EM Institutions and Markets

08 December 2022

Read Time 2 MIN

LATAM Politics

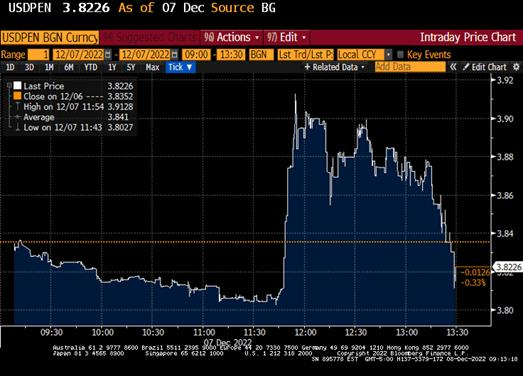

Very often when we talk about institutional frameworks in emerging markets (EM), it is in a context of their weakness, which can lead to deteriorating economic metrics, rating downgrades, and a loss of investor confidence. But there are other – much more encouraging – examples (which can also create interesting trade opportunities). Take yesterday’s “lunchtime” coup attempt in Peru. President Pedro Castillo (who is now ex-President) tried to avoid impeachment by unlawfully dissolving the congress. But the congress had none of it, impeaching Castillo anyway, and putting him in jail. The line of succession was clear, and by the early-afternoon Peru had the first ever female president, Dina Boluarte. The currency – which sold off initially – ended up stronger against the U.S. Dollar (see chart below), and the central bank matter-of-factly delivered a 25bps “farewell” policy rate hike. The end.

EM Rate Cuts

Institutional constraints also allowed the Brazilian central bank to remain on hold yesterday – instead of delivering a “warning shot” rate hike to address new administration’s fiscal expansion plans. President-elect Lula’s grand (populist) vision for social spending underwent a reality check in the parliament, and the market responded by pricing out some rate hikes on a 6-month horizon. Fiscal risks are still here – they featured prominently in the central bank’s statement, and they can delay 2023 rate cuts. As of this morning, the local swap curve was seeing no policy easing until September 2023 (compared to March/May 2023 before the elections runoff).

EM Disinflation

Institutions is a major discussion topic in Mexico and Hungary, but today’s market focus was on inflation. It looks like Mexico is finally on the disinflation track – with both core and headline bi-weekly inflation much lower than expected at the end of November. This should allow the central bank to safely slow the pace of rate hikes (to 50bps at the next meeting in a few days). Hungary’s case is more complicated. Headline inflation accelerated above consensus in November (to 22.5% year-on-year), and it is now set to get even higher in December (peaking at 25-26%) after the removal of gasoline price caps. The caps removal can actually be beneficial for Hungary’s budget (and for bonds’ technicals), but it is also essential that the central bank maintains a hawkish policy stance until inflation starts rolling over in 2023. Stay tuned!

Chart at a Glance: EM Asset Prices (Peruvian Sol) – The Importance of Being Nimble

Source: Bloomberg LP.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.