Gold Shines Through Market Chaos

06 March 2020

Read Time 5 MIN

Gold Shines Through Market Chaos

Coronavirus concern was the dominant driver across global markets in February and the gold market was no exception. Gold fell to its monthly low on February 5 as the S&P 500® trended to new all-time highs on the belief that the impact from coronavirus could be contained. As more infections were reported from South Korea, the outlook became clouded and gold had a strong advance to a seven-year high of $1,689 per ounce on February 24. Gold bullion exchange traded funds saw an unprecedented 25 consecutive days of inflows. However, during the last week of the month, markets came unglued as it became clear that the virus was spreading globally with infections in Italy, Iran and the U.S. The stock market crashed, creating a flight to cash, margin calls, and unusual derivatives trading. Safe haven assets such as gold, gold stocks and the U.S. dollar fell in the chaos. For the month, gold declined $3.47 per ounce (0.2%). The NYSE Arca Gold Miners Index (GDMNTR) dropped 8.13% and the MVIS Global Junior Gold Miners Index (MVGDXJTR) declined 10.41%.

Historically, Quick Rebound for Gold Stocks in Panic

While the sell-off in gold stocks was painful, it is not unusual in the midst of a stock market panic. The last such example was the 2008 financial crisis crash. Following the September 15, 2008 Lehman bankruptcy, gold declined just 10% before trending higher on October 27. Over the same period in 2008 the GDMNTR fell 48%, but by December 16 it had recovered to its pre-Lehman level in a classic V-shaped recovery. Contrast this with the S&P 500 that didn’t reach a bottom until March 6, 2009 after falling 46%. The S&P didn’t recover its post Lehman losses until January 2011. So, while the general stock market was struggling to recover for over two years, the gold stock market quickly rebounded and went on to bull market gains. We believe the markets will look back on the coronavirus “black swan” as a buying opportunity for gold shares, however, whether the worst is yet behind us is anyone’s guess.

Economic Impact of Virus Likely to End Expansion

As the virus spreads and the prospects for a vaccine or treatment are months in the making, it appears the economic impact will be substantial and we would not be surprised to see the longest economic expansion and bull market in history to come to an end in 2020. We look to China where the coronavirus has been in play for several months to see the potential depth of economic weakness. The China Manufacturing Purchasing Managers Index (PMI) fell from 50 in January to 35.7 in February, below the previous low of 38.8 in 2008. Likewise, the Non-Manufacturing (or services) PMI plummeted to a record low of 29.6 in February (below 50 is contractionary). The U.S. ISM Manufacturers PMI Index stands at 50.1 while the Non-Manufacturing PMI is 57.3. Meanwhile, the latest Euro Area IHS Markit Manufacturing PMI is 49.2. Note that the U.S. and Euro Area PMI’s were measured before the recent spread of the virus.

The Fed is Running Out of Bullets

Any action the U.S. Federal Reserve (Fed) takes in response to a virus-weakened economy is likely to lack efficacy. There are two aspects that make a coronavirus economy extremely difficult to stimulate. First, this is a deflationary shock with declines or stoppages in work, travel, leisure and other forms of economic activity. Second, it is likely to create shortages due to the interruption of global supply chains, which would normally be inflationary. No amount of rate cuts or quantitative easing will have much impact until people and businesses are able to resume normal activities. In any case, central banks have little or no room to stimulate with the Fed funds rate already low at 1.0% - 1.25% and comparable rates in much of Europe and Japan are negative. The Fed has typically cut rates by roughly 5% in past recessions.

Overwhelming Levels of Debt Could Drive Gold Higher

If there is to be a recession, then we believe that debt will become the foremost risk, as it has been in nearly every recession. Corporate profit growth has been in decline and Goldman Sachs now projects no earnings growth this year. Yet, corporate debt is at record levels as are the amount of risky leveraged loans. In addition, more debt is likely to be downgraded to junk status in a recession, which could force many funds to sell. Meanwhile, overwhelming levels of sovereign debt may limit government’s ability to borrow and spend in a downturn. Central banks may come under pressure to monetize or print money to keep governments and businesses afloat. These are the financial risks that might drive gold higher in the next recession.

