Emerging Markets Bonds: EMFX Key to 2020 Returns

16 April 2020

Read Time 2 MIN

At current valuations, we expect that emerging markets local currency bond returns will primarily be driven by currencies for the remainder of the year. If global growth shows signs of a recovery and the stimulative efforts of emerging markets central banks are successful, emerging markets currencies (EMFX) may rally from here as risk appetite and the search for yield re-emerges.

Emerging markets central banks have responded to the recent downturn by prioritizing growth and financial stability over inflation. Many have aggressively cut rates, and in some countries, quantitative easing (QE)-style open market operations have been implemented. Most of the countries in the J.P. Morgan GBI-EM Global Core Index went into the current downturn with the benefit of high real interest rates (nominal rates adjusted for inflation), and have been able to support growth through conventional monetary policy in contrast to developed markets, which already had near-zero or negative real rates. As opposed to previous episodes of risk aversion and capital outflows, we believe external vulnerabilities are reduced for many countries, foreign currency reserves are higher and the downside risks to growth appear to outweigh inflation pressures for now.

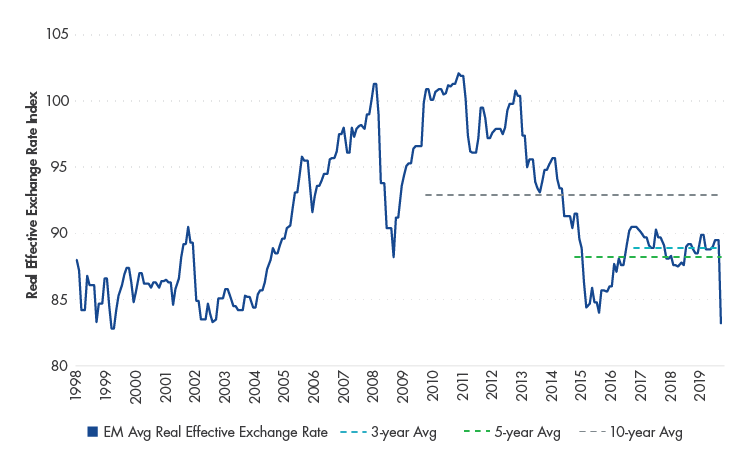

One result of lower rates amidst the current risk-off environment has been a steep decline in the values of many emerging markets currencies, particularly those of oil exporters such as Mexico and Russia. In terms of real effective exchange rates, which account for changes in price levels and the balance among a country’s trading partners, the average valuation of emerging markets currencies has not been this low since 1999 and is well below historical averages.

Real Effective Exchange Rates Attractive by Historical Standards

Source: J.P. Morgan and VanEck. Real Effective Exchange Rate Index represents the weighted average of the real effective exchange rates of the countries in the J.P. Morgan GBI-EM Global Core Index using 3/31/2020 country weights.

The approach being taken by emerging markets central banks is untested, and there are several risks to this scenario, in our view. Further growth downgrades would negatively impact currencies, as well as worsening fiscal and current account balances, inflation pressures, and accelerating capital outflows. Although oil importers make up the majority of the index, a prolonged period of severely depressed oil prices may also keep pressure on commodity sensitive currencies.

Related Insights

Related Insights

18 diciembre 2025

04 diciembre 2025

28 octubre 2025

26 junio 2025

18 diciembre 2025

Prepare su portafolio para 2026 con información detallada del equipo de inversiones de VanEck sobre los factores que determinarán el riesgo y los rendimientos en sus respectivas clases de activos.

04 diciembre 2025

La deuda de alto rendimiento de mercados emergentes ha extendido su dinamismo en 2025, ofreciendo un carry sólido y rendimientos atractivos. Gracias a una mayor calidad crediticia y a menores tasas de incumplimiento, este segmento presenta un perfil de riesgo más favorable que la deuda estadounidense de alto rendimiento.

28 octubre 2025

El equipo de deuda de mercados emergentes acaba de regresar de las reuniones anuales de otoño del FMI; estas son sus conclusiones.

26 junio 2025

Los riesgos de estanflación, el aumento de las probabilidades de recesión y la dinámica cambiante del poder mundial están reconfigurando el panorama de inversión, lo que obliga a los inversores a replantearse dónde reside realmente la seguridad y las oportunidades.

25 junio 2025

Los bonos de mercados emergentes han tenido un mejor desempeño de forma discreta que los mercados amplios de EE. UU. y globales durante la última década, al ofrecer rendimientos altos, fundamentos sólidos y diversificación en medio de los riesgos globales.