Welcome to VanEck

Select Investor Type

07 September 2020

“How many millionaires do you know who have become wealthy by investing in savings accounts? I rest my case." - Robert G. Allen, American finance writer and author of the ‘One minute millionaire’.

In anxious times savings are soaring. Across Europe, household savings are hitting all-time highs. The destination for this glut of idle cash? Bank accounts that are earning close to zero for their owners.

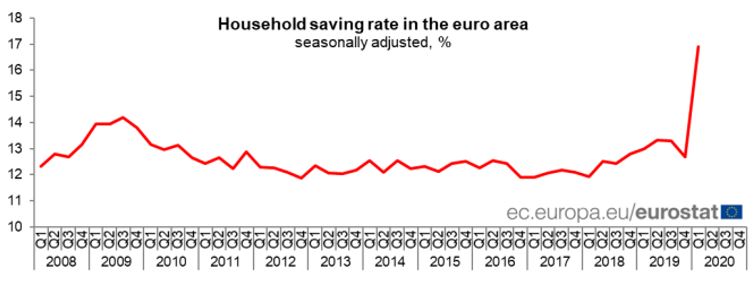

As the gathering pandemic sent society into lockdown, the household saving rate touched 16.9% in the first three months of 2020, according to the European Central Bank's (ECB) survey of the euro area (see figure 1). For comparison, the rate was 12.7% in the final months of 2019.

Seasonally adjusted household saving rate (in %)

Source: Eurostat press release, 7 July 2020.

It's true that the number of individual investors investing in stocks and funds is also growing, as we wrote last month. But the number of them is dwarfed by the rush into bank accounts, which pay nothing.

Let me tell you why that is not very wise. Remind yourself that prices tend to rise while the value of your cash remains the same. That's called inflation, and currently there is a lot of debate about how this will develop. Looking back in history, which in the end is all we really can do, we see that prices tend to rise. Which means that it can arguably be less risky to put your money in a broad spread of reasonable investments that should at least match inflation than in a bank account, which won't.

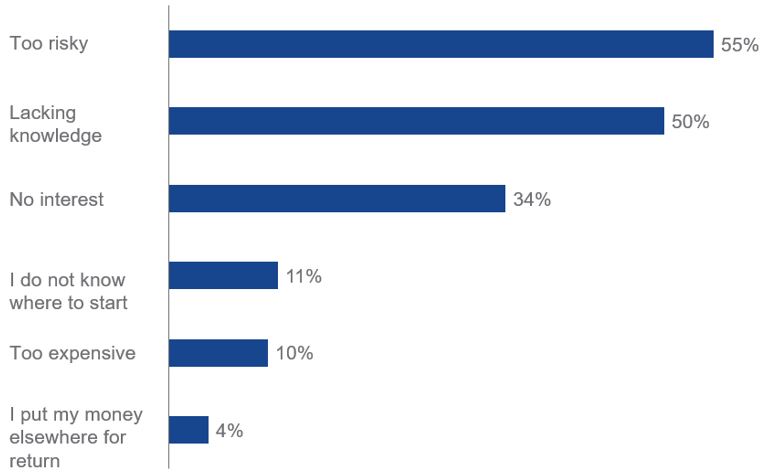

So, why don't individuals invest more? What are the reasons? When Dutch people were asked last year, more than half (55%) said that investing was too risky, according to a survey of more than 50,000 people carried out by the country's financial regulator (see figure 1). Half (50%) said that they lacked knowledge. And, a third (34%) admitted that they had no interest.

We could sum this up as fear of the unknown.

Source: AFM – Consumer Monitor 2019. Representative survey amongst 50,864 Dutch adults, October 2019.

As we have already said, putting your money in the bank is not without risk and there are three reasons for this.

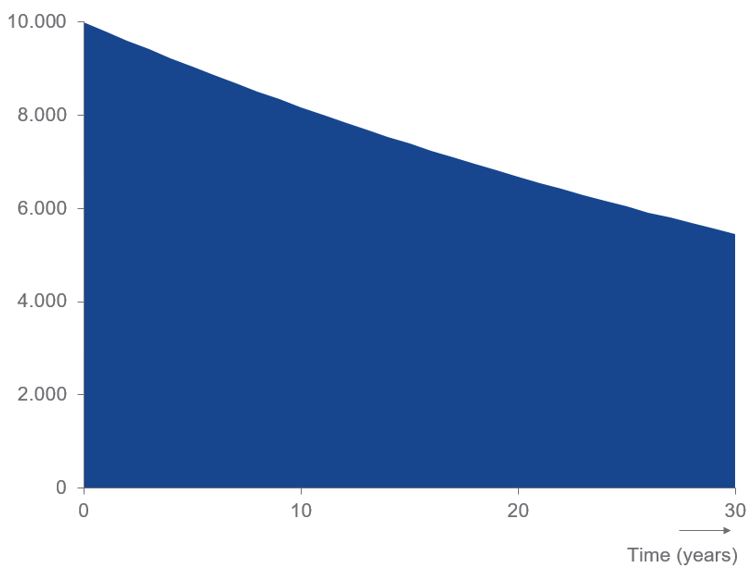

Firstly, if interest rates are zero or close to zero, inflation will eat into the value of your savings. To illustrate this, consider someone who deposits €10,000, £10,000 or CHF10,000 in the bank at a time when inflation averages about 2% (the ECB';s long-term target). The real value of your money would fall to a bit over 5.400 of whatever currency you've saved up, after 30 years (see figure 3).

