EM Bonds - Place Your Bets

13 April 2023

Read Time 2 MIN

EM Bonds Performance

The latest IMF projections show that the growth differential between emerging and developed economies should improve noticeably in favor of EMs in 2023 - an additional factor supporting the outlook for the asset class this year. However, EM is not a monolith, and while the market looks with amazement at super-tight sovereign spreads of “EM Graduates,” some lower-income EMs appear more distressed. As the debt restructuring drumbeat is getting stronger, many participants were unhappy about the slow progress in the common framework, especially as regards China’s role and the involvement of private creditors. China might be in a unique position to push things ahead. Still, the recent change of leadership and some institutional features inside China can make it more difficult to follow in the Paris Club's footsteps. Geopolitical tensions involving China create an extra layer of uncertainty that can lead to further delays.

EM Structural Reforms

These issues define a broader context for discussions about structural reforms in EM, including fiscal adjustment. Everybody agrees that exceptional fiscal support during the pandemic was fully justified. Still, now governments have to balance disinflation and financial stability with the need to continue protecting the most vulnerable, especially in low-income countries. Some participants pointed out that aggressive fiscal consolidation in countries with high debt levels might have an offsetting negative impact on GDP, delaying their progress in meeting the UN’s sustainable development goals.

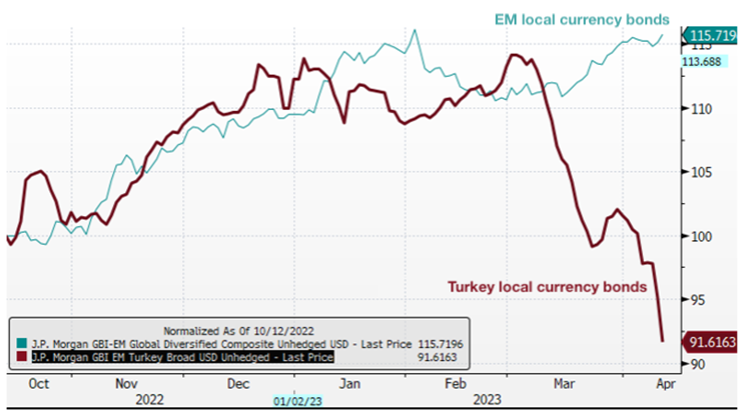

Turkey Elections

One country that has attracted a lot of attention this year is Turkey. Turkey is heading for the elections in exactly one month. The local bond rout (see chart below) signals that the market prices in (1) a normalization of the policy rate after the elections, and (2) the central bank having less firepower to support the local bond market, given the need to defend the exchange rate. Investors expect a lot of noise and volatility immediately after the elections, while the new team is put in place and some macro-prudential regulations potentially lifted. Deputy Portfolio Manager David Austerweil visited Turkey recently. He believes that the elections will majorly impact the debt market and that long-dated low-dollar price sovereign bonds look the most attractive given the balance of risks. Stay tuned!

Chart at a Glance: Turkey Pre-Election Signals - Things Need To Change*

Source: Bloomberg LP

*J.P. Morgan GBI-EM Global Diversified Composite Unhedged USD Index – Comprehensive emerging market debt benchmark that track local currency bonds issued by Emerging market governments, denominated in U.S. dollars without any currency hedging.

**J.P. Morgan GBI-EM Turkey Broad USD Unhedged Index – Tracks the performance of a diversified range of local currency government bonds issued by Turkey, denominated in U.S. dollars without any currency hedging.

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.