Growth Cliff vs. Policy Credibility

06 October 2022

Read Time 2 MIN

EM Growth Outlook

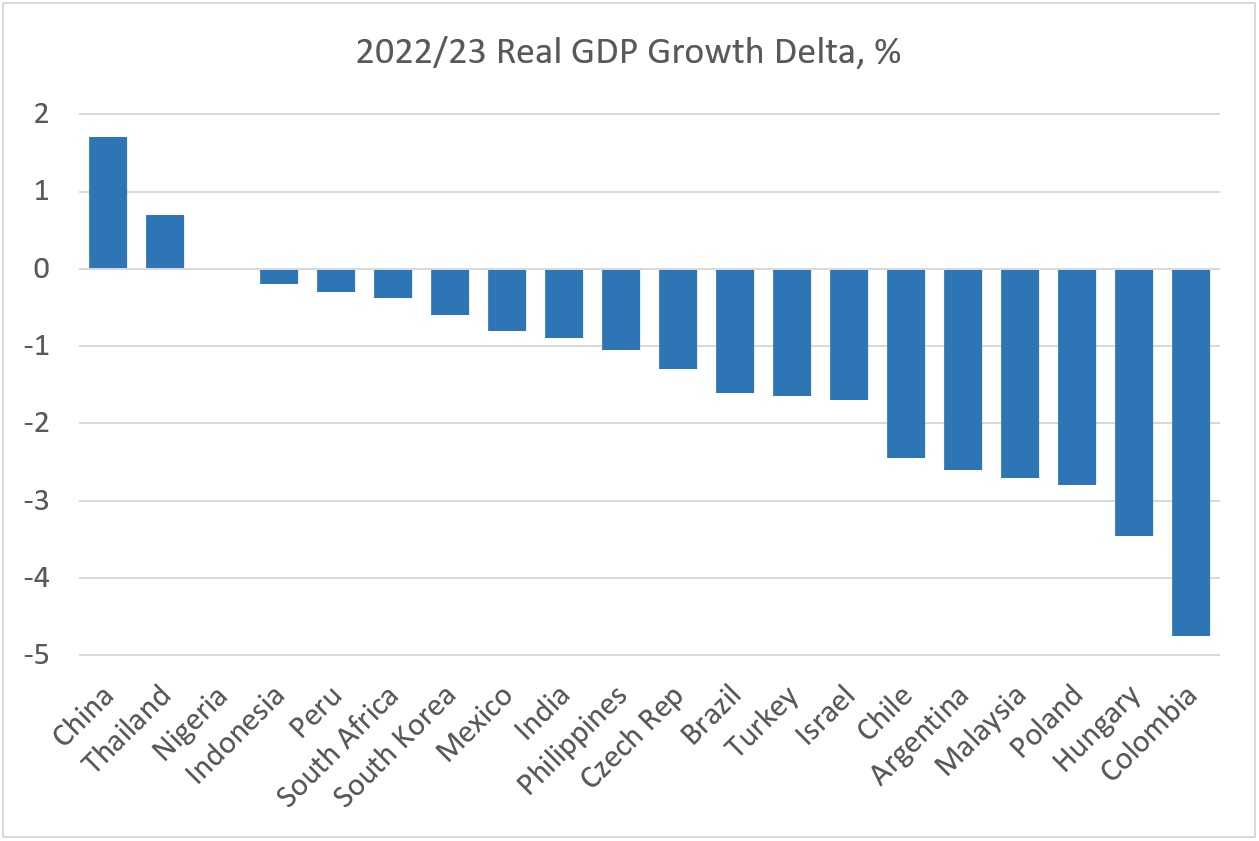

The International Monetary Fund’s (IMF) updated growth projections should be released any day now, but the consensus forecast points to a significant 2023 slowdown in major economies in emerging Europe and LATAM (see chart below). This so–called growth cliff is already having an impact on monetary policy decisions in countries like Poland, which surprised the market yesterday by keeping the benchmark rate on hold, despite re–accelerating inflation. The central bank statement revealed major concerns about the growth outlook — but also hopes that the slowdown will help to lower inflation in the coming months. The reasoning is very similar to that of the Czech National Bank — which extended its rate pause in September — together with the belief that inflation is driven mainly by exogenous factors that are outside of central bank’s policy scope.

Dovish Pivots In EM

These central banks certainly have a point. The question is whether the dovish pivot is sustainable, because if you do not hike and your currency continues to weaken, this can add to inflation pressures. One possible Plan B is FX interventions. The Czech National Bank has plenty of reserves, so it can afford to spend estimated 20% of them to support the currency (year–to–date). But international reserves are not infinite, so if sizable interventions continue in the coming weeks, the central bank might need to look for other alternatives. The Hungarian central bank just introduced a new line of short–term instruments, hoping they will help to drain liquidity without additional rate hikes.

Pace Of Rate Hikes In LATAM

In LATAM, today’s focus is on the Peruvian central bank, which is expected to deliver another small 25bps rate hike after the New York market close. The latest inflation print in Peru was a bit higher than consensus, but sequential inflation showed signs of moderation. Importantly, the government’s fiscal accounts look good (small deficit in 2022 and 2023) — so there are no additional inflation risks associated with this particular factor. So, there may be room for keeping the policy rate on hold safely after today’s hike. Stay tuned!

Chart at a Glance: Who Is Afraid of a Growth Cliff in EM?

Source: Bloomberg LP.

Related Insights

Related Insights

07 April 2025

06 March 2025

20 February 2025

16 January 2025

07 April 2025

Trump’s tariffs spark trade war fears, fueling market volatility, inflation risk, and recession threats. With global retaliation likely, near-term growth is clearly at risk.

06 March 2025

Trump’s tariffs, AI’s next phase, and a potential U.S. gold revaluation could shake markets—investors who stay ahead of these transitions will be best positioned.

20 February 2025

China's AI breakthrough, persistent inflation, gold’s outperformance, and rising energy demand underscore a shifting investment landscape.

16 January 2025

In 2025, navigating turbulence means balancing tech innovation, inflation hedges, energy shifts, and risks from spending cuts and inflation.

05 December 2024

"Trump Trade 2.0" fueled U.S. equity and digital asset rallies, while real assets faltered under a strong dollar, with global markets reacting unevenly to pro-growth policies.