Welcome to VanEck

Select Investor Type

18 October 2022

After a brutal re-pricing in 2022, global bond prices are beginning to be considered enticing.

The global government bond benchmark now yields 3% after 1% at the start of the year, global investment grade yields 5% up from 2% and global high-yield is touching almost 10%.1

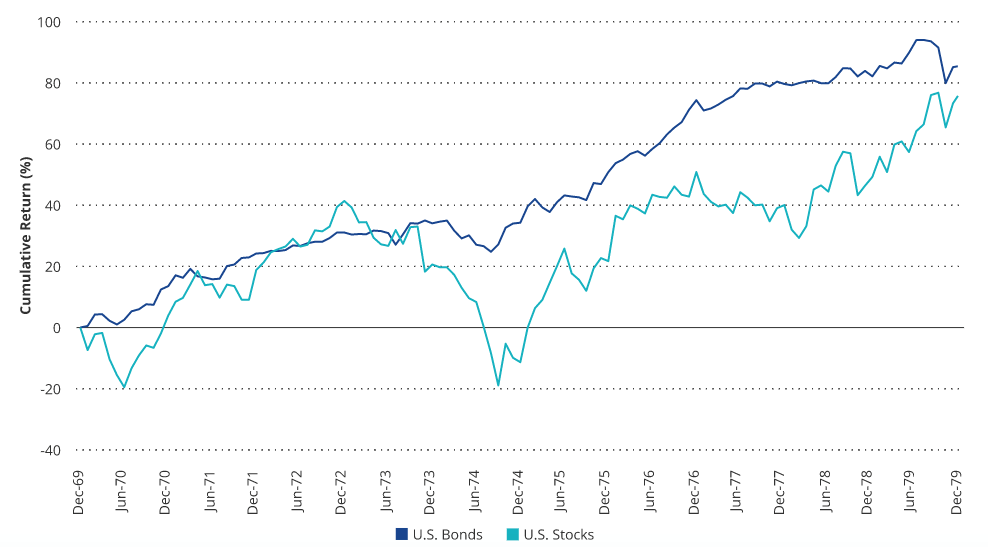

Looking back to another time of high inflation and low economic growth, the 1970s, the best performing US asset class excepting commodities and gold was, surprisingly, bonds. Indeed, bonds rose by more than 80% over the decade, easily outpacing stocks.

Past performance is not a reliable indicator for future performance.

With interest rates super low, a rise in rates can do a lot of damage to bond prices. That’s what’s happened so far in 2022, as central banks have lifted interest rates to stifle inflation. But once rates have already risen from low levels, subsequent increases are less dramatic. What’s more, if bonds are yielding 5-6% that has a tremendous compounding effect.

What’s more, the correction in global bond prices may be nearing its end. Inflation appears close to a peak in the US at least, broken by higher rates and escalating energy prices that are leading to the possibility of recession. If so, rates in the US should be close to a peak too. Obviously, this is only my personal estimate and cannot be guaranteed.

Based on all of this, I think bonds could be an attractive place to be, because the corollary of lower bond prices is higher income yields. While we don’t know how much damage may be done to companies and their bonds if there is a recession, I believe that corporate bonds have already priced in a lot of the potential bad news although obviously future performance cannot be guaranteed. It’s up to investors to allocate across fixed income, according to their individual risk appetites.

1 Source: ICE.

2 Past performance is not a guarantee of future results.

All data as of 11 October 2022.

VanEck Asset Management B.V., the management company of VanEck iBoxx EUR Sovereign Capped AAA-AA 1-5 UCITS ETF, VanEck iBoxx EUR Sovereign Diversified 1-10 UCITS ETF, VanEck Global Fallen Angel High Yield Bond UCITS ETF, VanEck iBoxx EUR Corporates UCITS ETF, VanEck Emerging Markets High Yield Bond UCITS ETF sub-funds of VanEck ETFs N.V., is a UCITS management company incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). The ETF is registered with the AFM and tracks a bond index. The value of the ETF’s assets may fluctuate heavily as a result of the investment strategy. If the underlying index falls in value, the ETF will also lose value.

Investors must read the sales prospectus and key investor information before investing in a fund. These are available in English and the KIDs in certain other languages as applicable and can be obtained free of charge at www.vaneck.com or from the Management Company.

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

18 May 2026

15 May 2026

18 May 2026

15 May 2026