Welcome to VanEck

Select Investor Type

04 June 2020

When working to forge the United Nations after World War II, Winston Churchill is reputed to have quipped: “never waste a good crisis.” Seventy years later, in a different kind of crisis, it’s again a time for reflection and review. In the case of investing, the global pandemic has triggered an economic recession, making this a logical time to prioritize portfolio diversification.

To quote another figure from history, US financier Andrew Mellon is reported to have stated at the time of the 1929 Wall Street Crash that “gentlemen prefer bonds.” Although financial market folklore sometimes confuses this with the title of a 1953 Marilyn Monroe film “Gentlemen prefer blondes,” in fact Mellon’s original meaning was more practical. His point being: an educated person’s portfolio should include some bonds.

My experience is that, in recent years, investors have allocated increasingly to equities at the expense of fixed income. Yet diversification into bonds would have reduced losses in March’s sharp bear market. Looking forward at a time of continuing economic uncertainty, fixed income has a role to play in diversifying and reducing a portfolio’s risk.

But what of the returns at a time of record low yields?

As the COVID-19 pandemic has unfolded, yields on euro sovereign and quality corporate bonds have remained extremely low. For example, despite France’s massive increase in state spending to support the economy, the country’s 10-year government bond yield was 0.0% at the end of May, up slightly from -0.3% at the end of February, before the pandemic hit financial markets. Turning to high quality euro corporate bonds, even the yield on the VanEck iBoxx EUR Corporates UCITS ETF was just 1.1% in late May.

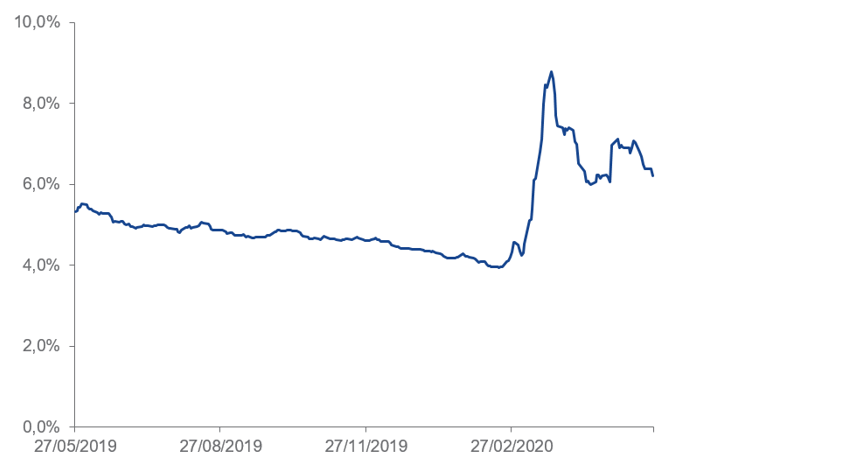

But the returns on high yield bonds have risen significantly. For example, the yield on the VanEck Global Fallen Angel High Yield Bond UCITS ETF increased from 4.0% at mid February to 6.2% as 26 May, see figure 1. Please be aware that yield is inversely related to actual performance. Overall, the performance of the ETF has been negative since the start of the COVID-19 pandemic. This ETF invests in corporate bonds which were investment grade at the moment of issuance, but have since been downgraded to sub-investment grade.

Past performance is not a reliable indicator for future performance. Source: VanEck. Data for the period 27/5/2019 – 26/5/2020.

Despite the derogatory labels of “sub-investment grade” or even “junk” bonds, many institutional investors allocate to this asset class. According to Mercer, the consulting firm, 10% of European pension funds have a strategic allocation to high yield bonds2. Actual allocation will probably be higher, as many allocate to it as part of broader credit mandates. According to S&P, the high yield market constitutes roughly 15% of the corporate bond market3.

However, not many individuals have a pension fund’s resources or expertise. Let’s therefore spend some time discussing how to assess the risks.

High yields bonds contain three main sources of risk:

Each of them needs to be viewed in different ways.

