Chinese Bonds Offer Yield Pickup

29 September 2020

Global bond investors have shown increasing appetite this year for Chinese bonds, particularly those denominated in local currency. They currently offer attractive yield advantage over U.S. and other developed markets bonds. Further, we believe the potential for currency appreciation, relative stability and diversification potential provide support for an allocation to Chinese domestic bonds within a global fixed income portfolio.

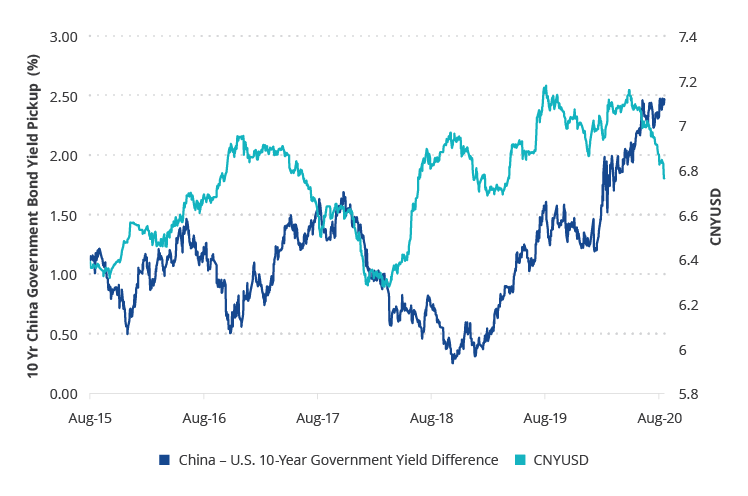

Currently, 10-year Chinese government bonds are yielding nearly 250 basis points above the 10-year U.S. Treasury, a differential that has increased sharply over the past two years.1 Local yields have increased over the past three months amid an impressive economic recovery and a muted monetary and fiscal policy response. However, the growing yield advantage has been driven primarily by the plunge in U.S. yields from over 3% to the current levels below 0.70%. This yield advantage is perhaps even more striking when considering China’s single-A credit rating and that it has the world’s second largest bond market behind only the U.S.

China Yield Pickup and FX Rate

Source: Bloomberg. Data as of 9/17/2020.

Beyond the attractive yield potential, the RMB has recently appreciated and provided additional return to investors, driven by some of the same factors behind the recent move in rates. Policymakers in China closely manage the currency’s value, which is one reason it has not historically experienced the same level of volatility of other emerging markets currencies. Further, there is a massive local investor base that can provide liquidity and funding, even in stressed periods. These attributes have made China local bonds a relatively more stable part of the emerging markets debt landscape.

With gradual inclusion in local bond indices continuing, including the ongoing addition to the J.P. Morgan GBI-EM suite of indices and recently announced inclusion in the FTSE World Government Bond Index, inflows from foreign investors are expected to continue and may reach $300 billion as passively managed funds adjust their allocations. This amount will likely be higher as actively managed portfolios also increase exposure. In addition to the yield advantage, currency appreciation potential and stability provided, we believe onshore bonds have also exhibited attractive diversification benefits. They have very low correlation to U.S. Treasuries and investment grade bonds, lower correlation to other emerging markets bonds (both local and hard currency) than U.S. high yield, and a lower correlation to U.S. equity than emerging markets bonds and U.S. high yield.2

Related Insights

Related Insights

18 diciembre 2025

04 diciembre 2025

28 octubre 2025

26 junio 2025

18 diciembre 2025

Prepare su portafolio para 2026 con información detallada del equipo de inversiones de VanEck sobre los factores que determinarán el riesgo y los rendimientos en sus respectivas clases de activos.

04 diciembre 2025

La deuda de alto rendimiento de mercados emergentes ha extendido su dinamismo en 2025, ofreciendo un carry sólido y rendimientos atractivos. Gracias a una mayor calidad crediticia y a menores tasas de incumplimiento, este segmento presenta un perfil de riesgo más favorable que la deuda estadounidense de alto rendimiento.

28 octubre 2025

El equipo de deuda de mercados emergentes acaba de regresar de las reuniones anuales de otoño del FMI; estas son sus conclusiones.

26 junio 2025

Los riesgos de estanflación, el aumento de las probabilidades de recesión y la dinámica cambiante del poder mundial están reconfigurando el panorama de inversión, lo que obliga a los inversores a replantearse dónde reside realmente la seguridad y las oportunidades.

16 mayo 2025

Los bonos locales de los mercados emergentes están obteniendo mejores resultados en 2025, ya que ofrecen un alto rendimiento, diversificación y sólidos fundamentos en medio de la debilidad del mercado estadounidense.