Evolution of value of initial investment of 10,000 (€, £ or CHF) assuming zero interest rates and 2% annual inflation

Source: VanEck calculations.

Secondly, even banks can go bankrupt. Although governments protect deposits through deposit protection schemes, the level of protection is finite. Take the European Deposit Insurance Scheme in the EU or the Financial Services Compensation Scheme in the UK. These schemes only protect your cash up to €100,000 or £85,000 respectively.

Thirdly, what many people don't realize is that if you put more than these amounts in a bank account, you're effectively investing in the bank remaining solvent. When you deposit money with a bank you're investing in that bank's ability to lend wisely to both businesses and people, both of which may default on their loans or mortgages.

Given that you're reading this newsletter, the chances are that you're already investing. So maybe, you can use the arguments above to motivate someone else to start investing. If you're not investing, or if the bulk of your savings are in the bank, I would like to state some of investing's basic truths.

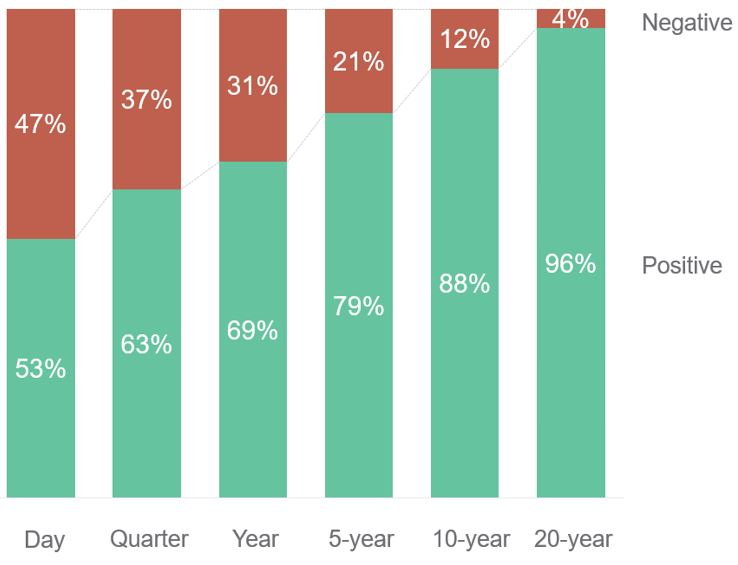

In the long run, investing is not as risky as many think. The following graph (figure 4) shows that, historically, the chances of losing money through investing in equities diminish the longer you hold them. Note that equities are a relatively risky asset class. Adding less risky asset classes such as bonds to one's portfolio further reduces the risk of short-term losses.

Historical probabilities of realizing a positive or negative return for various holding periods

Past performance is not a reliable indicator for future performance. Source: VanEck analysis based on total returns of the S&P500. Data for the period 1-1-1928 until 20-9-2019. Returns are nominal, not corrected for inflation.

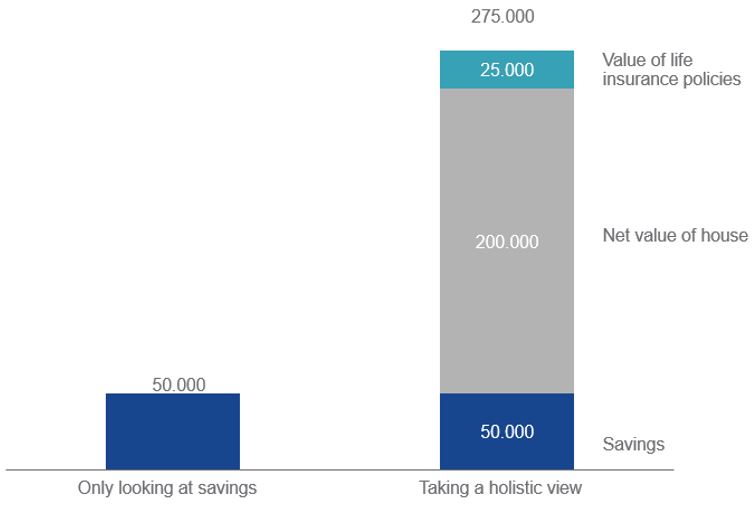

Ok, so you don't want to invest all your savings, fair enough. But think about it, your savings and investments are likely to be less than half of the picture. What about your house, life insurance policies, pension savings and future salary earnings? These are all already part of your wealth. Considering your potential investing decision in this context shows that not so much of your capital is at high risk. As illustrated in figure 5, you might be more willing to invest a significant part of your savings if you take such a holistic view, rather than simply looking at savings and investments alone.

Obviously, when deciding to invest, one should not follow the fad of the day. Rather one should take well-informed decisions, based on self-learning or independent third party advice and a thorough understanding of one's own financial capacity and risk appetite.

What is my net worth?

Source: VanEck. Hypothetical numbers.

Recently, a big European private bank reiterated its recommended long-term asset allocation. This asset allocation is how much it thinks clients should put in cash, equities, bonds and so on to protect and grow their money in the long term. Their view is you should allocate close to zero to cash. I share that view. You need cash to use and cover planned expenses and to act as a buffer so that you can survive any periods of unemployment. All other cash, even if only a small regular monthly payment, could be used to invest and build a healthy portfolio.

For any long-term investor, holding a large amount of cash looks like a good way of getting less wealthy.

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

18 May 2026

15 May 2026