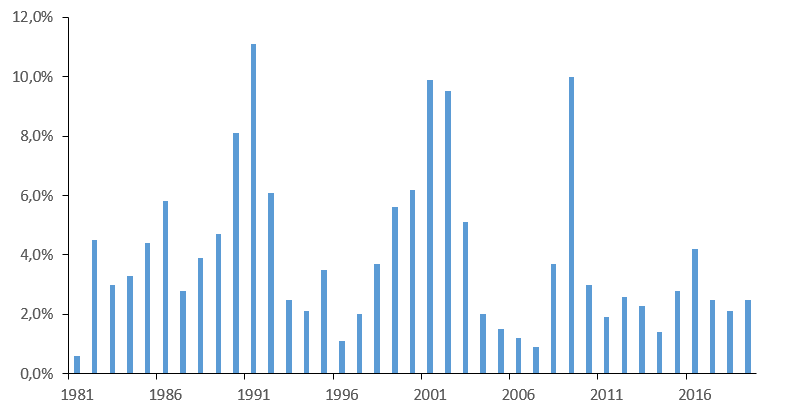

Credit risk is the risk that a bond defaults. In other words, the corporate borrower issuing the bond cannot make its regular coupon payments or redeem the principal. But how can individuals even begin to estimate default risks? What can help, as a first step, is looking at historical default rates. As we can see in figure 2, they have averaged 4.0% over the last 37 years for global high yield bonds, rising in recessions and falling back in recoveries.

Source: S&P - Default, Transition, and Recovery: 2019 Annual Global Corporate Default And Rating Transition Study.

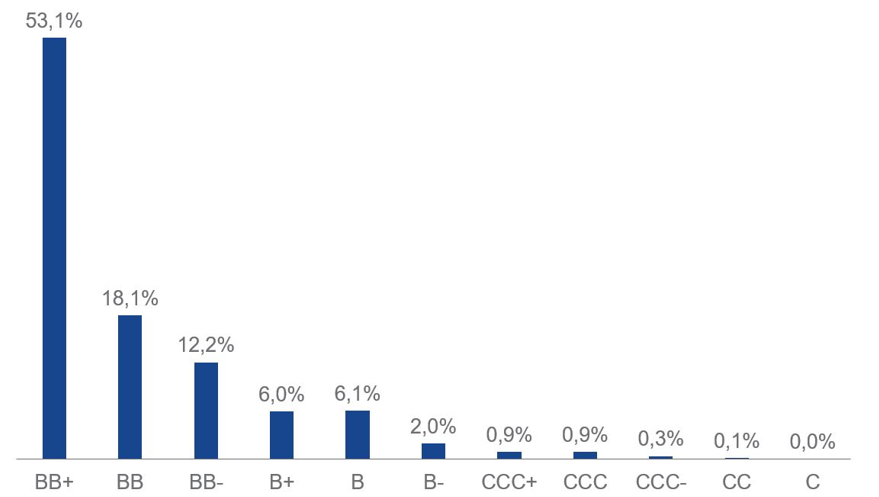

A next step is to peer more closely at the bonds and judge their quality, which tells us whether they are likely to default. Fortunately, credit rating agencies exist to do just this. The VanEck Global Fallen Angel High Yield Bond UCITS ETF shows you, in figure 3, the different ratings of the bonds it includes – starting from higher quality BB+-rated bonds and going through to the few bonds rated CCC-. Turning to figure 4, you can see the records for how different rating categories have defaulted over 20 years. While it is important to note that history does not repeat itself, it often rhymes. In other words, it gives an idea of the patterns you might see, or the probability of default.