Gold Investors Must Not Lose Sight of Bigger Picture

As markets gyrate, gold investors must not lose sight of the bigger picture. For over a year the primary driver of the gold price has been falling real rates. Through the coronavirus crash, ten-year treasury yields have plummeted to all-time lows. With the markets in disarray, gold has not responded to this fall in real rates. Once the volatility subsides, we expect real rates to again become a primary driver of gold prices.

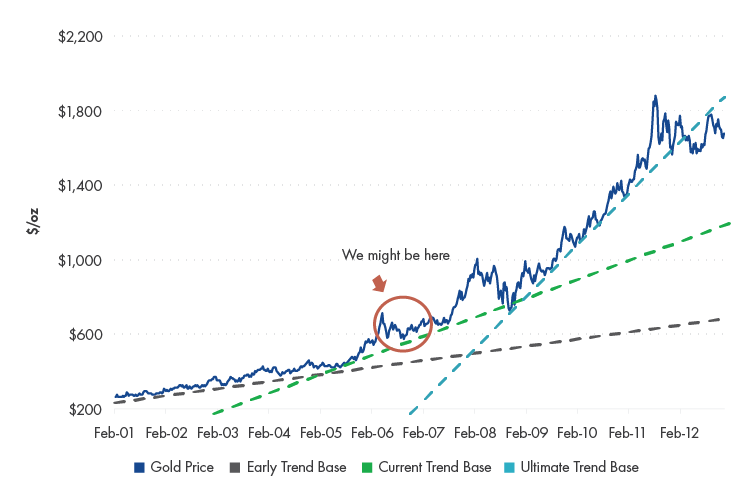

Gold and gold stocks are in the midst of a secular bull market that started in December 2015 when gold bottomed out at $1,050 per ounce. The two gold price charts highlight the technical similarities between the current bull and the 2001 – 2011 bull. The first chart tracks the price trend of the current bull market. It began with a weakly rising trend for several years, then accelerated to a stronger trend in 2019. Likewise, in the second chart an early trend of weakly rising prices broke into a stronger trend in 2005. In the earlier market (second chart), the ultimate trend followed the financial crisis in 2008. The red circle shows roughly where the current market might be in the larger scheme of things, using the 2001 – 2011 market as an analogy.

Fundamentally, each of these markets had different drivers, with the early 2000’s market driven by fallout from the tech bust and U.S. dollar weakness. The early years of the current market were driven by geopolitical risks and Fed activity. Regardless of specific drivers, both markets rose with increasing risks to the global financial system where gold was bought as a safe store of wealth.

Comparing Bulls: Current Market Similar to Gold’s Last Secular Rally

Source: Bloomberg, VanEck. Data as of February 28, 2020. Past performance is no guarantee of future results. Chart is for illustrative purposes only.

Related Insights

Related Insights

08 April 2026

Gold pulled back amid rising rates and a stronger dollar, but history shows volatility is typical in crises. Strong margins leave miners well positioned if gold stabilizes or moves higher.

10 March 2026

Gold miners are generating record margins and free cash flow as prices remain elevated. With disciplined capital allocation and costs below $2,000 per ounce, the sector appears well positioned for 2026.

10 February 2026

Gold price swings in January highlighted volatility, not weakness. Strong demand, central bank buying and improving miner fundamentals continue to support a durable long-term bull market in 2026.

14 January 2026

Gold hit record highs in 2025 as central banks and investors boosted demand. Mining stocks outpaced bullion, and despite sharp gains, attractive valuations and strong margins point to more upside in 2026.

18 December 2025

Get your portfolio ready for 2026 with detailed insights from VanEck’s investment team about the factors driving risk and returns in their respective asset classes.