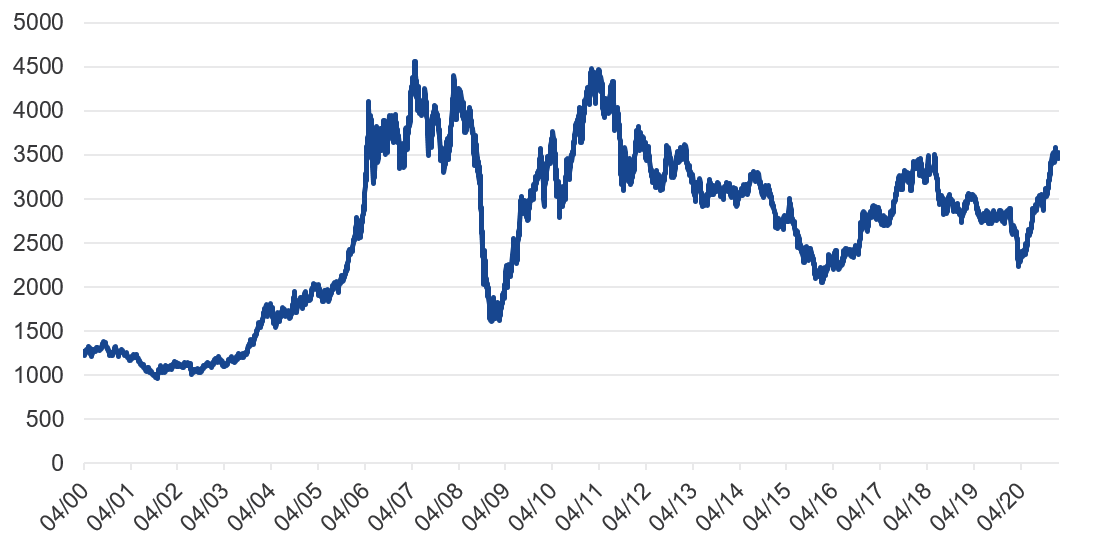

Quel che è certo è che i prezzi dei metalli registrano un'impennata. Nell'ultimo anno, il prezzo del ferro ha guadagnato oltre l'85% toccando a dicembre – prima di ritracciare – il massimo a nove anni, ossia 175 dollari Usa per tonnellata. Il rame è aumentato dell'80% dai minimi di marzo, raggiungendo un massimo a otto anni di oltre 8.400 dollari per tonnellata.

Fonte: Bloomberg. I risultati passati non costituiscono un indicatore affidabile dei risultati futuri. Il London Metal Exchange LMEX Index è calcolato una volta al giorno sulla base dei prezzi di chiusura dei sei metalli principali: rame, alluminio, piombo, stagno, zinco e nichel. Al suo lancio nel 1984 il suo valore base era 1000.

Molti pensano che l'imminente transizione verso un'economia a basse emissioni di carbonio stimolerà la domanda di metalli quali acciaio e rame, utilizzati nelle turbine eoliche o per cablare i pannelli solari e i veicoli elettrici. L'Unione Europea, il Regno Unito e molti altri paesi si sono impegnati a eliminare il carbonio dalle proprie economie entro il 2050, mentre la Cina si allineerà nel 2060. Molte di loro hanno obiettivi intermedi per il 2030, il che significa che la transizione deve iniziare immediatamente.

Si dovrà installare una quantità enorme di energia eolica, pannelli solari, elettrolizzatori per l'idrogeno, fabbriche per batterie elettriche, ecc. Secondo la Commissione europea, entro il 2050 nella sola Europa saranno necessari 240-450 GW di energia eolica prodotta offshore2. Riproponendo classicamente l'andamento di altri cicli delle materie prime, le società minerarie non investono in nuovi progetti di esplorazione, che comportano rischi, e quindi la loro offerta è limitata.

Molte delle società comprese nel VanEck Global Mining UCITS ETF dispongono di riserve dei metalli necessari per affrontare questa enorme transizione. Tra queste, le più grandi estraggono ad esempio litio, nichel e solfato di cobalto, tutti metalli utilizzati nella produzione di batterie.