Source: ICE, data as of 30/4/2020.

| AAA | AA | A | BBB | BB | B | CCC/C | |

| 2000 | 0.00 | 0.00 | 0.27 | 0.37 | 1.16 | 7.71 | 35.96 |

| 2001 | 0.00 | 0.00 | 0.27 | 0.34 | 2.98 | 11.56 | 45.45 |

| 2002 | 0.00 | 0.00 | 0.00 | 1.02 | 2.90 | 8.20 | 44.44 |

| 2003 | 0.00 | 0.00 | 0.00 | 0.23 | 0.59 | 4.07 | 32.73 |

| 2004 | 0.00 | 0.00 | 0.08 | 0.00 | 0.44 | 1.45 | 16.18 |

| 2005 | 0.00 | 0.00 | 0.00 | 0.07 | 0.31 | 1.74 | 9.09 |

| 2006 | 0.00 | 0.00 | 0.00 | 0.00 | 0.30 | 0.82 | 13.33 |

| 2007 | 0.00 | 0.00 | 0.00 | 0.00 | 0.20 | 0.25 | 15.24 |

| 2008 | 0.00 | 0.38 | 0.39 | 0.49 | 0.81 | 4.11 | 27.27 |

| 2009 | 0.00 | 0.00 | 0.22 | 0.55 | 0.75 | 11.01 | 49.46 |

| 2010 | 0.00 | 0.00 | 0.00 | 0.00 | 0.58 | 0.87 | 22.73 |

| 2011 | 0.00 | 0.00 | 0.00 | 0.07 | 0.00 | 1.68 | 16.42 |

| 2012 | 0.00 | 0.00 | 0.00 | 0.00 | 0.30 | 1.58 | 27.52 |

| 2013 | 0.00 | 0.00 | 0.00 | 0.00 | 0.10 | 1.65 | 24.67 |

| 2014 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.78 | 17.51 |

| 2015 | 0.00 | 0.00 | 0.00 | 0.00 | 0.16 | 2.41 | 26.67 |

| 2016 | 0.00 | 0.00 | 0.00 | 0.06 | 0.47 | 3.75 | 33.33 |

| 2017 | 0.00 | 0.00 | 0.00 | 0.00 | 0.08 | 1.00 | 26.45 |

| 2018 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.99 | 27.18 |

| 2019 | 0.00 | 0.00 | 0.00 | 0.11 | 0.00 | 1.49 | 30.05 |

Source: S&P Default, Transition, and Recovery: 2019 Annual Global Corporate Default And Rating Transition Study.

It’s important to note that even when bonds default, the investor does not always lose the full value of the bond. That’s because the liquidator of the company will recover as much value as possible. Again, taking history as a guide, recovery rates for US bonds have been 47%6.

In technical market jargon, one minus the recovery rate is called the “loss given default”. By multiplying the probability of default with the loss given default, one can anticipate the expected loss of a bond. Normally the mechanics of financial markets mean that the expected loss should be lower than the bond’s interest rate spread over sovereign bonds. Otherwise there would be no incentive to buy high yield bonds. However, markets can be wrong and actual defaults might be higher than yields suggest.

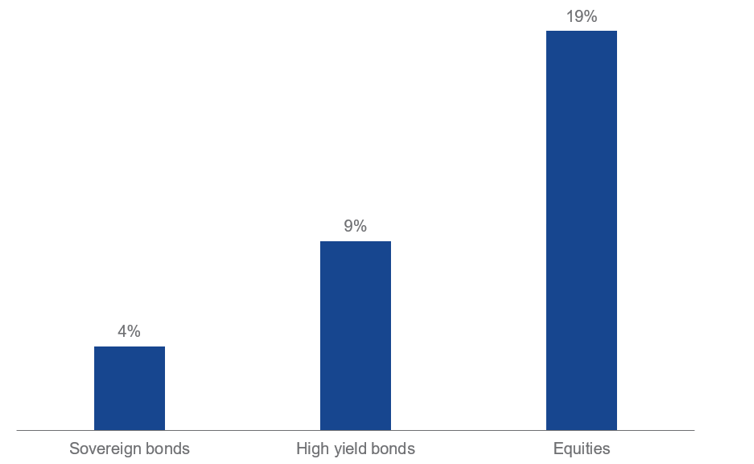

Even if a bond does not default, prices can fluctuate as investors become risk averse and require higher yields to compensate for the risk of investing. For long-term investors, this should make little difference – the bond will eventually be repaid at face value when it matures, so market fluctuations don’t matter. However, in the short term, the investor’s portfolio can decrease in value. In figure 5, we compare the volatility of high yield bonds with that of sovereign bonds and equities. We can see that it is roughly in between the two, but closer to sovereign bonds than to equities.

