Global Growth Risks and EM Prospects

29 June 2022

Read Time 2 MIN

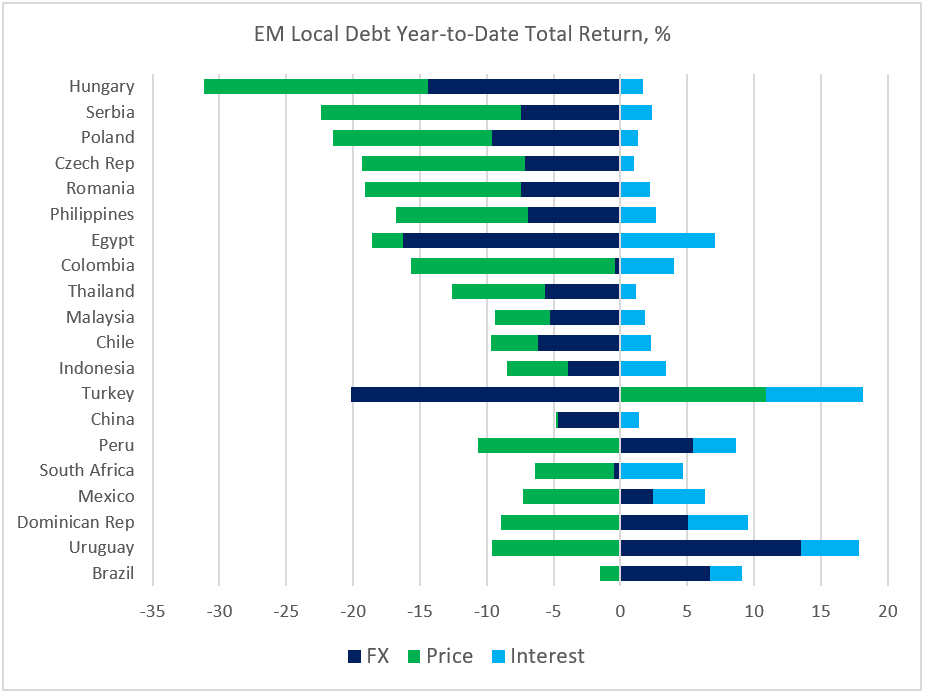

EM Local Debt Performance

Surging global inflation and elusive inflation peaks have not been kind to emerging markets (EM) local rates so far this year. But – as the chart below shows – currency dynamics can make a big difference for EM local debt’s total return. Central bank credibility and the timely/aggressive policy response gave a much needed boost to the South African rand and LATAM FX. The question is whether a growing risk of recession will change the playing field in the second half of the year. Very weak consumer confidence in parts of Europe, below-consensus activity surveys in developed markets (DM) and today’s downward revision of Q1 GDP in the U.S. (especially private consumption) suggest that this risk might not be fully priced in by the market.

EM Growth Prospects

As regards EM local debt year-to-date outperformers, the 2022 growth outlook for LATAM has actually been upgraded a bit after hitting the bottom in March-April. The tightening cycle in the region has further to run – which means restrictive policy stance – as inflation is high and well above the target. However, aggressive frontloading should be allow to proceed at a slower pace (of rate hikes) going forward, with a prospect of eventual rate cuts later in 2023. The growth newsflow in South Africa is more concerning though. First, the central bank is a latecomer to the EM tightening cycle and might need to step up rate hikes to bring inflation back to the target range (headline inflation escaped last month). Today’s comments by Governor Lesetja Kganyago about a potential 50bps hike in July were deemed insufficiently hawkish by the market. Second, the wage talks at the country’s power utility, Eskom, resulted in another wave of load-shedding and blackouts. Finally, consumer confidence posted a big drop in Q2 – to the levels last seen in the early-1990s (with the exception of the pandemic).

China Slowdown

The next batch of China’s domestic activity gauges – out this evening – can be an important catalyst one way or another. The market reacted positively to changes in the quarantine rules, and the consensus also expects that both the manufacturing and services PMIs (Purchasing Managers Indices) flip into expansion zone in June. China’s 2022 GDP forecast has been cut again this morning (to 4.13%), but if June’s PMIs do not disappoint, it can mark the lowest point in the current cycle. Stay tuned!Chart at a Glance: EM Local Debt Performance – Not A Monolith

Source: Bloomberg LP (J.P. Morgan GBI-EM Global Diversified Index)

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

10 February 2026

Debasement is back in focus. Here’s what’s driving it, what could reverse it and how we’re positioning portfolios for both scenarios.

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.