Praticamente tutti noi compreremo presto quantità maggiori di metalli semplicemente acquistando veicoli elettrici, pompe di calore e pannelli solari. Come olandese che vive al di sotto del livello del mare, nei Paesi Bassi, sono abituato all'idea di mulini a vento che limitano l'innalzamento del mare. La differenza è che i mulini a vento olandesi, costruiti in legno, erano storicamente usati per pompare l'acqua del mare, mentre oggi, quelli in metallo, dovrebbero innanzi tutto rallentare il riscaldamento globale e impedire l'aumento del livello dei mari.

Nel frattempo, chiunque condivida la tendenza rialzista del Ceo di Glencore può facilmente investire in un paniere delle principali società estrattive del mondo attraverso il nostro ETF sui titoli minerari. Questo ETF offre esposizione ad azioni di società minerarie di tutto il mondo, compresi i mercati sviluppati e in via di sviluppo. Le società in questione sono leader nell'estrazione di oro, argento, rame, nichel, zinco, litio e ferro. Sono quelle sulle quali puntiamo nel passaggio verso le energie rinnovabili per elettrificare l'economia globale.

Gli investitori devono considerare i rischi prima di investire. Investire in società minerarie espone ai rischi associati alle risorse naturali, ad esempio quello di esaurimento, di oscillazione dei prezzi e il rischio geopolitico. Non intendiamo prevedere un super-ciclo. I prezzi di mercato possono anche calare.

1Fonte: The Times.

2Fonte: Commissione Europea.

Esclusivamente per scopi informativi e pubblicitari.

Queste informazioni sono redatte da VanEck (Europe) GmbH che è stata nominata distributore dei prodotti VanEck in Europa dalla Società di gestione VanEck Asset Management B.V., costituita ai sensi della legge olandese e registrata presso l'Authority for the Financial Markets (AFM) dei Paesi Bassi. VanEck (Europe) GmbH con sede legale in Kreuznacher Str. 30, 60486 Francoforte, Germania, è un fornitore di servizi finanziari regolamentato dall'Ente federale tedesco di vigilanza dei servizi finanziari (BaFin). Le informazioni contenute in questo commento hanno l'unico scopo di offrire agli investitori indicazioni generiche e preliminari e non costituiscono in alcun modo consulenza d'investimento, legale o fiscale. VanEck (Europe) GmbH e le sue affiliate (congiuntamente "VanEck") declinano ogni responsabilità relativamente decisioni d'investimento, disinvestimento o di mantenimento delle posizioni assunta dall'investitore sulla base di queste informazioni. Le opinioni e i pareri espressi sono quelli degli autori, ma non corrispondono necessariamente a quelli di VanEck. Le opinioni sono aggiornate alla data di pubblicazione e soggette a modifiche in base alle condizioni del mercato. Alcune dichiarazioni contenute nel presente documento possono costituire proiezioni, previsioni e altre indicazioni prospettiche che non riflettono i risultati effettivi. Le informazioni fornite da fonti terze sono ritenute affidabili e non sono state sottoposte a verifica indipendente per accertarne l'accuratezza o la completezza, pertanto non possono essere garantite. Tutti gli indici menzionati sono studiati per misurare i settori e le performance di mercato comuni. Non è possibile investire direttamente in un indice.

Tutte le informazioni sulle performance sono storiche e non costituiscono garanzia di risultati futuri. L'investimento è soggetto a rischi, compreso quello di perdita del capitale. Prima di investire, è necessario leggere il Prospetto e il documento contenente le informazioni chiave per gli investitori (KID).

Nessuna parte di questo materiale può essere riprodotta in alcuna forma né citata in un’altra pubblicazione senza l’esplicita autorizzazione scritta di VanEck.

© VanEck (Europe) GmbH

07 giugno 2026

26 maggio 2026

18 maggio 2026

07 giugno 2026

26 maggio 2026

18 maggio 2026