Past performance is not a reliable indicator for future performance. This also holds for historical market data.

Source: VanEck. For sovereign bonds the VanEck iBoxx EUR Sovereign Diversified 1-10 UCITS ETF has been used, for high yield bonds the VanEck Global Fallen Angel High Yield Bond UCITS ETF and for equities the VanEck Global Equal Weight UCITS ETF. Data for the period 19/3/2018 (launch of the VanEck Global Fallen Angel High Yield Bond UCITS ETF) – 26/5/2020. Using longer periods leads to comparable results. Do note that the SRRI scores of the three ETFs are respectively 3, 4 and 5 and hence are in line with the above analysis.

Obviously, market movements are not always a bad thing. Sometimes it works in the investor’s favor. If investors become less risk averse or markets look more positively on the credit cycle, spreads should tighten and bond prices will rise.

Finally, it is important to note that EU investors take a currency risk if they buy non-euro denominated bonds. Should the euro rise against the currency of the bond, the value of the bond for a euro investor would decrease. Again, this goes both ways: if the euro fell in value, the bond would increase in value for EU investors.

So, this crisis is a good time to think about lifting allocations to bonds, and especially high yield bonds as they still offer attractive returns. Of course, Churchill would likely be in favor of investors reviewing their options after such a momentous crisis, although history does not relate his liking for bonds (or indeed blondes for that matter).

1Yield is the expected return in absence of default. The numbers quoted here are "yield-to-worst” which is lowest of either yield-to-maturity or yield-to-call date on every possible call date.

2Source: Mercer - European asset allocation survey 2019.

3Source: https://www.spglobal.com/marketintelligence/en/pages/toc-primer/hyd-primer#sec2.

4The rating distribution indicates the relative weight of bonds of various credit ratings. I.e., if the graphs indicates 55% for a given credit rating, it means that 55% of the total portfolio is invested in bonds with that credit rating.

5The table shows for each year which share of bonds in the global universe of S&P has defaulted. E.g., in 2009 11.01% of all bonds which S&P rated B defaulted. S&P is one of the world’s major credit rating agencies. Other agencies such as Moody’s or Fitch do not necessarily give the same rating to the same bond. However, on average ratings are in line.

6Volatility is an indicator of level of risk. It relates to how much daily prices have fluctuated in the past over the period measured. The higher the volatility, the higher the risk of the instrument. Contrary to performance, historical volatility tends to be an indicator of future volatility.

Fund-specific Disclosure

VanEck iBoxx EUR Corporates UCITS ETF and VanEck Global Equal Weight UCITS ETF are sub-funds of VanEck ETFs N.V., an investment scheme which is domiciled in the Netherlands and registered with the Dutch Authority for the Financial Markets and subject to the European regulation of collective investment schemes under the UCITS Directive.

VanEck iBoxx EUR Corporates UCITS ETF tracks a bond index. VanEck Global Equal Weight UCITS ETF tracks an equity index. VanEck Global Fallen Angel High Yield Bond UCITS ETF is a sub-fund of VanEck UCITS ETFs plc., an investment scheme which is domiciled in Ireland and registered with the Central Bank of Ireland and subject to the European regulation of collective investment schemes under the UCITS Directive. VanEck Global Fallen Angel High Yield Bond UCITS ETF tracks a bond index.

The value of an ETF's assets may fluctuate widely as a result of its investment policy. If the underlying index falls in value, the ETF also falls in value.

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

18 May 2026

15 May 2026